Question: need help with both please. Question 18 (4 points) The current spot exchange rate is $1.8350/ and the three-month forward rate is $1.8662/. You enter

need help with both please.

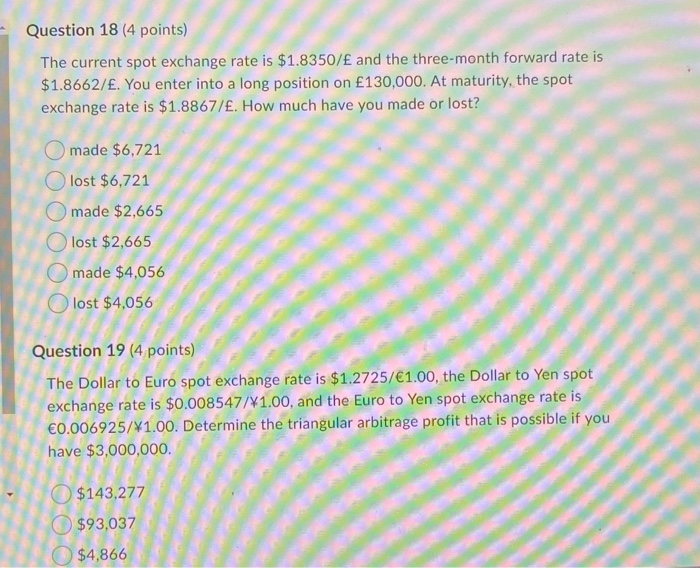

Question 18 (4 points) The current spot exchange rate is $1.8350/ and the three-month forward rate is $1.8662/. You enter into a long position on 130,000. At maturity, the spot exchange rate is $1.8867/. How much have you made or lost? O made $6,721 Olost $6,721 O made $2,665 Olost $2,665 O made $4,056 lost $4,056 Question 19 (4 points) The Dollar to Euro spot exchange rate is $1.2725/1.00, the Dollar to Yen spot exchange rate is $0.008547/41.00, and the Euro to Yen spot exchange rate is 0.006925/1.00. Determine the triangular arbitrage profit that is possible if you have $3,000,000. $143,277 $93,037 $4,866

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock