Question: non-invertible moving average process Problem 4, 20pts: non-invertible moving average process Let {Xt} be the (non-invertible) MA(1) process Xt = Z+ + 0Zt-1, {Zt} ~

non-invertible moving average process

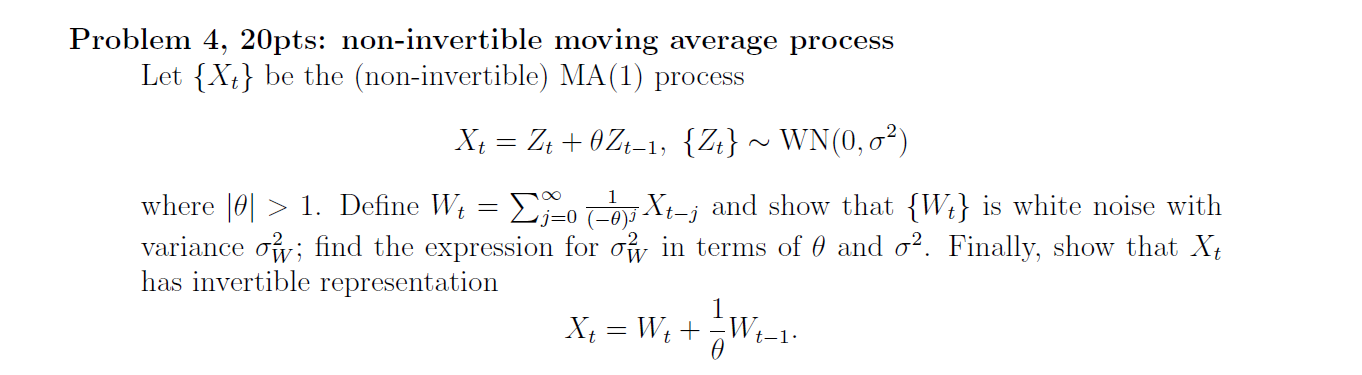

Problem 4, 20pts: non-invertible moving average process Let {Xt} be the (non-invertible) MA(1) process Xt = Z+ + 0Zt-1, {Zt} ~ WN(0, 62) where |0| > 1. Define Wt = 2j=o (-0)7- Xt-j and show that {Wt} is white noise with variance ow; find the expression for ow in terms of 0 and o2. Finally, show that Xt has invertible representation 1 Xt = Wt+ -Wt-1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock