Question: need hand writing 3. (20 points) Consider the binomial asset pricing model. Assume the stock's current price is S0=4, the up factor u=2, the down

need hand writing

need hand writing

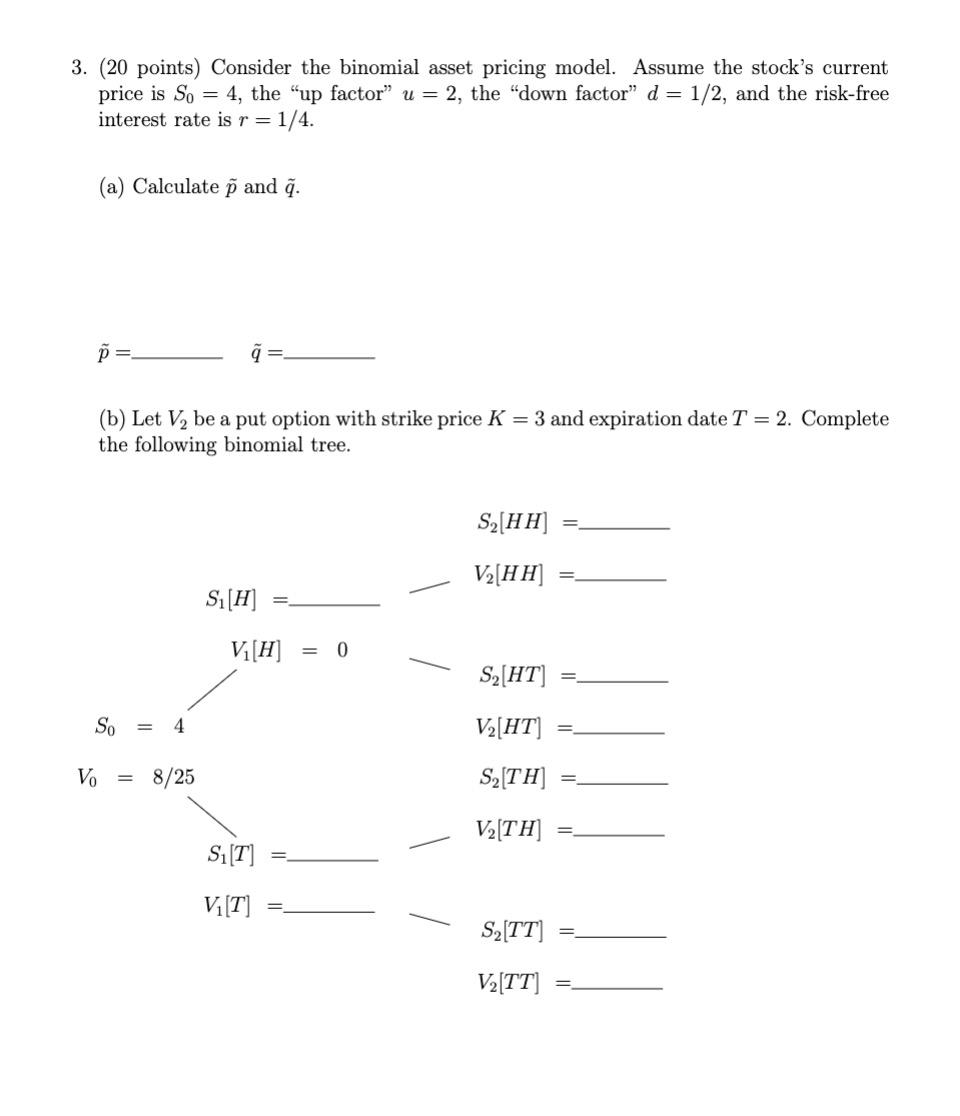

3. (20 points) Consider the binomial asset pricing model. Assume the stock's current price is S0=4, the "up factor" u=2, the "down factor" d=1/2, and the risk-free interest rate is r=1/4. (a) Calculate p~ and q~. p~=q~= (b) Let V2 be a put option with strike price K=3 and expiration date T=2. Complete the following binomial tree. S2[HH]=S1[H]=V2[HH]=S0=4V1[H]=0S2[HT]=V0=8/25V2[HT]=S1[T]=S2[TH]=V1[T]=V2[TH]=S2[TT]=V2[TT]=

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock