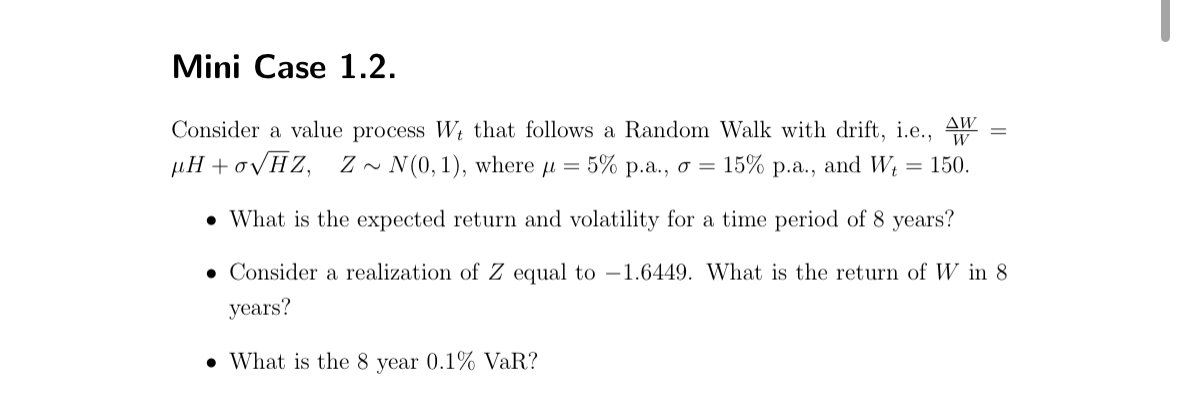

Question: Mini Case 1 . 2 . Consider a value process W t that follows a Random Walk with drift, i . e . , W

Mini Case

Consider a value process that follows a Random Walk with drift, ie

where pa pa and

What is the expected return and volatility for a time period of years?

Consider a realization of equal to What is the return of in

years?

What is the year VaR?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock