Mr Mike, a CFA charter holder (fund manager), recently met with one of his clients. Mr Mike

Question:

Mr Mike, a CFA charter holder (fund manager), recently met with one of his clients. Mr Mike typically invests in a master list of 20 equities drawn from several industries. As the meeting concluded, the client made the following statement: 'I trust your stock-picking ability and believe that you should invest my funds in your five best ideas.' Why invest in 20 companies when you obviously have stronger opinions on a few of them? Mr Mike to respond to his client within the context of modern portfolio theory.

- Contrast the concepts of market risk and total risk measured by standard deviation and give an example of each type of risk within the context given above. Discuss how both systematic and total risk change as the number of securities in a portfolio is increased.

Part 2)

Suppose that there are many shares in the security market and that the characteristics of shares A and B are given as follows:

| Share | Expected return | Standard Deviation |

| A | 12% | 5% |

| B | 14% | 10% |

| correlation | -1 |

- Can you form a portfolio with a zero risk assuming that investing equally. If it is what must be the value of risk-free rate (portfolio with zero risk?)

- Discuss the importance of correlation coefficient in the construction of portfolio risk diversification.

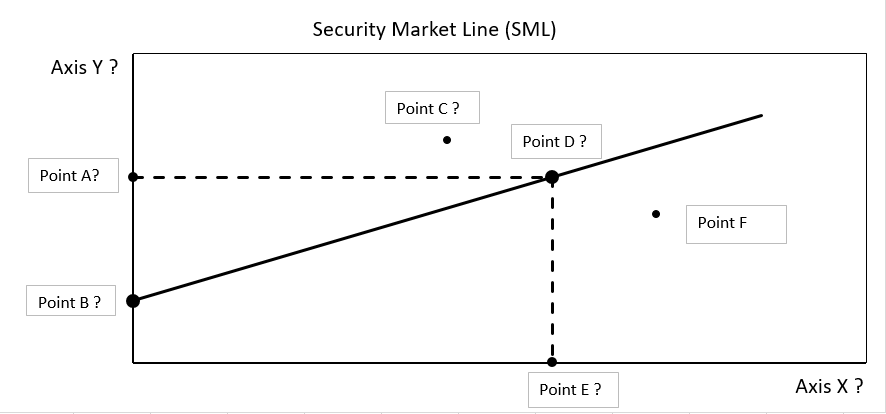

Question 2

The market portfolio (M) provides a 15% annual return with a 20% standard deviation. The risk-free rate of return (rf) is 5% per annum. Security Q and P provide 17% and 11% return per annum and their betas are 1.2 and 0.8 respectively. Based on this information Mr Ali drew the following graph of Security Market Line (SML) to identify any mispricing of security Q and P in the market.Unfortunately, Jenny forgot to label her graph. Help her label the following graph.

Expert Answer: