Question: Nothing is missing, this is the information for this task Consider US investors who invest only in the domestic (US) stock market portfolio. The mean

Nothing is missing, this is the information for this task

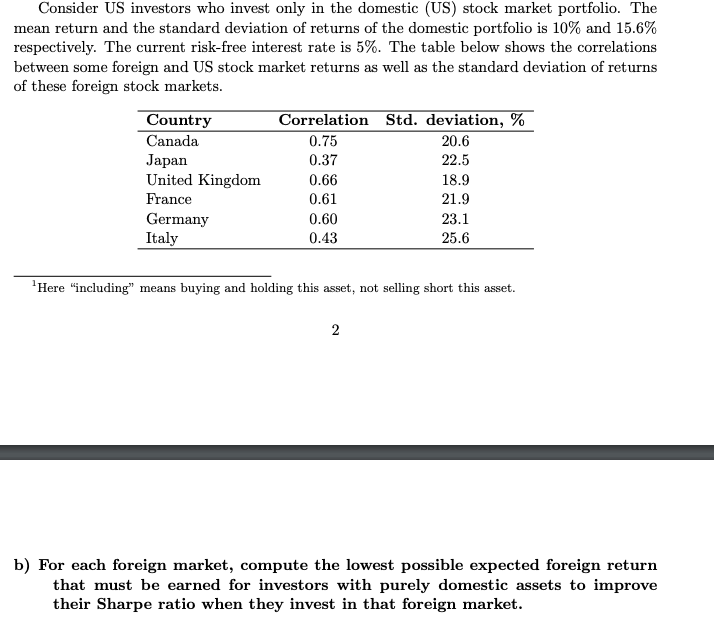

Consider US investors who invest only in the domestic (US) stock market portfolio. The mean return and the standard deviation of returns of the domestic portfolio is 10% and 15.6% respectively. The current risk-free interest rate is 5%. The table below shows the correlations between some foreign and US stock market returns as well as the standard deviation of returns of these foreign stock markets. Country Correlation Std. deviation, % Canada 0.75 20.6 Japan 0.37 22.5 United Kingdom 0.66 18.9 France 0.61 21.9 Germany 0.60 23.1 Italy 0.43 25.6 Here "including" means buying and holding this asset, not selling short this asset. 2 b) For each foreign market, compute the lowest possible expected foreign return that must be earned for investors with purely domestic assets to improve their Sharpe ratio when they invest in that foreign market

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts