Mr. Chuma is a company secretary with Metal Limited, a local company and was resident in Kenya

Question:

Mr. Chuma is a company secretary with Metal Limited, a local company and was resident in Kenya for the whole of 2005. The following extracts relate to information about his income and related benefits for 2005:

(i) Basic salary from Metal Limited was at the rate of Sh.50,000 per month up to 30 June 2005. It was raised to Sh.56,000 with effect from 1 July 2005.

(ii) The company made the following payments to him per month:

Home to office car allowance - Sh.3,000;

House allowance of Sh.10,000 (up to 30 June)

Sh.2,000 for making sales check trips.

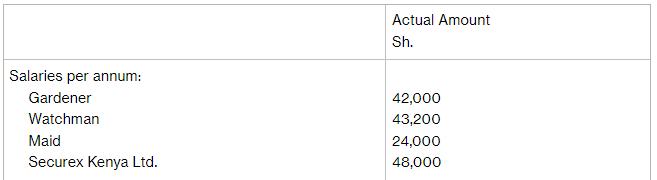

(iii) On 1 July he moved to a company house and paid a nominal rent of 5% of basic pay. The company, from that date, provided him with a gardener, a watchman, and a maid. In addition, his house was linked to Securex Kenya Ltd.'s 24-hour security alarm system.

The company incurred the following expenditure in respect of these benefits in 2005.

(iv) He rented his house to a tenant from 1 July for Sh.20,000 per month. The house was fully furnished when he rented it to the tenant. Furniture worth Sh.200,000 was acquired for this purpose. Other expenditure on the house included repairs of Sh.10,000 and mortgage interest. He had a mortgage of Sh.1,000,000 with H.F.C.K. Mortgage repayments were Sh.20,000 per month and interest rate was 20% p.a. Due to some cash flow problem he had only paid 9 instalments in the year.

(v) Dividend income (net) was Sh.9,000 from Metal Limited. He holds 4% of the share capital.

(vi) Mr. Chuma is a lawyer by profession and during their spare time they practice law with his wife, Mrs. Jane Chuma, also a lawyer. Due to unforeseen circumstances, they made a taxable loss of Sh.300,000 in 2005.

Mrs. Jane Chuman works for Metal Limited as personnel manager. Her basic salary was Sh.30,000 per month. In the year, she also received Sh.20,000 as a productivity bonus from the company. She obtained a loan of Sh.400,000 from the company repayable over 5 years at 10%. She immediately, on 21 January when she received the money invested it as follows:

Sh.100,000 in 15% Kenya Government Stock

Sh.100,000 in 12% Post Office Savings Account

Sh.200,000 in 20% Golden Premium Account with KCB.

She also received Sh.4,500 net dividend from Dress Making Limited.

Mr. Chuma was in the company's life insurance scheme into which the company paid Sh.5,000 p.a. Mrs. Chuma's life cover was of her own and she paid Sh.6,000 p.a.

On 1 December, after some serious disagreement, Mr and Mrs. Chuma were permanently separated by the court. Mrs. Jane Chuma received custody of their child, Juma and an alimony of Sh.20,000 per month. The legal practice was to continue on an equal sharing basis. PAYE paid at source was, Mr. Chuma sh.72,000 and Mrs. Chuma Sh.60,000, respectively.

Required:

Mr and Mrs. Chuma's tax liability for 2005, commenting on the effects of their separation.

Expert Answer:

To calculate the tax liability for Mr and Mrs Chuma for the year 2005 we need to consider their respective sources of income deductions and credits Il... View the full answer

South-Western Federal Taxation 2018 Comprehensive

ISBN: 9781337386005

41st Edition

Authors: David M. Maloney, William H. Hoffman, Jr., William A. Raabe, James C. Young