On 1 July 2019, Parker purchased 85% of Skyklar by way of a share exchange of one

Question:

On 1 July 2019, Parker purchased 85% of Skyklar by way of a share exchange of one new share in Parker for every two purchased in Skylar plus an immediate cash payment of $ 10.4 million. Parker’s share price at the acquisition date was $ 5. Only the cash element of the consideration has been recorded by Parker.

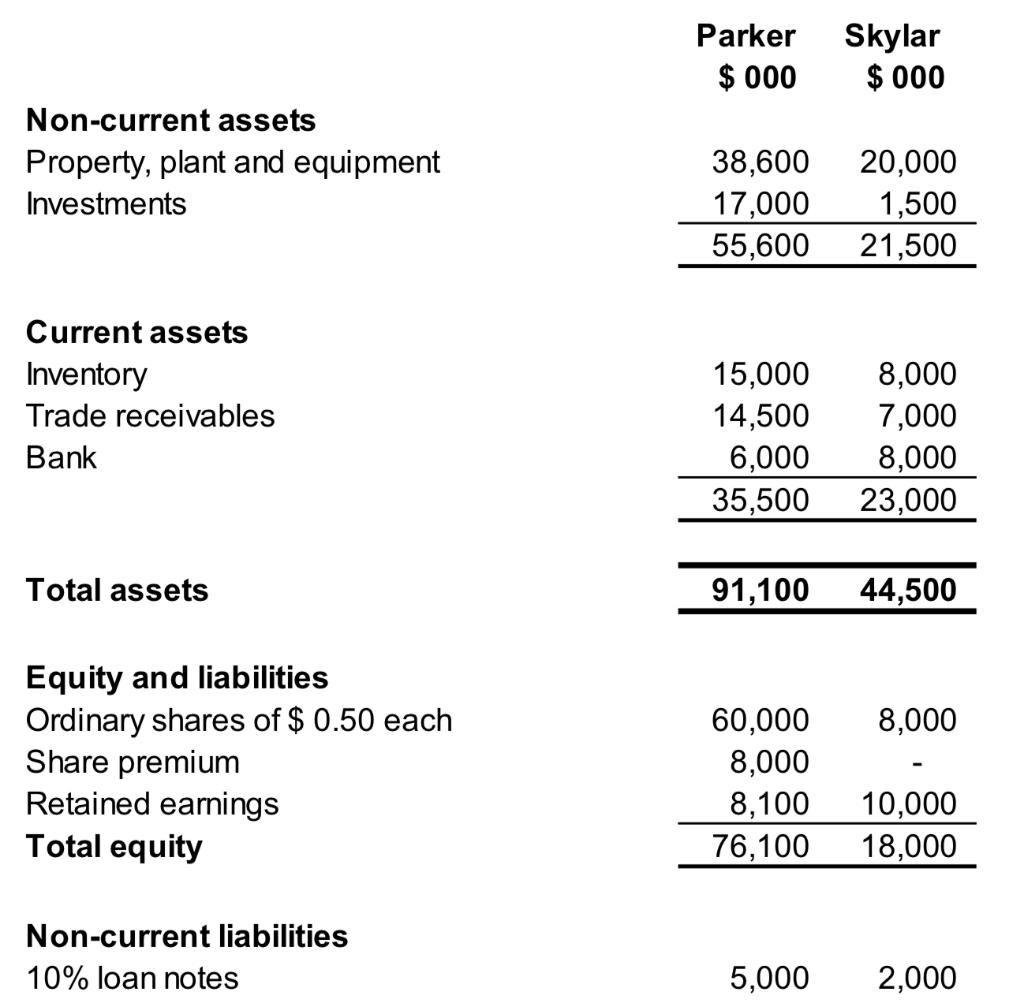

The Statement of Financial Positions of both companies as of 30 June 2020 are as follows:

The following information is relevant:

Skylar’s retained earnings at the date of acquisition were $ 3.8 million.

Parker’s policy is to value the non-controlling interest at fair value at the date of acquisition. The share price of Skyklar at the date of acquisition was $ 3.

An impairment test carried out on 30 June 2020 revealed that consolidated goodwill was impaired by $ 2 million.

Skylar sold goods to Parker in the post-acquisition period at a markup of 25% for $ 20 million and 1/4 of these goods are included in the inventory of Parker at 30 June 2020.

Parker’s trade payables of $ 3 million do not tally with Skylar’s trade receivables due to cash in transit of $ 1 million from Parker to Skylar.

The fair value of Skylar’s net assets differed from its carrying values on 1 July 2019. The plant had a fair value of $ 6 million in excess of its net book value and would create additional depreciation of $ 1.5 million in the post-acquisition period to 30 June 2020.

REQUIRED

Prepare the consolidated statement of the financial position of Parker as at 30 June 2020.

Expert Answer:

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott