Question: NOTE: SHOW YOUR SOLUTION MANUAL AND IN MS EXCEL Exercise Given a portfolio with only 2 assets, assets 1 & 2, with a 50/50 weighting

NOTE: SHOW YOUR SOLUTION MANUAL AND IN MS EXCEL

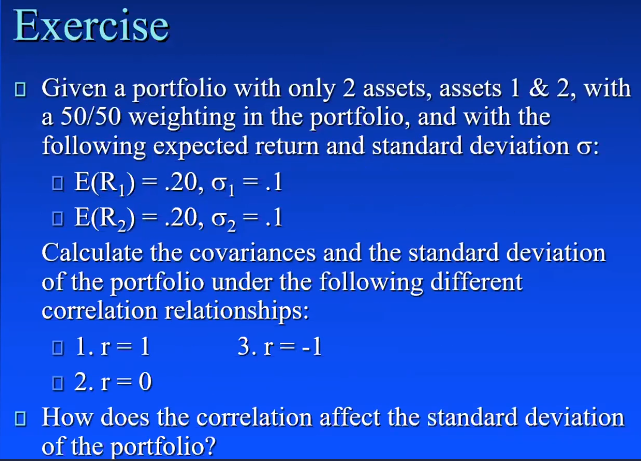

Exercise Given a portfolio with only 2 assets, assets 1 & 2, with a 50/50 weighting in the portfolio, and with the following expected return and standard deviation o: O E(R) = .20, 0 =.1 O E(R2) = .20, 02= .1 Calculate the covariances and the standard deviation of the portfolio under the following different correlation relationships: 01. r= 1 3. r=-1 2. r= 0 O How does the correlation affect the standard deviation of the portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock