On March 21, 2017, Julia Mitchell, an equity analyst with a major superannuation fund, was working long

Question:

On March 21, 2017, Julia Mitchell, an equity analyst with a major superannuation fund, was working long hours; the fund had a significant stake in Downer EDI Limited (Downer), a leading provider of engineering, construction, and infrastructure management services in Australia and New Zealand. Downer had requested a three-day trading halt of its stock on the Australian Securities Exchange (ASX) to announce its unsolicited offer for Spotless Group Holdings (Spotless) at A$1.152per share and to launch the institutional portion of a renounceable rights issue intended to fund the acquisition.3

Mitchell had to decide whether to recommend that the fund accept the rights offering, and thus increase its exposure in Downer. To do so, she would have to be convinced that the takeover bid would be value- enhancing for Downer. However, Mitchell had several concerns with the offer. Spotless had struggled in recent years, Downer had not conducted any due diligence, and the offer price for Spotless stock was at a 59 per cent premium to the previous day's closing price of $0.725.4

With the institutional portion of the rights offering due to close the next day, on March 22, 2017, Mitchell had little time to complete her analysis of the acquisition's merits. She had to determine if Downer's $1.15 per share offer for Spotless was a golden opportunity to buy a company for a relatively low price, or if it was yet another example of an eager acquirer overpaying for a target company. How could Spotless be valued? What was Spotless really worth? Was the offer price of $1.15 per share a bargain, an overpayment, or a fair price for Downer shareholders?

TRANSACTION STRUCTURE5

Downer was offering cash consideration of $1.15 for Spotless stock, subject to several conditions, including regulatory approval, a minimum of 90 per cent acceptance, and no reduction in fiscal year (FY) 2017 earnings guidance provided by Spotless in February 2017. The takeover was to be funded from existing debt facilities and proceeds from a fully underwritten renounceable6two-for-five rights issue at $5.95 per share, which amounted to a 19.8 per cent discount on Downer's March 20, 2017 closing price of $7.42. The accelerated offer to institutional investors was scheduled to close on March 22, 2017; the offer to retail investors was closing on April 11, 2017.

Despite the projected 40 per cent increase in the number of shares on issue, Downer claimed that the transaction would increase the earnings per share (EPS) rate by approximately 10 per cent before any synergies. If pre-tax synergi

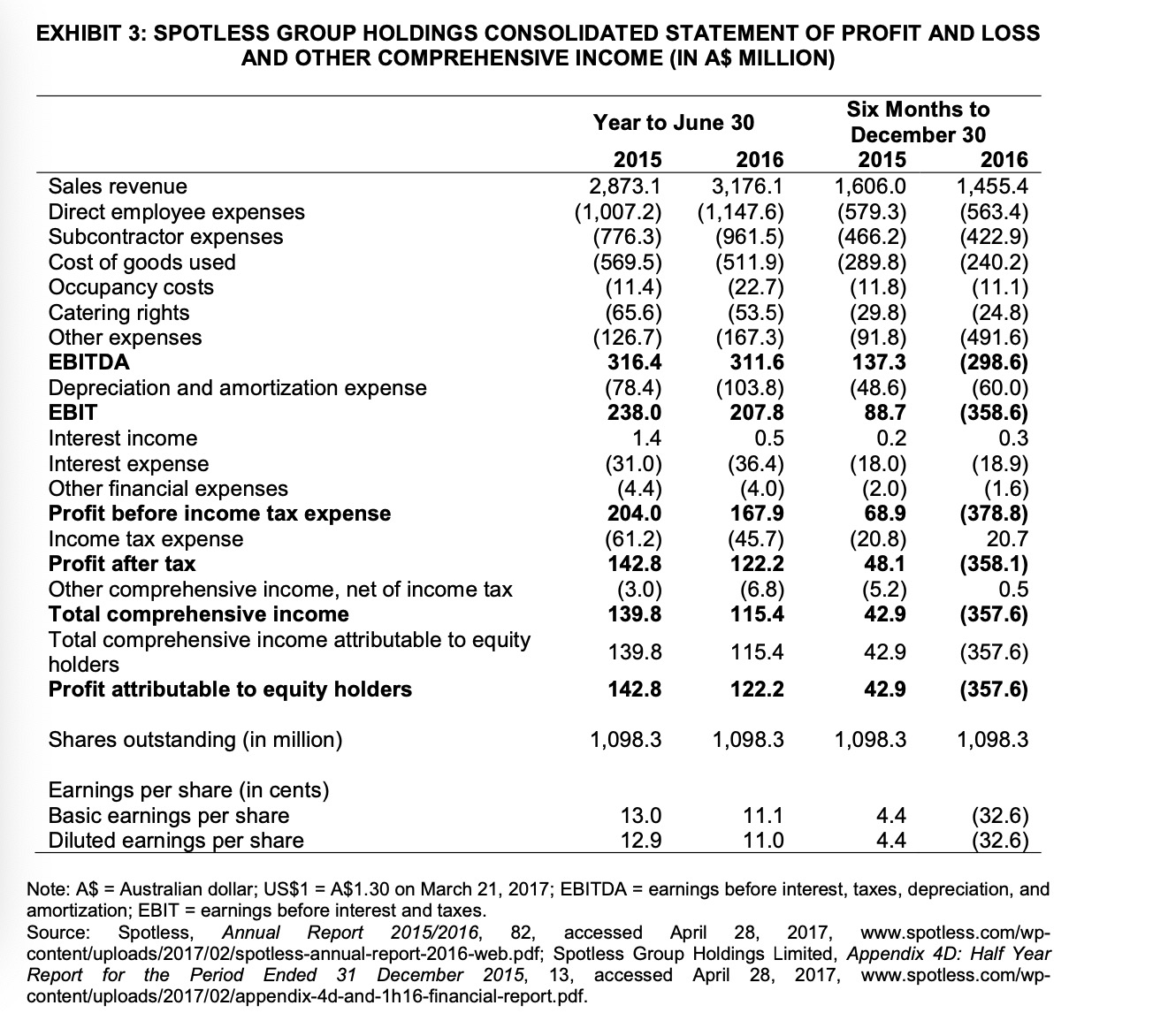

By Fn Spotless released its results for the first half of FY 2017 in late February 2017. The restructuring of the contract portfolio and other exceptional items resulted in a largely non-cash accodustry had total revenue of $2.1 billion and nearly 19,000 employees in FY 2017.28The laundry segment had benefitted from increasing demand for its services as the heavy investment require

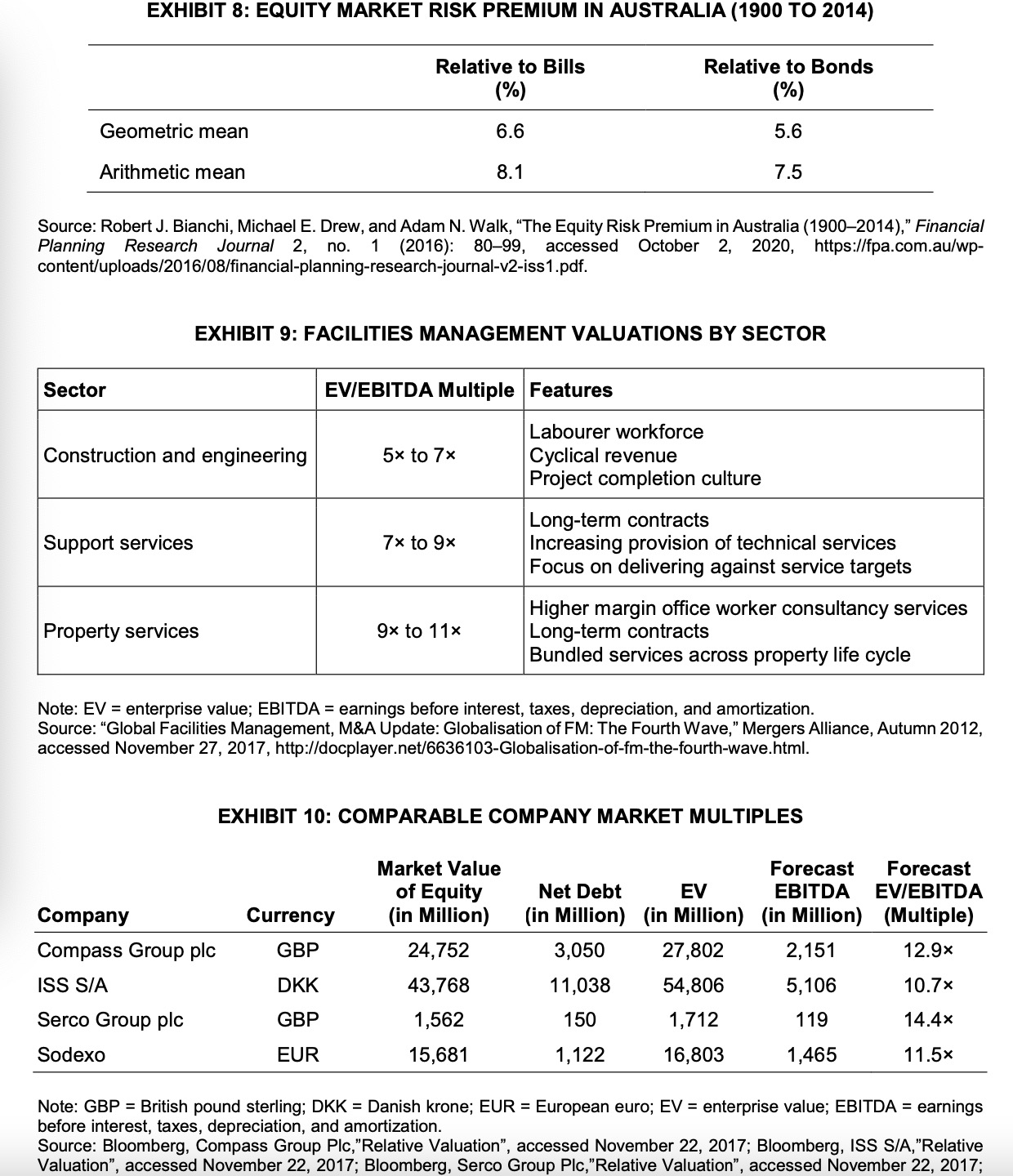

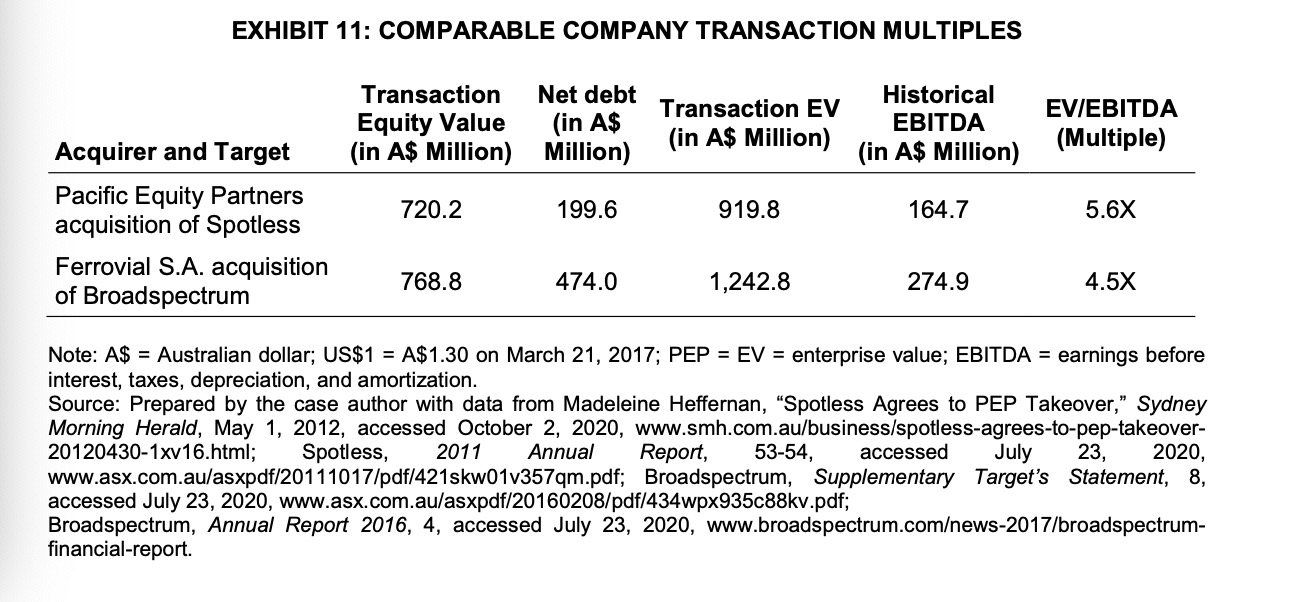

A valuation of Spotless, using both the free cash flow model and data on comparable companies, would help Mitchell decide whether the acquisition made sense for Downer shareholders. If the acquisition was not value-enhancing for Downer shareholders, Mitchell would recommend against taking up the rights offering. This would also mean that the fund should consider selling its stake in Downer.

Expert Answer: