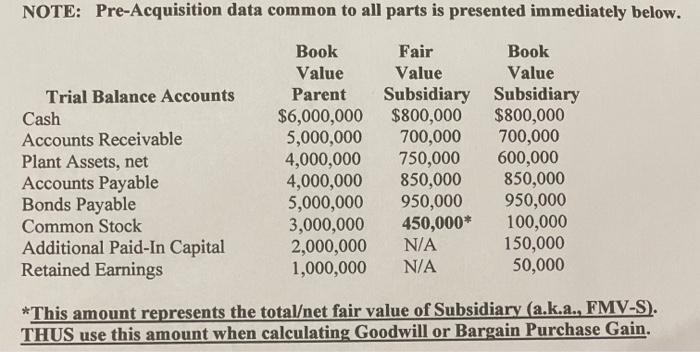

Question: NOTE: Pre-Acquisition data common to all parts is presented immediately below. Trial Balance Accounts Cash Accounts Receivable Plant Assets, net Accounts Payable Bonds Payable Common

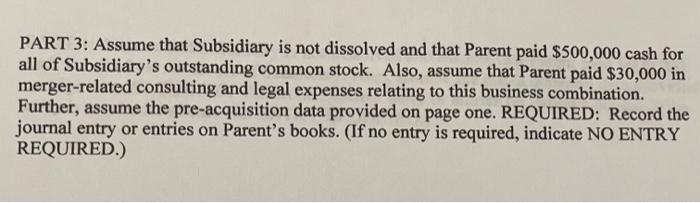

NOTE: Pre-Acquisition data common to all parts is presented immediately below. Trial Balance Accounts Cash Accounts Receivable Plant Assets, net Accounts Payable Bonds Payable Common Stock Additional Paid-In Capital Retained Earnings Book Value Parent $6,000,000 5,000,000 4,000,000 4,000,000 5,000,000 3,000,000 2,000,000 1,000,000 Fair Book Value Value Subsidiary Subsidiary $800,000 $800,000 700,000 700,000 750,000 600,000 850,000 850,000 950,000 950,000 450,000* 100,000 N/A 150,000 N/A 50,000 *This amount represents the totalet fair value of Subsidiary (a.k.a., FMV-S). THUS use this amount when calculating Goodwill or Bargain Purchase Gain. PART 3: Assume that Subsidiary is not dissolved and that Parent paid $500,000 cash for all of Subsidiary's outstanding common stock. Also, assume that Parent paid $30,000 in merger-related consulting and legal expenses relating to this business combination. Further, assume the pre-acquisition data provided on page one. REQUIRED: Record the journal entry or entries on Parent's books. (If no entry is required, indicate NO ENTRY REQUIRED.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts