Question: Note: Please keep four decimal points in your final results and two decimal points for percentage numbers unless otherwise specified. 1. Compute the 95% 1-month

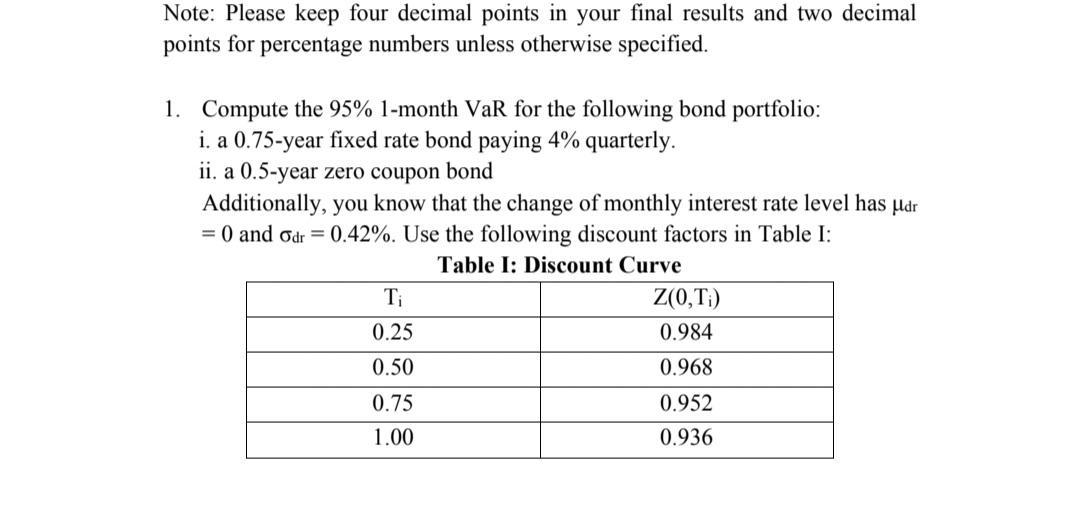

Note: Please keep four decimal points in your final results and two decimal points for percentage numbers unless otherwise specified. 1. Compute the 95% 1-month VaR for the following bond portfolio: i. a 0.75-year fixed rate bond paying 4% quarterly. ii. a 0.5-year zero coupon bond Additionally, you know that the change of monthly interest rate level has udr = 0 and Odr = 0.42%. Use the following discount factors in Table I: Table I: Discount Curve T Z(0,T;) 0.25 0.984 0.50 0.968 0.75 0.952 0.936 1.00 Note: Please keep four decimal points in your final results and two decimal points for percentage numbers unless otherwise specified. 1. Compute the 95% 1-month VaR for the following bond portfolio: i. a 0.75-year fixed rate bond paying 4% quarterly. ii. a 0.5-year zero coupon bond Additionally, you know that the change of monthly interest rate level has udr = 0 and Odr = 0.42%. Use the following discount factors in Table I: Table I: Discount Curve T Z(0,T;) 0.25 0.984 0.50 0.968 0.75 0.952 0.936 1.00

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts