Question: Need help with part B through I 7. Consider zero-coupon bonds with face value $1. The price for 1-year, 2-year, 3-year, 4-year, and 5-year bonds

Need help with part B through I

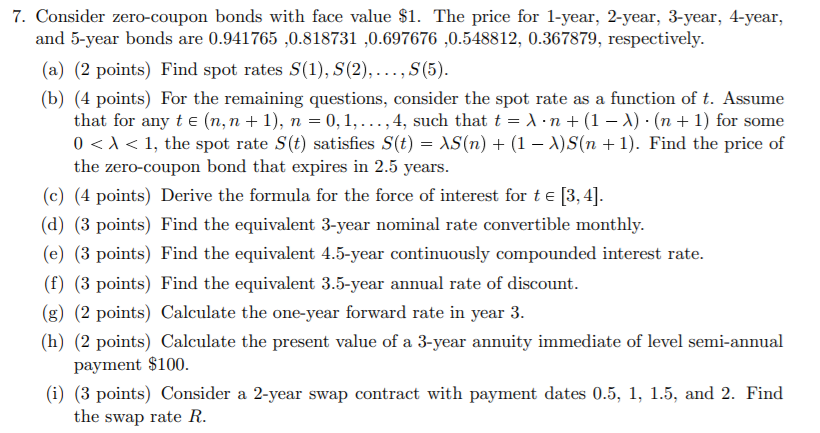

7. Consider zero-coupon bonds with face value $1. The price for 1-year, 2-year, 3-year, 4-year, and 5-year bonds are 0.941765 ,0.818731 ,0.697676 ,0.548812, 0.367879, respectively. (a) (2 points) Find spot rates S(1), S(2), ...,S(5). (b) (4 points) For the remaining questions, consider the spot rate as a function of t. Assume that for any ten, n +1), n = 0,1,...,4, such that t = ln + (1 - 1)(n+1) for some 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock