Question: No information about Beta o standard deviation, only the weight for risky and riskless asset 2) POINTS 12: Suppose an economy is characterized by two

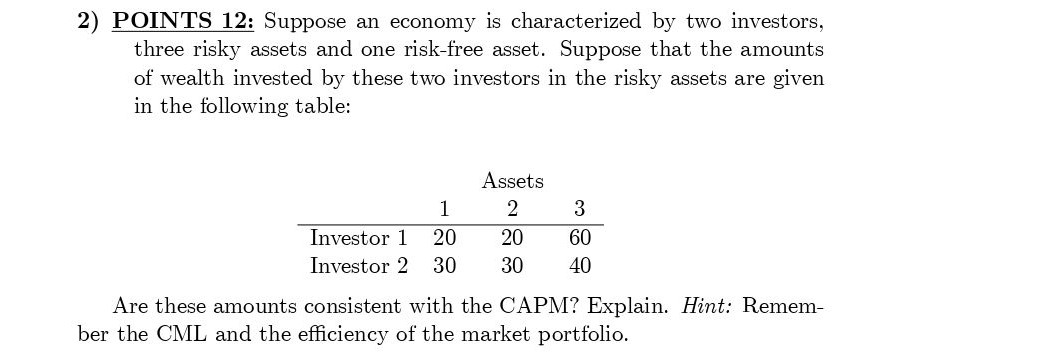

2) POINTS 12: Suppose an economy is characterized by two investors, three risky assets and one risk-free asset. Suppose that the amounts of wealth invested by these two investors in the risky assets are given in the following table: 1 3 Assets 2 20 30 Investor 1 20 Investor 2 30 60 40 Are these amounts consistent with the CAPM? Explain. Hint: Remem- ber the CML and the efficiency of the market portfolio. 2) POINTS 12: Suppose an economy is characterized by two investors, three risky assets and one risk-free asset. Suppose that the amounts of wealth invested by these two investors in the risky assets are given in the following table: 1 3 Assets 2 20 30 Investor 1 20 Investor 2 30 60 40 Are these amounts consistent with the CAPM? Explain. Hint: Remem- ber the CML and the efficiency of the market portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts