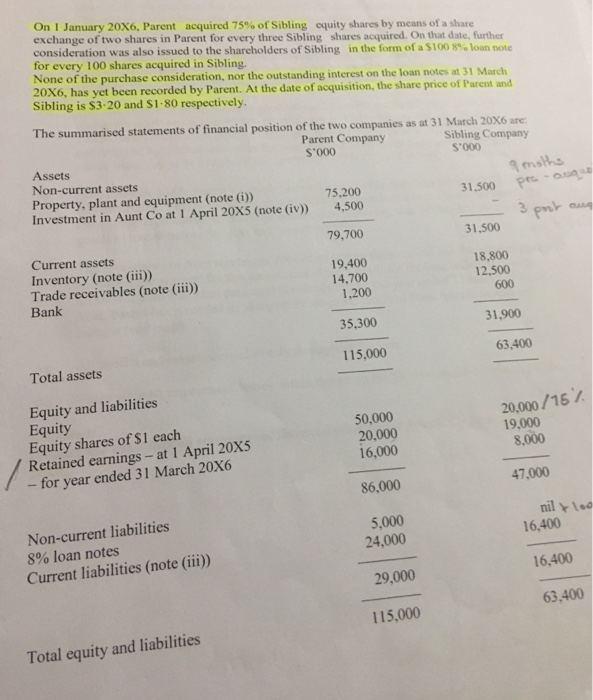

On 1 January 20X6, Parent acquired 75% of Sibling equity shares by means of a share...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

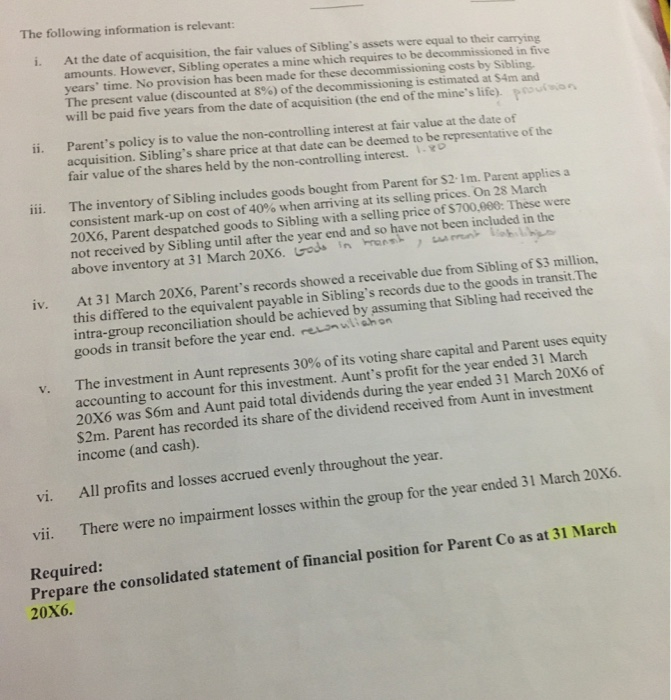

On 1 January 20X6, Parent acquired 75% of Sibling equity shares by means of a share exchange of two shares in Parent for every three Sibling shares acquired. On that date, further consideration was also issued to the shareholders of Sibling in the form of a $100 8% loan note for every 100 shares acquired in Sibling. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Parent. At the date of acquisition, the share price of Parent and Sibling is $3-20 and $1-80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: Parent Company Sibling Company $'000 $'000 Assets Non-current assets Property, plant and equipment (note (i)) Investment in Aunt Co at 1 April 20X5 (note (iv)) Current assets Inventory (note (iii)) Trade receivables (note (iii)) Bank Total assets Equity and liabilities Equity Equity shares of $1 each Retained earnings - at 1 April 20X5 for year ended 31 March 20X6 Non-current liabilities 8% loan notes Current liabilities (note (iii)) Total equity and liabilities 75,200 4,500 79,700 19,400 14,700 1,200 35,300 115,000 50,000 20,000 16,000 86,000 5,000 24,000 29,000 115,000 31,500 31,500 18,800 12,500 600 moths pre-auque 3 31,900 63,400 prot aug 20,000/15/ 19,000 8,000 47,000 nillo 16,400 16,400 63,400 The following information is relevant: i. At the date of acquisition, the fair values of Sibling's assets were equal to their carrying amounts. However, Sibling operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Sibling. The present value (discounted at 8%) of the decommissioning is estimated at $4m and will be paid five years from the date of acquisition (the end of the mine's life). prouision ii. iii. iv. V. vi. vii. Parent's policy is to value the non-controlling interest at fair value at the date of acquisition. Sibling's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. 1.0 The inventory of Sibling includes goods bought from Parent for S2-1m. Parent applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Parent despatched goods to Sibling with a selling price of $700,000: These were not received by Sibling until after the year end and so have not been included in the above inventory at 31 March 20X6. Gods in trans > current At 31 March 20X6, Parent's records showed a receivable due from Sibling of $3 million, this differed to the equivalent payable in Sibling's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Sibling had received the goods in transit before the year end. renuliahon The investment in Aunt represents 30% of its voting share capital and Parent uses equity accounting to account for this investment. Aunt's profit for the year ended 31 March 20X6 was $6m and Aunt paid total dividends during the year ended 31 March 20X6 of $2m. Parent has recorded its share of the dividend received from Aunt in investment income (and cash). All profits and losses accrued evenly throughout the year. There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Parent Co as at 31 March 20X6. On 1 January 20X6, Parent acquired 75% of Sibling equity shares by means of a share exchange of two shares in Parent for every three Sibling shares acquired. On that date, further consideration was also issued to the shareholders of Sibling in the form of a $100 8% loan note for every 100 shares acquired in Sibling. None of the purchase consideration, nor the outstanding interest on the loan notes at 31 March 20X6, has yet been recorded by Parent. At the date of acquisition, the share price of Parent and Sibling is $3-20 and $1-80 respectively. The summarised statements of financial position of the two companies as at 31 March 20X6 are: Parent Company Sibling Company $'000 $'000 Assets Non-current assets Property, plant and equipment (note (i)) Investment in Aunt Co at 1 April 20X5 (note (iv)) Current assets Inventory (note (iii)) Trade receivables (note (iii)) Bank Total assets Equity and liabilities Equity Equity shares of $1 each Retained earnings - at 1 April 20X5 for year ended 31 March 20X6 Non-current liabilities 8% loan notes Current liabilities (note (iii)) Total equity and liabilities 75,200 4,500 79,700 19,400 14,700 1,200 35,300 115,000 50,000 20,000 16,000 86,000 5,000 24,000 29,000 115,000 31,500 31,500 18,800 12,500 600 moths pre-auque 3 31,900 63,400 prot aug 20,000/15/ 19,000 8,000 47,000 nillo 16,400 16,400 63,400 The following information is relevant: i. At the date of acquisition, the fair values of Sibling's assets were equal to their carrying amounts. However, Sibling operates a mine which requires to be decommissioned in five years' time. No provision has been made for these decommissioning costs by Sibling. The present value (discounted at 8%) of the decommissioning is estimated at $4m and will be paid five years from the date of acquisition (the end of the mine's life). prouision ii. iii. iv. V. vi. vii. Parent's policy is to value the non-controlling interest at fair value at the date of acquisition. Sibling's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. 1.0 The inventory of Sibling includes goods bought from Parent for S2-1m. Parent applies a consistent mark-up on cost of 40% when arriving at its selling prices. On 28 March 20X6, Parent despatched goods to Sibling with a selling price of $700,000: These were not received by Sibling until after the year end and so have not been included in the above inventory at 31 March 20X6. Gods in trans > current At 31 March 20X6, Parent's records showed a receivable due from Sibling of $3 million, this differed to the equivalent payable in Sibling's records due to the goods in transit. The intra-group reconciliation should be achieved by assuming that Sibling had received the goods in transit before the year end. renuliahon The investment in Aunt represents 30% of its voting share capital and Parent uses equity accounting to account for this investment. Aunt's profit for the year ended 31 March 20X6 was $6m and Aunt paid total dividends during the year ended 31 March 20X6 of $2m. Parent has recorded its share of the dividend received from Aunt in investment income (and cash). All profits and losses accrued evenly throughout the year. There were no impairment losses within the group for the year ended 31 March 20X6. Required: Prepare the consolidated statement of financial position for Parent Co as at 31 March 20X6.

Expert Answer:

Answer rating: 100% (QA)

ANSWER Financial position is the current balance of the recorded assets liabilities and equity of an ... View the full answer

Related Book For

Probability and Statistics

ISBN: 978-0321500465

4th edition

Authors: Morris H. DeGroot, Mark J. Schervish

Posted Date:

Students also viewed these accounting questions

-

Prove the distributive properties in Theorem 1.4.10. In theorem For every three sets A, B, and C, A (B C) = (A B) (A C) and A (B C) = (A B) (A C).

-

On 1 April 20X5 Hardy entity acquired 4 million of Sibling entity's ordinary shares paying ¬4.50 each. At the same time it also purchased at nominal value ¬500 000 of its 10% preference...

-

Company S has 4,000 shares outstanding and a total stockholders equity of $200,000. It is about to issue 6,000 new shares to the prospective parent company. The shares will be sold for a total of...

-

A bond currently has a price of $940. The current yield to maturity on the bond is 7%. If the yield decreases by 20 basis points, the price of the bond will go up to $960. Based on this information,...

-

LetX1, X2 be two independent random variables each with p.d.f. f1(x) = ex for x > 0 and f1(x) = 0 for x 0. Let Z = X1 X2 and W = X1/X2. a. Find the joint p.d.f. of X1 and Z. b. Prove that the...

-

A Gallup Poll of U.S. adults indicated that Kentucky is the state with the highest percentage of smokers (Gallup.com, December 2015). Consider the following example data from the Tri-State region, an...

-

Prove that, for fixed \(t\), \[A_{t}^{(u)} \stackrel{\text { law }}{=} \int_{0}^{t} e^{2\left(u(t-s)+W_{t}-W_{s} ight.} d s:=Y_{t}^{(u)}\] and that, as a process \[d Y_{t}^{(u)}=\left(2(u+1)...

-

Talkington Electronics issues a $400,000, 8%, 15-year mortgage note on December 31, 2016. The proceeds from the note are to be used in financing a new research laboratory. The terms of the note...

-

coaches of women's sports teams at the college and university level are often paid significantly less than the coaches of men's teams. Should collegiate coaches receive equal salaries if they coach...

-

Micro Technologies sells two products: X and Y. The selling price, variable cost, and sales mix for the products are presented in the table below. Product Unit Sales Price Unit Variable Cost...

-

In Finance, you are responsible for: A. Oselling your products to the market. B. Ocreating products that meet your customers' demands. C. Omaking the products, and managing the capacity and...

-

What do you mean by Security Market Line? Suppose the risk- free rate goes down to 7%. What effect would higher interest rates have on the SML and on the returns required on high-risk and low-risk...

-

what ways does the interdisciplinary nature of recombinant DNA technology foster collaborations between molecular biologists, biochemists, engineers, and clinicians to address pressing societal...

-

How do recombinant DNA techniques contribute to the production of biopharmaceuticals, vaccines, and industrial enzymes through microbial fermentation, mammalian cell culture, and transgenic organism...

-

Can you elucidate the interplay between genetic imprinting, genomic imprinting disorders, and cloning, highlighting the challenges associated with preserving parent-specific epigenetic marks and...

-

Txy = An element is acted upon by the following stresses: x = 14 MPa. 49 MPa, y = 14 MPa, and (a) By means of the equations, compute the stresses on the sides of an element oriented 30 clockwise with...

-

Consider an economy in which the marginal propensity to consume is 0.75, prices are constant; G is initially 1,000, taxes are autonomous (not related to income) and are initially 1,400, transfer...

-

The activities listed in lines 2125 serve primarily as examples of A) Underappreciated dangers B) Intolerable risks C) Medical priorities D) Policy failures

-

For the data presented in Table 11.9, construct a confidence interval for 5β0 β1+ 4 with confidence coefficient 0.90. Table 11.9 Data for Exercise 1 87427 00077 12100 67890...

-

Consider again the conditions of Exercise 21. Show that a confidence interval for with confidence coefficient 1 can be obtained by the following procedure: Let k be the largest integer less than or...

-

Suppose that five components are functioning simultaneously, that the lifetimes of the components are i.i.d., and that each lifetime has the exponential distribution with parameter . Let T1 denote...

-

What is the goal of Industry 4.0?

-

In which application areas do you see opportunities for CPS and IoT systems? Where do you expect major changes caused by information technology?

-

Use the sources available to you to demonstrate the importance of embedded systems! Behavioral Structural design path high level of abstraction - low level of abstraction Geometrical Fig. 1.11...

Study smarter with the SolutionInn App