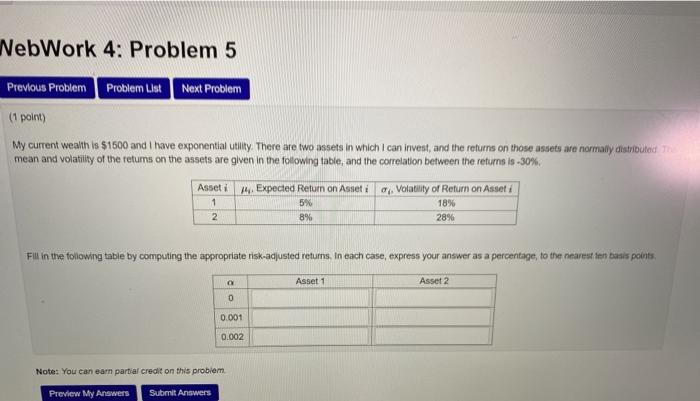

Question: NebWork 4: Problem 5 Previous Problem Problem List Next Problem (1 point) My current wealth is $1500 and I have exponential utility. There are two

NebWork 4: Problem 5 Previous Problem Problem List Next Problem (1 point) My current wealth is $1500 and I have exponential utility. There are two assets in which I can invest, and the returns on those assets are normally distributed mean and volatility of the returns on the assets are given in the following table, and the correlation between the returns is -30% 14. Expected Return on Asset Volatility of Return on Asset i Asset i 1 2 5% 8% 18% 28% Fill in the following table by computing the appropriate risk-adjusted returns in each case, express your answer as a percentage, to the nearest tenuis points, Asset 1 Asset 2 0 0.001 0.002 Note: You can earn partial credit on this problem Preview My Answers Submit Answers NebWork 4: Problem 5 Previous Problem Problem List Next Problem (1 point) My current wealth is $1500 and I have exponential utility. There are two assets in which I can invest, and the returns on those assets are normally distributed mean and volatility of the returns on the assets are given in the following table, and the correlation between the returns is -30% 14. Expected Return on Asset Volatility of Return on Asset i Asset i 1 2 5% 8% 18% 28% Fill in the following table by computing the appropriate risk-adjusted returns in each case, express your answer as a percentage, to the nearest tenuis points, Asset 1 Asset 2 0 0.001 0.002 Note: You can earn partial credit on this problem Preview My Answers Submit Answers

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts