Question: need help with part b only Question 5 (7 marks) Consider the following futures contact prices for crude oil: 1 year 2 years Maturity Futures

need help with part b only

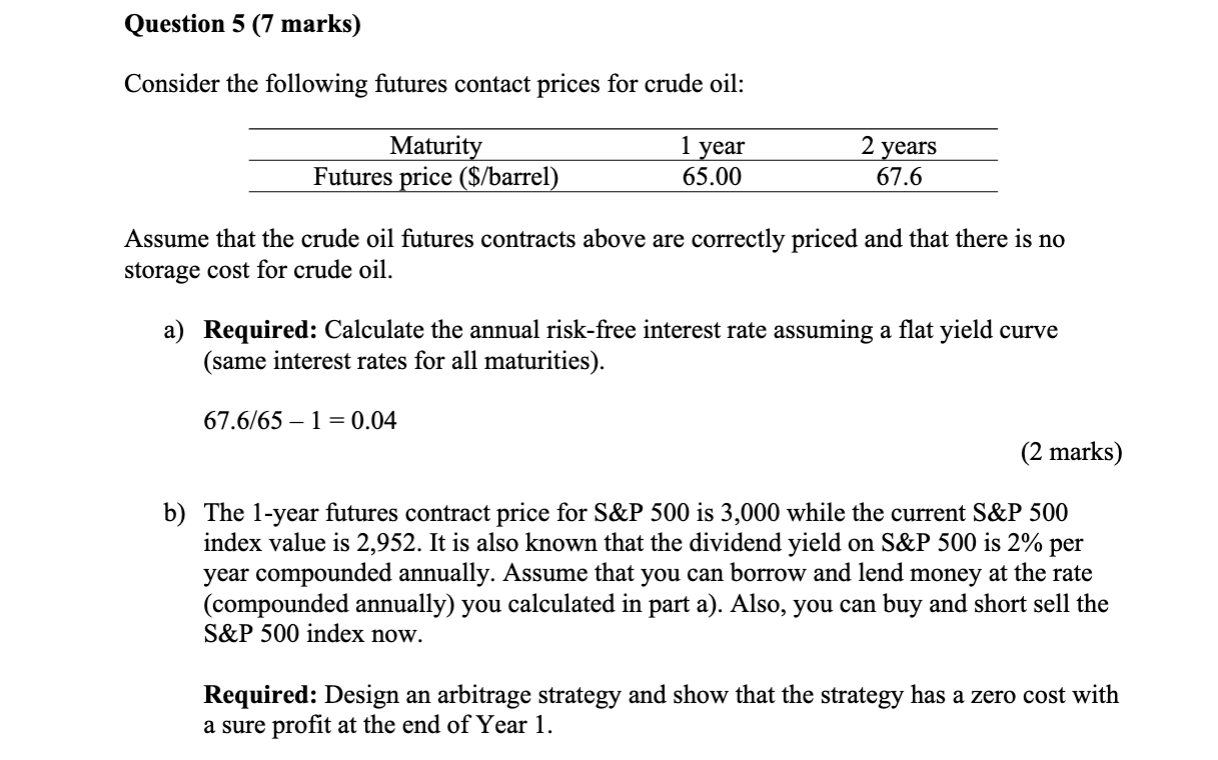

Question 5 (7 marks) Consider the following futures contact prices for crude oil: 1 year 2 years Maturity Futures price ($/barrel) 65.00 67.6 Assume that the crude oil futures contracts above are correctly priced and that there is no storage cost for crude oil. a) Required: Calculate the annual risk-free interest rate assuming a flat yield curve (same interest rates for all maturities). 67.6/65-1 = 0.04 (2 marks) b) The 1-year futures contract price for S&P 500 is 3,000 while the current S&P 500 index value is 2,952. It is also known that the dividend yield on S&P 500 is 2% per year compounded annually. Assume that you can borrow and lend money at the rate (compounded annually) you calculated in part a). Also, you can buy and short sell the S&P 500 index now. Required: Design an arbitrage strategy and show that the strategy has a zero cost with a sure profit at the end of Year 1. Question 5 (7 marks) Consider the following futures contact prices for crude oil: 1 year 2 years Maturity Futures price ($/barrel) 65.00 67.6 Assume that the crude oil futures contracts above are correctly priced and that there is no storage cost for crude oil. a) Required: Calculate the annual risk-free interest rate assuming a flat yield curve (same interest rates for all maturities). 67.6/65-1 = 0.04 (2 marks) b) The 1-year futures contract price for S&P 500 is 3,000 while the current S&P 500 index value is 2,952. It is also known that the dividend yield on S&P 500 is 2% per year compounded annually. Assume that you can borrow and lend money at the rate (compounded annually) you calculated in part a). Also, you can buy and short sell the S&P 500 index now. Required: Design an arbitrage strategy and show that the strategy has a zero cost with a sure profit at the end of Year 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts