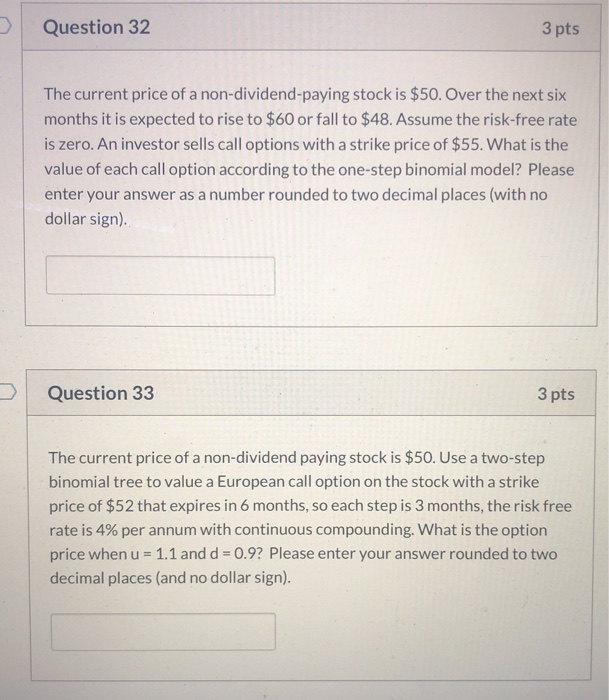

Question: Options HW. Please help. TY Question 32 3 pts The current price of a non-dividend paying stock is $50. Over the next six months it

Question 32 3 pts The current price of a non-dividend paying stock is $50. Over the next six months it is expected to rise to $60 or fall to $48. Assume the risk-free rate is zero. An investor sells call options with a strike price of $55. What is the value of each call option according to the one-step binomial model? Please enter your answer as a number rounded to two decimal places (with no dollar sign). Question 33 3 pts The current price of a non-dividend paying stock is $50. Use a two-step binomial tree to value a European call option on the stock with a strike price of $52 that expires in 6 months, so each step is 3 months, the risk free rate is 4% per annum with continuous compounding. What is the option price when u = 1.1 and d = 0.9? Please enter your answer rounded to two decimal places (and no dollar sign)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts