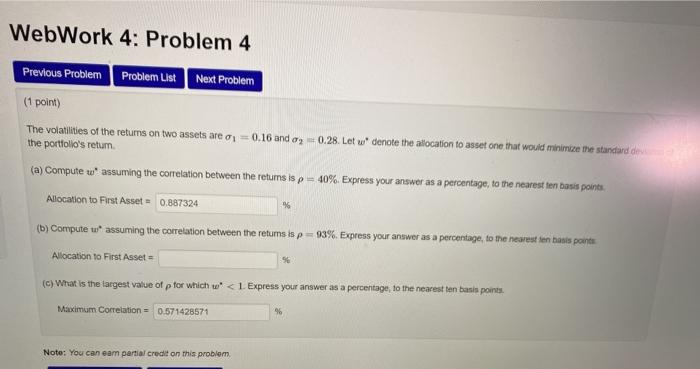

Question: WebWork 4: Problem 4 Previous Problem Problem List Next Problem (1 point) The volatilities of the returns on two assets are on = 0.16 and

WebWork 4: Problem 4 Previous Problem Problem List Next Problem (1 point) The volatilities of the returns on two assets are on = 0.16 and ag 0.28. Let u denote the allocation to asset one that would minimize the standard de the portfolio's retum (a) Compute w' assuming the correlation between the returns is p = 40%. Express your answer as a percentage, to the nearest ten basis points Allocation to First Asset = 0.887324 (b) Compute t assuming the correlation between the retums is p = 93%. Express your answer as a percentage, to the nearest en tants pants Allocation to First Asset (c) What is the largest value of p for which w'

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock