Question: need quick response I will give you like for correct answer thank you Edit Pictures.. Sa Auto Correct Shortcuts. DBX X 91% Probability 0.35 State

need quick response I will give you like for correct answer thank you

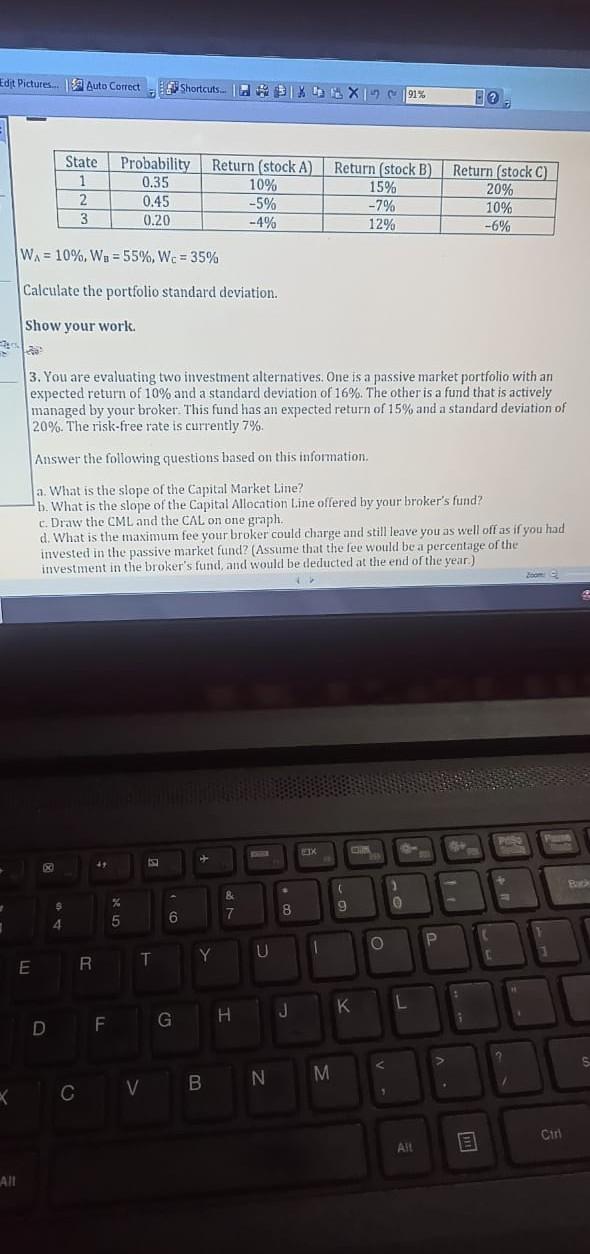

Edit Pictures.. Sa Auto Correct Shortcuts. DBX X 91% Probability 0.35 State 1 2. 3 Return (stock A 10% -5% -4% 0.45 Return (stock B) 15% -7% 12% Return (stock C) 20% 10% -6% 0.20 WA = 10%, W. = 55%, Wc = 35% Calculate the portfolio standard deviation. Show your work. 3. You are evaluating two investment alternatives. One is a passive market portfolio with an expected return of 10% and a standard deviation of 16%. The other is a fund that is actively managed by your broker. This fund has an expected return of 15% and a standard deviation of 20%. The risk-free rate is currently 7% Answer the following questions based on this information. a. What is the slope of the Capital Market Line? b. What is the slope of the Capital Allocation Line offered by your broker's fund? c.Draw the CML and the CAL on one graph. d. What is the maximum fee your broker could charge and still leave you as well off as if you had invested in the passive market fund? (Assume that the fee would be a percentage of the investment in the broker's fund, and would be deducted at the end of the year.) pese 3 0 & 7 $ 4 % 5 9 8 6 U 1 O Y T E R K L J F H G D S M N B C V Cir Aft All

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts