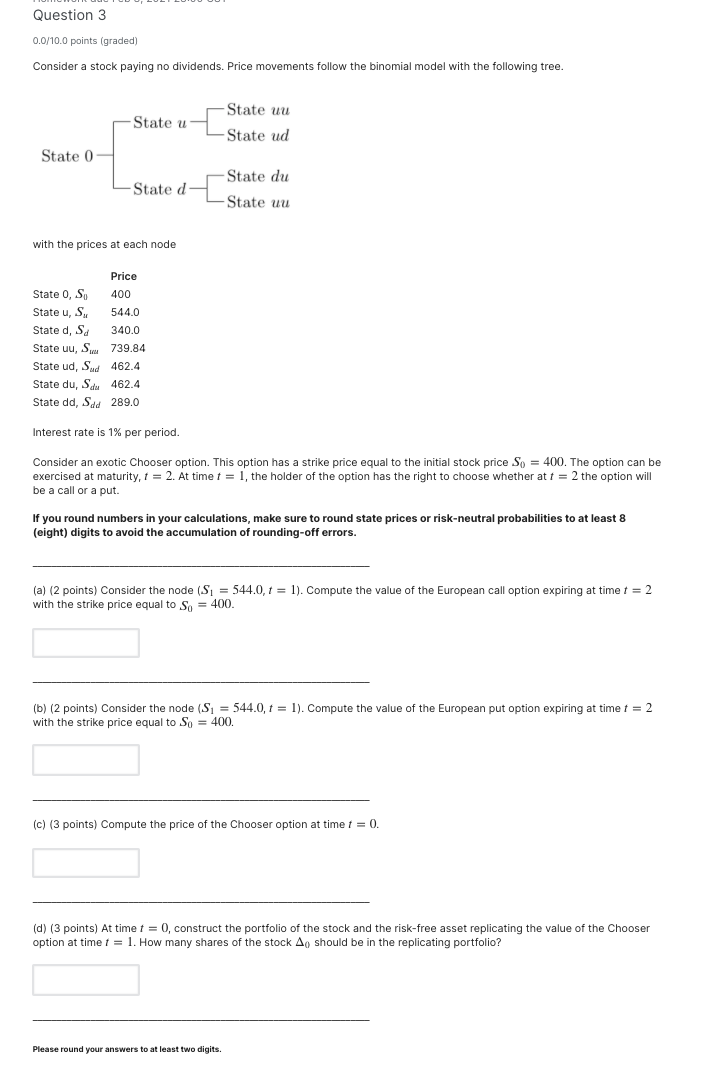

Question: option pricing, please provide correct answer. Thanks a lot for kind help. Question 3 0.0/10.0 points (graded) Consider a stock paying no dividends. Price movements

option pricing, please provide correct answer. Thanks a lot for kind help.

Question 3 0.0/10.0 points (graded) Consider a stock paying no dividends. Price movements follow the binomial model with the following tree. State uu State u State ud State 0 State du State d State uu with the prices at each node 544.0 Price State O, S. 400 State u, S, State d, Sd 340.0 State uu, S. 739.84 State ud, Sud 462.4 State du, Su 462.4 State dd, Sad 289.0 Interest rate is 1% per period. Consider an exotic Chooser This option has a strike price equal to the initial stock price So = 400. The option be exercised at maturity, t = 2. At time t = 1, the holder of the option has the right to choose whether at t = 2 the option will be a call or a put. If you round numbers in your calculations, make sure to round state prices or risk-neutral probabilities to at least 8 (eight) digits to avoid the accumulation of rounding-off errors. (a) (2 points) Consider the node (Si = 544.0, 1 = 1). Compute the value of the European call option expiring at time t = 2 with the strike price equal to So = 400. (b) (2 points) Consider the node (S = 544.0, 1 = 1). Compute the value of the European put option expiring at time t = 2 with the strike price equal to So = 400. (c) (3 points) Compute the price of the Chooser option at time t = 0. (d) (3 points) At time t = 0, construct the portfolio of the stock and the risk-free asset replicating the value of the Chooser option at time t = 1. How many shares of the stock A, should be in the replicating portfolio? Please round your answers to at least two digits. Question 3 0.0/10.0 points (graded) Consider a stock paying no dividends. Price movements follow the binomial model with the following tree. State uu State u State ud State 0 State du State d State uu with the prices at each node 544.0 Price State O, S. 400 State u, S, State d, Sd 340.0 State uu, S. 739.84 State ud, Sud 462.4 State du, Su 462.4 State dd, Sad 289.0 Interest rate is 1% per period. Consider an exotic Chooser This option has a strike price equal to the initial stock price So = 400. The option be exercised at maturity, t = 2. At time t = 1, the holder of the option has the right to choose whether at t = 2 the option will be a call or a put. If you round numbers in your calculations, make sure to round state prices or risk-neutral probabilities to at least 8 (eight) digits to avoid the accumulation of rounding-off errors. (a) (2 points) Consider the node (Si = 544.0, 1 = 1). Compute the value of the European call option expiring at time t = 2 with the strike price equal to So = 400. (b) (2 points) Consider the node (S = 544.0, 1 = 1). Compute the value of the European put option expiring at time t = 2 with the strike price equal to So = 400. (c) (3 points) Compute the price of the Chooser option at time t = 0. (d) (3 points) At time t = 0, construct the portfolio of the stock and the risk-free asset replicating the value of the Chooser option at time t = 1. How many shares of the stock A, should be in the replicating portfolio? Please round your answers to at least two digits

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts