Question: need an explanation the correct answer is already there Golden Bank currently offers traditional banking services, from which they generate an average return of 6%

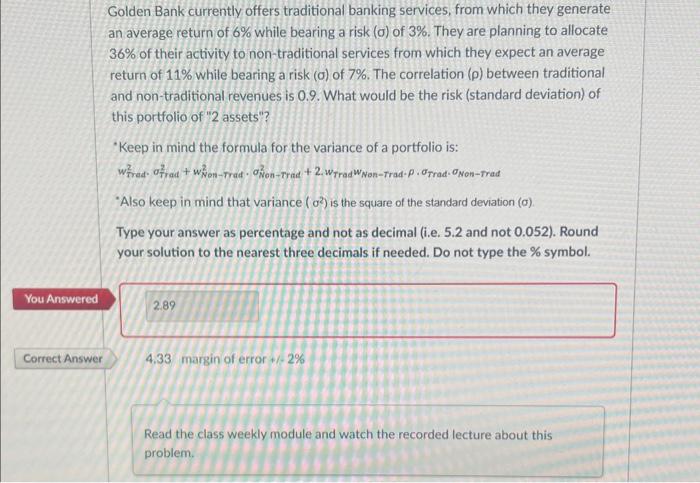

Golden Bank currently offers traditional banking services, from which they generate an average return of 6% while bearing a risk (o) of 3%. They are planning to allocate 36% of their activity to non-traditional services from which they expect an average return of 11% while bearing a risk ( ) of 7%. The correlation ( ) between traditional and non-traditional revenues is 0.9. What would be the risk (standard deviation) of this portfolio of " 2 assets"? 'Keep in mind the formula for the variance of a portfolio is: wTrad:2Trad2+wNon-Trad2Non-rrad2+2wTradwNon-TradTradNon-trad - Also keep in mind that variance (2) is the square of the standard deviation (). Type your answer as percentage and not as decimal (i.e. 5.2 and not 0.052 ). Round your solution to the nearest three decimals if needed. Do not type the % symbol. 4.33 margin of error +1.2% Read the class weekly module and watch the recorded lecture about this

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts