Question: need help with #5 need help with 5.c** 5. A mutual fund manager holds the following portfolio: Stock Beta 1 2 Investment $ 2 million

need help with #5

need help with 5.c**

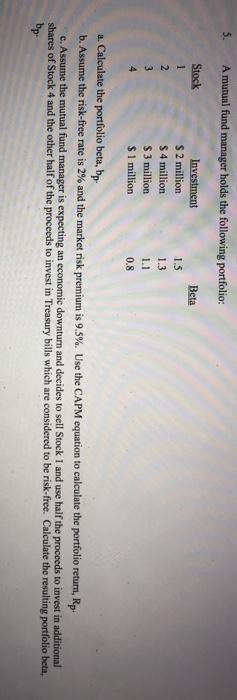

5. A mutual fund manager holds the following portfolio: Stock Beta 1 2 Investment $ 2 million $ 4 million $ 3 million $ 1 million 1.5 1.3 1.1 0.8 3 4 a. Calculate the portfolio beta, bp- b. Assume the risk-free rate is 2% and the market risk premium is 9.5%. Use the CAPM equation to calculate the portfolio return, Rp. c. Assume the mutual fund manager is expecting an economic downturn and decides to sell Stock I and use half the proceeds to invest in additional shares of Stock 4 and the other half of the proceeds to invest in Treasury bills which are considered to be risk-free. Calculate the resulting portfolio beta, bp

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock