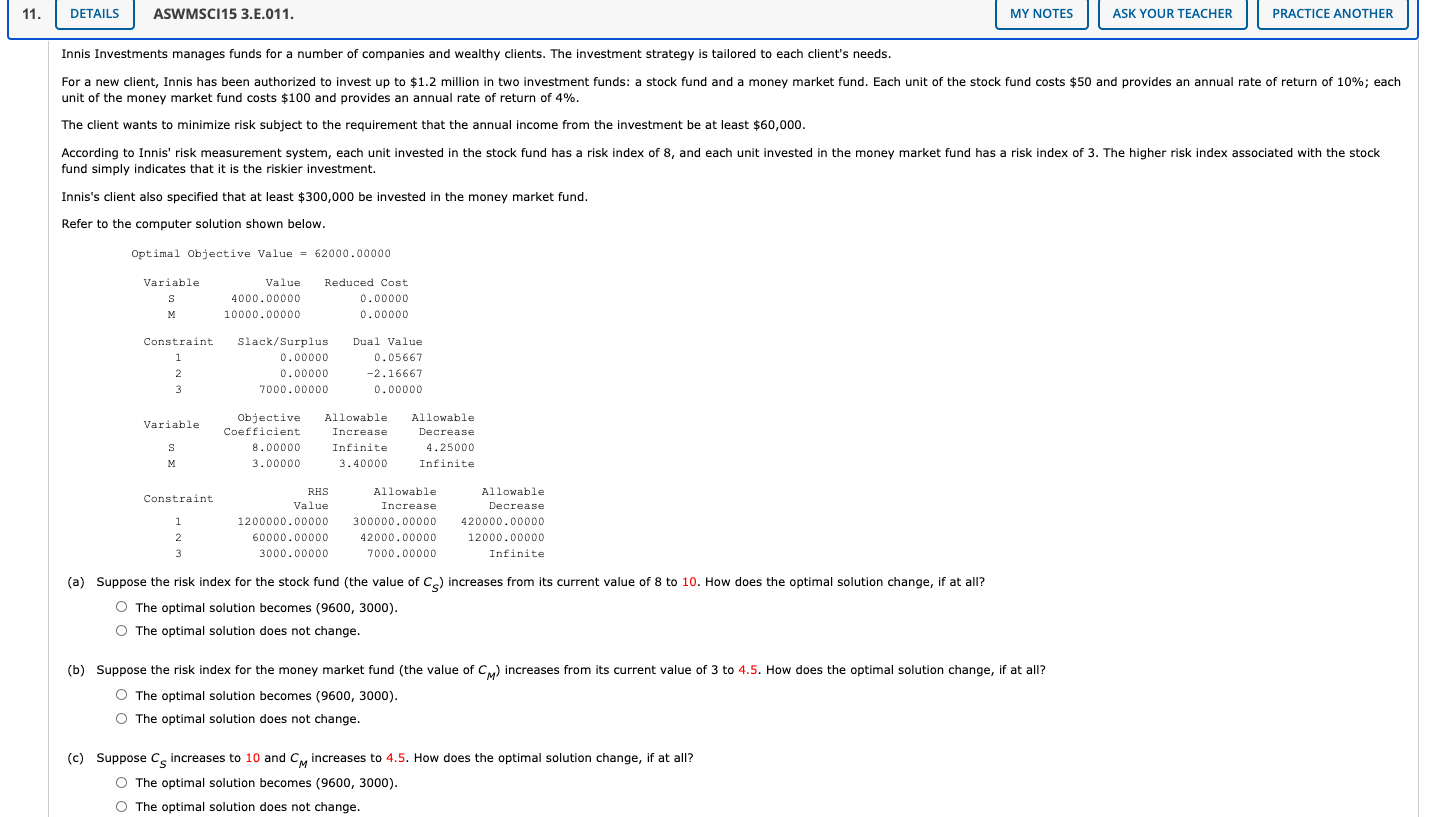

Question: Module 2: LP Sensitivity Analysis (QUESTION 11) 11. DETAILS ASWMSCI15 3.E.011. MY NOTES ASK YOUR TEACHER PRACTICE ANOTHER Innis Investments manages funds for a number

Module 2: LP Sensitivity Analysis (QUESTION 11)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock