Question: Note : You need to write your own spreadsheet programs . You can adopt the basic format of the sample Black-Scholes OPM and modify the

Note: You need to write your own spreadsheet programs. You can adopt the basic format of the sample Black-Scholes OPM and modify the inputs and parameters according to the given formulae. You work out with the pricing model only. (No sensitivity analysis or charts needed.)

Use the attached written out answer and use above instructions to create spreadsheet model.

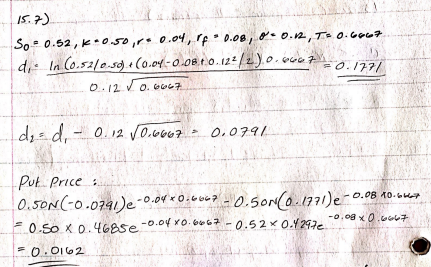

15.7) So - 0.52, k *0.50,-. 0.04, 10.08, p=0.12, T0.6667 1) d. In (0.52/0-59) +(0.04 -0.081.0.122/2).0.6667 0:12 0.6667 =0./77/ de-d, -0.12.10.6001. 0.0791 put. Price 0.50N (-0.0741)e-0.04 * 0.6667 - 0,50N (0.1771)e-0. - 0.500(0.1771)e-0.08 10.com 0.50 X 0.4685e -0.04x0.6467 -7 -0.520.42970 50.0162 -0.ogx 0.6667 15.7) So - 0.52, k *0.50,-. 0.04, 10.08, p=0.12, T0.6667 1) d. In (0.52/0-59) +(0.04 -0.081.0.122/2).0.6667 0:12 0.6667 =0./77/ de-d, -0.12.10.6001. 0.0791 put. Price 0.50N (-0.0741)e-0.04 * 0.6667 - 0,50N (0.1771)e-0. - 0.500(0.1771)e-0.08 10.com 0.50 X 0.4685e -0.04x0.6467 -7 -0.520.42970 50.0162 -0.ogx 0.6667

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts