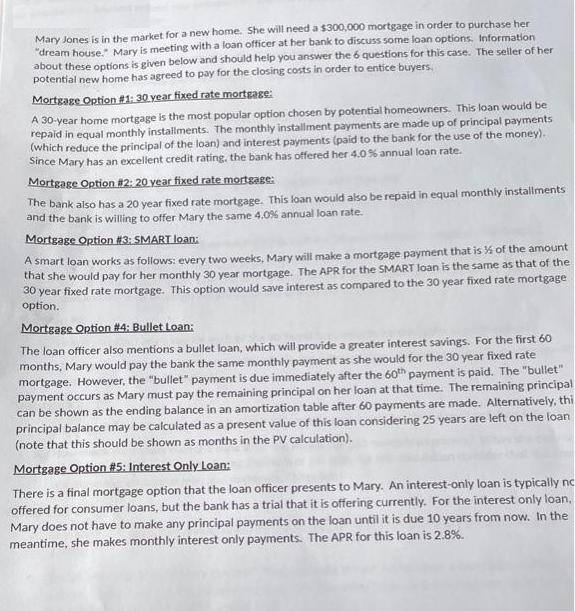

Mary Jones is in the market for a new home. She will need a $300,000 mortgage...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

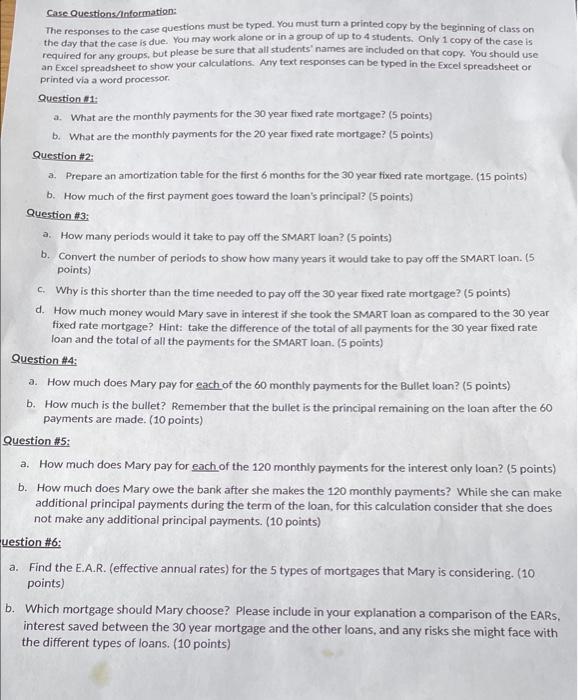

Mary Jones is in the market for a new home. She will need a $300,000 mortgage in order to purchase her "dream house." Mary is meeting with a loan officer at her bank to discuss some loan options. Information about these options is given below and should help you answer the 6 questions for this case. The seller of her potential new home has agreed to pay for the closing costs in order to entice buyers. Mortgage Option # 1: 30 year fixed rate mortgage: A 30-year home mortgage is the most popular option chosen by potential homeowners. This loan would be repaid in equal monthly installments. The monthly installment payments are made up of principal payments (which reduce the principal of the loan) and interest payments (paid to the bank for the use of the money). Since Mary has an excellent credit rating, the bank has offered her 4.0% annual loan rate. Mortgage Option #2: 20 year fixed rate mortgage: The bank also has a 20 year fixed rate mortgage. This loan would also be repaid in equal monthly installments and the bank is willing to offer Mary the same 4.0% annual loan rate. Mortgage Option #3: SMART loan: A smart loan works as follows: every two weeks, Mary will make a mortgage payment that is % of the amount that she would pay for her monthly 30 year mortgage. The APR for the SMART loan is the same as that of the 30 year fixed rate mortgage. This option would save interest as compared to the 30 year fixed rate mortgage option. Mortgage Option #4: Bullet Loan: The loan officer also mentions a bullet loan, which will provide a greater interest savings. For the first 60 months, Mary would pay the bank the same monthly payment as she would for the 30 year fixed rate mortgage. However, the "bullet" payment is due immediately after the 60th payment is paid. The "bullet" payment occurs as Mary must pay the remaining principal on her loan at that time. The remaining principal can be shown as the ending balance in an amortization table after 60 payments are made. Alternatively, thi principal balance may be calculated as a present value of this loan considering 25 years are left on the loan (note that this should be shown as months in the PV calculation). Mortgage Option #5: Interest Only Loan: There is a final mortgage option that the loan officer presents to Mary. An interest-only loan is typically no offered for consumer loans, but the bank has a trial that it is offering currently. For the interest only loan, Mary does not have to make any principal payments on the loan until it is due 10 years from now. In the meantime, she makes monthly interest only payments. The APR for this loan is 2.8%. Case Questions/Information: The responses to the case questions must be typed. You must turn a printed copy by the beginning of class on the day that the case is due. You may work alone or in a group of up to 4 students. Only 1 copy of the case is required for any groups, but please be sure that all students' names are included on that copy. You should use an Excel spreadsheet to show your calculations. Any text responses can be typed in the Excel spreadsheet or printed via a word processor. Question #1: a. What are the monthly payments for the 30 year fixed rate mortgage? (5 points) b. What are the monthly payments for the 20 year fixed rate mortgage? (5 points) Question #2: a. Prepare an amortization table for the first 6 months for the 30 year fixed rate mortgage. (15 points) b. How much of the first payment goes toward the loan's principal? (5 points) Question #3: a. How many periods would it take to pay off the SMART loan? (5 points) b. Convert the number of periods to show how many years it would take to pay off the SMART loan. (5 points) C. Why is this shorter than the time needed to pay off the 30 year fixed rate mortgage? (5 points) d. How much money would Mary save in interest if she took the SMART loan as compared to the 30 year fixed rate mortgage? Hint: take the difference of the total of all payments for the 30 year fixed rate loan and the total of all the payments for the SMART loan. (5 points) Question #4: a. How much does Mary pay for each of the 60 monthly payments for the Bullet loan? (5 points) b. How much is the bullet? Remember that the bullet is the principal remaining on the loan after the 60 payments are made. (10 points) Question #5: a. How much does Mary pay for each of the 120 monthly payments for the interest only loan? (5 points) b. How much does Mary owe the bank after she makes the 120 monthly payments? While she can make additional principal payments during the term of the loan, for this calculation consider that she does not make any additional principal payments. (10 points) question #6: a. Find the E.A.R. (effective annual rates) for the 5 types of mortgages that Mary is considering. (10 points) b. Which mortgage should Mary choose? Please include in your explanation a comparison of the EARS, interest saved between the 30 year mortgage and the other loans, and any risks she might face with the different types of loans. (10 points) Mary Jones is in the market for a new home. She will need a $300,000 mortgage in order to purchase her "dream house." Mary is meeting with a loan officer at her bank to discuss some loan options. Information about these options is given below and should help you answer the 6 questions for this case. The seller of her potential new home has agreed to pay for the closing costs in order to entice buyers. Mortgage Option # 1: 30 year fixed rate mortgage: A 30-year home mortgage is the most popular option chosen by potential homeowners. This loan would be repaid in equal monthly installments. The monthly installment payments are made up of principal payments (which reduce the principal of the loan) and interest payments (paid to the bank for the use of the money). Since Mary has an excellent credit rating, the bank has offered her 4.0% annual loan rate. Mortgage Option #2: 20 year fixed rate mortgage: The bank also has a 20 year fixed rate mortgage. This loan would also be repaid in equal monthly installments and the bank is willing to offer Mary the same 4.0% annual loan rate. Mortgage Option #3: SMART loan: A smart loan works as follows: every two weeks, Mary will make a mortgage payment that is % of the amount that she would pay for her monthly 30 year mortgage. The APR for the SMART loan is the same as that of the 30 year fixed rate mortgage. This option would save interest as compared to the 30 year fixed rate mortgage option. Mortgage Option #4: Bullet Loan: The loan officer also mentions a bullet loan, which will provide a greater interest savings. For the first 60 months, Mary would pay the bank the same monthly payment as she would for the 30 year fixed rate mortgage. However, the "bullet" payment is due immediately after the 60th payment is paid. The "bullet" payment occurs as Mary must pay the remaining principal on her loan at that time. The remaining principal can be shown as the ending balance in an amortization table after 60 payments are made. Alternatively, thi principal balance may be calculated as a present value of this loan considering 25 years are left on the loan (note that this should be shown as months in the PV calculation). Mortgage Option #5: Interest Only Loan: There is a final mortgage option that the loan officer presents to Mary. An interest-only loan is typically no offered for consumer loans, but the bank has a trial that it is offering currently. For the interest only loan, Mary does not have to make any principal payments on the loan until it is due 10 years from now. In the meantime, she makes monthly interest only payments. The APR for this loan is 2.8%. Case Questions/Information: The responses to the case questions must be typed. You must turn a printed copy by the beginning of class on the day that the case is due. You may work alone or in a group of up to 4 students. Only 1 copy of the case is required for any groups, but please be sure that all students' names are included on that copy. You should use an Excel spreadsheet to show your calculations. Any text responses can be typed in the Excel spreadsheet or printed via a word processor. Question #1: a. What are the monthly payments for the 30 year fixed rate mortgage? (5 points) b. What are the monthly payments for the 20 year fixed rate mortgage? (5 points) Question #2: a. Prepare an amortization table for the first 6 months for the 30 year fixed rate mortgage. (15 points) b. How much of the first payment goes toward the loan's principal? (5 points) Question #3: a. How many periods would it take to pay off the SMART loan? (5 points) b. Convert the number of periods to show how many years it would take to pay off the SMART loan. (5 points) C. Why is this shorter than the time needed to pay off the 30 year fixed rate mortgage? (5 points) d. How much money would Mary save in interest if she took the SMART loan as compared to the 30 year fixed rate mortgage? Hint: take the difference of the total of all payments for the 30 year fixed rate loan and the total of all the payments for the SMART loan. (5 points) Question #4: a. How much does Mary pay for each of the 60 monthly payments for the Bullet loan? (5 points) b. How much is the bullet? Remember that the bullet is the principal remaining on the loan after the 60 payments are made. (10 points) Question #5: a. How much does Mary pay for each of the 120 monthly payments for the interest only loan? (5 points) b. How much does Mary owe the bank after she makes the 120 monthly payments? While she can make additional principal payments during the term of the loan, for this calculation consider that she does not make any additional principal payments. (10 points) question #6: a. Find the E.A.R. (effective annual rates) for the 5 types of mortgages that Mary is considering. (10 points) b. Which mortgage should Mary choose? Please include in your explanation a comparison of the EARS, interest saved between the 30 year mortgage and the other loans, and any risks she might face with the different types of loans. (10 points)

Expert Answer:

Answer rating: 100% (QA)

1 a The mortgage with a fixed rate and a term of 30 years has monthly installments of 1433 The following formula can be used to determine the monthly payments for a mortgage with a fixed rate and 30 y... View the full answer

Related Book For

Principles of Auditing and Other Assurance Services

ISBN: 978-0078025617

19th edition

Authors: Ray Whittington, Kurt Pany

Posted Date:

Students also viewed these mathematics questions

-

A dairy is in the market for a new container-filling machine and is considering two models, manufactured by company A and company B. Ruggedness, cost, and convenience are comparable in the two...

-

A friend of yours is in the market for a new computer. Four different machines are under consideration. The four computers are essentially the same, but they vary in price and reliability. The least...

-

A debt of $6500 is repaid in equal monthly installments over four years. Interest is 9% com- pounded monthly. (a) What is the size of the monthly payments? (b) What will be the total cost of...

-

The Kc for the following reaction is 9.30 X 10^-2 at 25C:PCl5(g) <-> PCl3(g) + Cl2(g) How many moles & grams of PCl5 must be added to a 2-literflask to obtain a Cl2 concentration of 0.150M...

-

Suppose that job satisfaction scores can be modeled with N(100, 12). Human resource departments of corporations are generally concerned if the job satisfaction drops below a certain score. What score...

-

The initial price of a cup of coffee is $1, and at that price, 400 cups are demanded. If the price falls to $0.90, the quantity demanded will increase to 500. a) Calculate the (arc) price elasticity...

-

Steven Zhang, regional director of sales for Right Times Uniform Company, is reviewing the rsums and applications and his notes on three job candidates he interviewed for a vacant sales position in...

-

Unter Components manufactures low-cost navigation systems for installation in ride-sharing cars. It sells these systems to various car services that can customize them for their locale and business...

-

The spreadsheet produces forecasted annual EPS of $7.08. Identify one forecasting assumption (which affects forecasted EPS) that could be different and explain the alternative assumption. Provide...

-

In February 2009, Treasury 8.5s of 2020 yielded 3.2976% (see Figure 3.1). What was their price? If the yield rose to 4%, what would happen to the price? FIGURE 3.1 Sample Treasury bond quotes from...

-

2.24. (Sec. 2.4) Let (X,,Y,)',(X2, Y2)', (X3, Y3)' be independently distributed, (X, Y,)' according to Oxx Ozy i = 1,2,3. Oxy Oyy (a) Find the distribution of the six variables. (b) Find the...

-

3. Mr. Shanmugavel purchased (second hand) a machine for Rs. 8,000 on 1st April, 2001. He spent Rs. 3,500 on its overhaul and installation. Depreciation is written off @ 10% p.a. on the original...

-

Explain how "noise traders" can undermine the activity of arbitrageurs. Why is this important?

-

what does a social psychologist do under stressful situations?

-

How well do you think the group worked together? Give specific examples to back up your opinion. 2). What was your favorite role to fulfill within your group? Explain. 3) What was your least favorite...

-

Write the program in C++ with output result. i. Write a program to find factorial of number using recursion function. ii. Write a program that store 10 integers. The array and its size pass to a user...

-

PART A.1-Statement of Comprehensive Income Pet Training Company has shared the following details relating to 2023: Income from continuing operations (net of tax) During 2023, the company disposed of...

-

The senior management at Davis Watercraft would like to determine if it is possible to improve firm profitability by changing their existing product mix. Currently, the product mix is determined by...

-

Girard Corporation has just completed the acquisition of Williams, Inc., at a purchase price significantly higher than the fair values of the identifiable assets. Describe the audit issues caused by...

-

The following are typical questions that might appear on an internal control questionnaire for accounts payable. 1. Are monthly statements from vendors reconciled with the accounts payable listing?...

-

For each of the following brief scenarios, assume that you are reporting on a clients financial statements. Reply as to the type(s) of opinion possible for the scenario. In addition: Unless stated...

-

Sample size = 81, sample mean = 4.5 km, sample standard deviation = 3.1 km Assume that population means are to be estimated from the samples described. In each case, use the sample results to...

-

n = 100, x = 8.0 ft, s = 2.0 ft Assume that population means are to be estimated from the samples described. In each case, use the sample results to approximate the margin of error and 95% confidence...

-

Margin of error = \($5\), standard deviation = \($20\)

Study smarter with the SolutionInn App