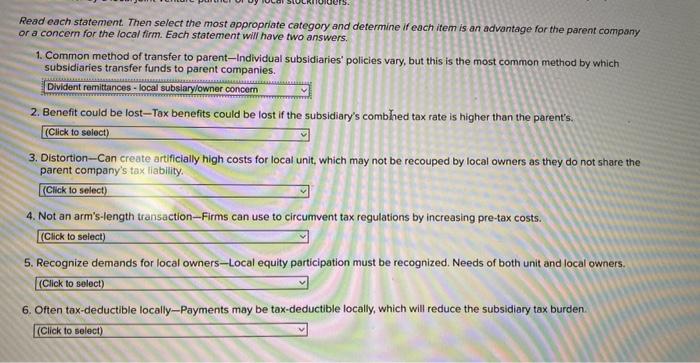

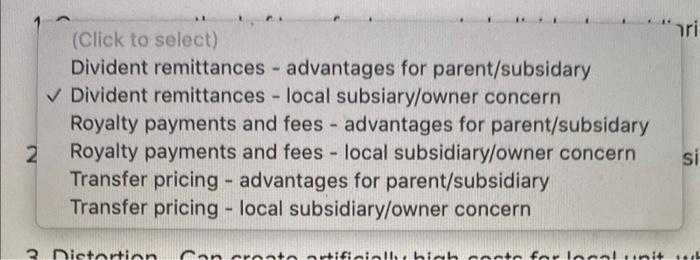

Question: or a concern for the local firm. Each statement will have two answers. 1. Common method of transfer to parent-Individual subsidiaries' policies vary, but this

or a concern for the local firm. Each statement will have two answers. 1. Common method of transfer to parent-Individual subsidiaries' policies vary, but this is the most common method by which subsidiaries transfer funds to parent companies. 2. Benefit could be lost-Tax benefits could be lost if the subsidiary's combhed tax rate is higher than the parent's. 3. Distortion-Can create artificially high costs for local unit, which may not be recouped by local owners as they do not share the parent company's tax liability. 4. Not an arm's-length transaction - Firms can use to circumvent tax regulations by increasing pre-tax costs. 5. Recognize demands for local owners-Local equity participation must be recognized. Needs of both unit and local owners. 6. Often tax-deductible locally-Payments may be tax-deductible locally, which will reduce the subsidiary tax burden. (Click to select) Divident remittances - advantages for parent/subsidary Divident remittances - local subsiary/owner concern Royalty payments and fees - advantages for parent/subsidary Royalty payments and fees - local subsidiary/owner concern Transfer pricing - advantages for parent/subsidiary Transfer pricing - local subsidiary/owner concern

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts