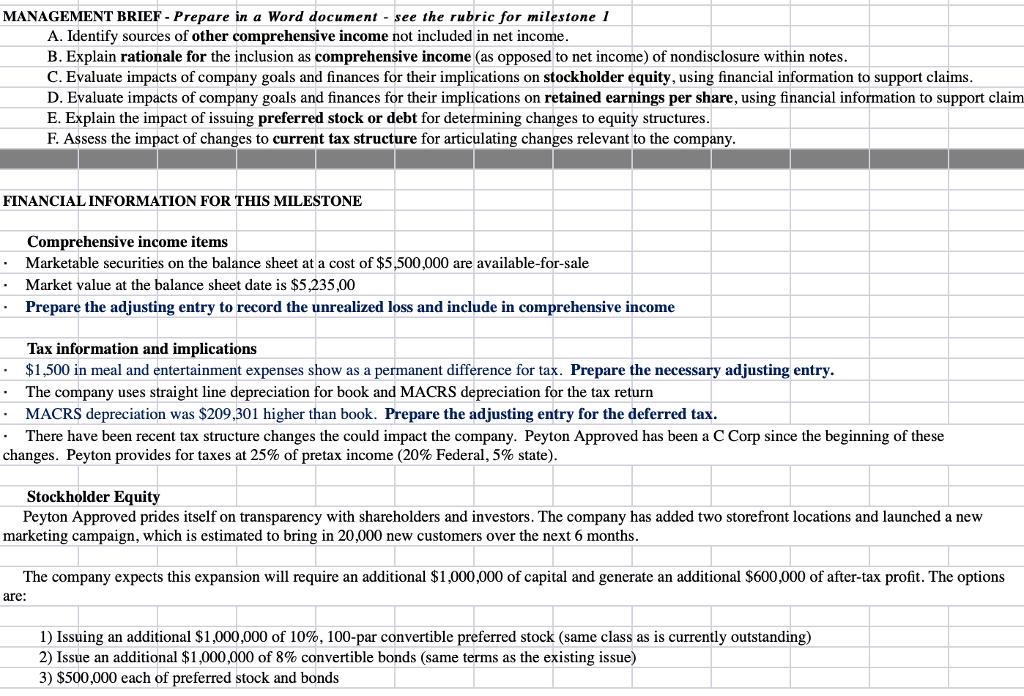

Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

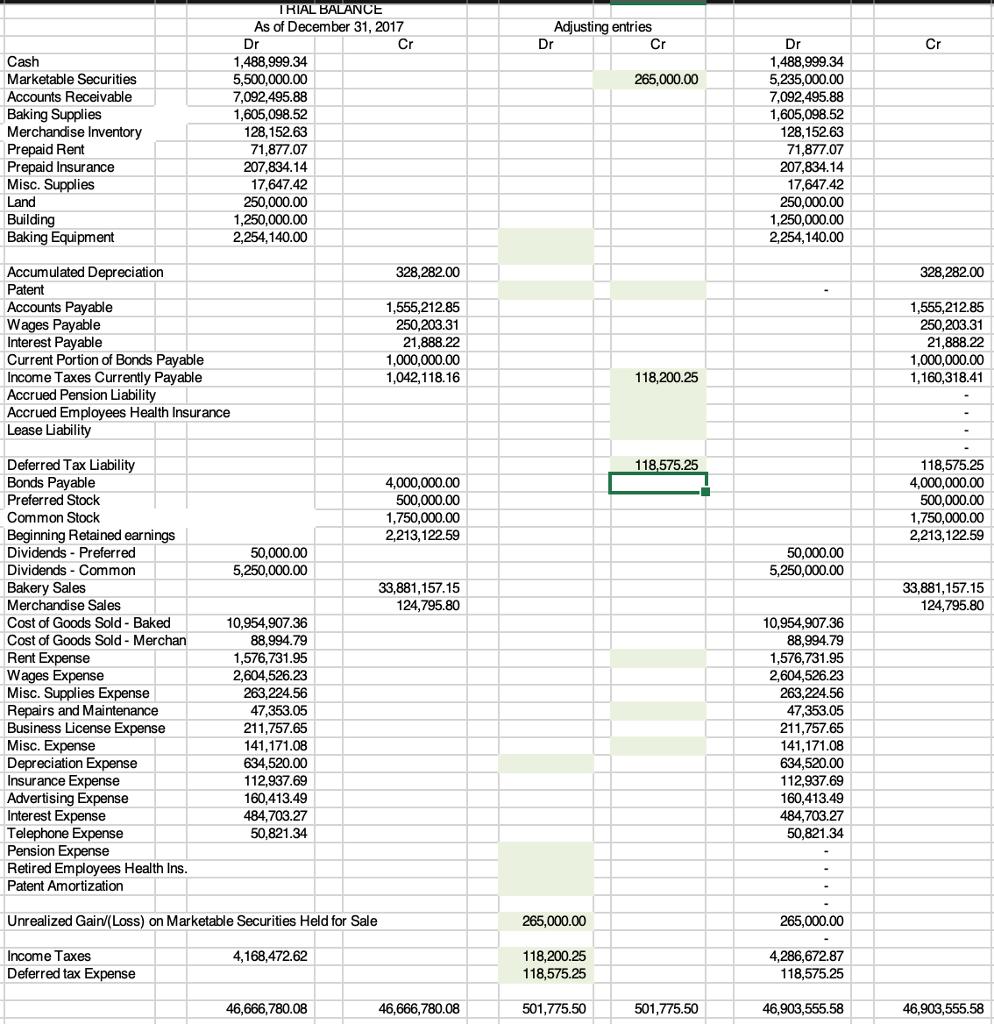

Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58 Overview Imagine that you are working as a financial accountant for Peyton Approved, and you have been charged with revising its financial information. The company has experienced tremendous growth in the past three years, and it is now a well-known bakery chain for pet products. They have become a publicly traded company and have several locations that they deliver to regionally. You will find the company's financial information in the Peyton Approved Balance Sheet and Income Statement. This document will need revisions and appropriate notes added in order to prepare for the year-end audit accordingly. In addition to ensuring that the balance sheet is ready for the year-end audit, you will address other major areas of need, including: Assessing tax implications ● Evaluating and explaining stockholder equity Accounting for postretirement benefits (The amounts would be determined by actuaries.) Assessing impacts of leases ● ● ● Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds MANAGEMENT BRIEF - Prepare in a Word document - see the rubric for milestone 1 A. Identify sources of other comprehensive income not included in net income. B. Explain rationale for the inclusion as comprehensive income (as opposed to net income) of nondisclosure within notes. FINANCIAL INFORMATION FOR THIS MILESTONE . . . Tax information and implications $1,500 in meal and entertainment expenses show as a permanent difference for tax. Prepare the necessary adjusting entry. The company uses straight line depreciation for book and MACRS depreciation for the tax return MACRS depreciation was $209,301 higher than book. Prepare the adjusting entry for the deferred tax. There have been recent tax structure changes the could impact the company. Peyton Approved has been a C Corp since the beginning of these changes. Peyton provides for taxes at 25% of pretax income (20% Federal, 5% state). . C. Evaluate impacts of company goals and finances for their implications on stockholder equity, using financial information to support claims. D. Evaluate impacts of company goals and finances for their implications on retained earnings per share, using financial information to support claim E. Explain the impact of issuing preferred stock or debt for determining changes to equity structures. F. Assess the impact of changes to current tax structure for articulating changes relevant to the company. . . Comprehensive income items Marketable securities on the balance sheet at a cost of $5,500,000 are available-for-sale Market value at the balance sheet date is $5,235,00 Prepare the adjusting entry to record the unrealized loss and include in comprehensive income Stockholder Equity Peyton Approved prides itself on transparency with shareholders and investors. The company has added two storefront locations and launched a new marketing campaign, which is estimated to bring in 20,000 new customers over the next 6 months. The company expects this expansion will require an additional $1,000,000 of capital and generate an additional $600,000 of after-tax profit. The options are: 1) Issuing an additional $1,000,000 of 10%, 100-par convertible preferred stock (same class as is currently outstanding) 2) Issue an additional $1,000,000 of 8% convertible bonds (same terms as the existing issue) 3) $500,000 each of preferred stock and bonds Cash Marketable Securities Accounts Receivable Baking Supplies Merchandise Inventory Prepaid Rent Prepaid Insurance Misc. Supplies Land Building Baking Equipment Accumulated Depreciation Patent Accounts Payable Wages Payable Interest Payable Current Portion of Bonds Payable Income Taxes Currently Payable Accrued Pension Liability Accrued Employees Health Insurance Lease Liability Deferred Tax Liability Bonds Payable Preferred Stock Common Stock Beginning Retained earnings Dividends Preferred Dividends - Common Bakery Sales Merchandise Sales Cost of Goods Sold - Baked Cost of Goods Sold - Merchan Rent Expense Wages Expense Misc. Supplies Expense Repairs and Maintenance Business License Expense Misc. Expense Depreciation Expense Insurance Expense Advertising Expense Interest Expense Telephone Expense Pension Expense Retired Employees Health Ins. Patent Amortization TRIAL BALANCE As of December 31, 2017 Dr Cr Income Taxes Deferred tax Expense 1,488.999.34 5,500,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 Unrealized Gain/(Loss) on Marketable Securities Held for Sale 4,168,472.62 46,666,780.08 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,042,118.16 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,666,780.08 Adjusting entries Dr 265,000.00 118,200.25 118,575.25 501,775.50 Cr 265,000.00 118,200.25 118,575.25 501,775.50 Dr 1,488,999.34 5,235,000.00 7,092,495.88 1,605,098.52 128,152.63 71,877.07 207,834.14 17,647.42 250,000.00 1,250,000.00 2,254,140.00 50,000.00 5,250,000.00 10,954,907.36 88,994.79 1,576,731.95 2,604,526.23 263,224.56 47,353.05 211,757.65 141,171.08 634,520.00 112,937.69 160,413.49 484,703.27 50,821.34 265,000.00 4,286,672.87 118,575.25 46,903,555.58 Cr 328,282.00 1,555,212.85 250,203.31 21,888.22 1,000,000.00 1,160,318.41 118,575.25 4,000,000.00 500,000.00 1,750,000.00 2,213,122.59 33,881,157.15 124,795.80 46,903,555.58

Expert Answer:

Answer rating: 100% (QA)

Analyzing inventory costs You will need to review the balance sheet income statement and other relev... View the full answer

Related Book For

Quality Inspired Management The Key to Sustainability

ISBN: 978-0131197565

1st edition

Authors: Harold Aikens

Posted Date:

Students also viewed these accounting questions

-

Imagine that you are on the board of directors of a company and you receive a letter from the chairman of the board that starts, "With deep regret and tremendous burden that I am carrying on my...

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

Since its founding in 1980, Chateau Americana (CA) has cultivated a reputation as one of America's finest wineries. The small, family-owned winery has an impressive vineyard whose 125 acres yields a...

-

After assembly, a finished TV is left turned on for one full day (24 h) to determine whether the product is reliable. On average, two TVs break down each day. Yesterday 500 TVs were produced. What is...

-

What are the penalties if Artist breaches the movie contract? Why are the penalties so light?

-

A firm uses a one-week periodic review inventory system. A two-day lead time is needed for any order, and the firm is willing to tolerate an average of one stock-out per year. a. Using the firms...

-

To determine whether your firm should change its dividend policy, based on an analysis of its investment opportunities and comparable firms. Key Questions How much could this firm have returned to...

-

(Determine Proper Amounts in Account Balances) Presented below are three independent situations. (a) Chinook Corporation incurred the following costs in connection with the issuance of bonds: (1)...

-

1.Garrison Corporation purchased a depreciable asset for $420,000 on January 1, 2015. The estimated salvage value is $42,000, and the estimated total useful life is 9 years. The straight-line method...

-

AT&T plans to sell the new iPhone for $200. The lower-priced phone would give AT&T an attractive weapon to win new subscribers. AT&Ts revenue is an average of $95 a month from each iPhone customer,...

-

What is the organizational structure and culture? Explain

-

Examine the use of unreliable narration in "The Catcher in the Rye." How does this technique affect the reader's perception of the protagonist, Holden Caulfield, and what does it suggest about his...

-

Write an appropriate C++ program segment that will ask the user to insert 15 positive integer numbers. Any negative number will not be counted as their input. From all the positive integer number...

-

Walton Sporting Goods Corporation makes two types of racquets, tennis and badminton. The company uses the same facility to make both products even though the processes are quite different. The...

-

Discuss the role of intertextuality in James Joyce's "Ulysses." How does Joyce reference and reinterpret classical texts to build the novel's layered narrative ?

-

The Fiat Lux lamp company manufactures metal lamps using a variety of different metals and their production is constrained by how much of each metal they have on hand. For the next month, the company...

-

What is the holding period return of the baseball?card?What is the simple annual return on the baseball? cardWhat is the effective annual return?(EAR) on the baseball?card? Holding period and annual...

-

What tools are available to help shoppers compare prices, features, and values and check other shoppers opinions?

-

Define some of the outcomes of HRM as an open system. How can feedback be used to improve these outcomes? How would these outcomes be measured?

-

Suggest some of the issues that an ecodesign engineer should consider in developing green designs for the following products. a. Computer b. Automobile c. Sport coat d. Shoes

-

Consider each of the organizations listed in problem 3-6. To what extent do you believe the employees can be empowered? As a senior leader, how would you empower them?

-

On July 1, 2020, West Company purchased for cash, eight \(\$ 10,000\) bonds of North Corporation to yield \(10 \%\). The bonds pay \(9 \%\) interest, payable on a semiannual basis each July 1 and...

-

Repeat Exercise 14-43, assuming discounts and premiums are amortized using the straight-line interest method. Exercise 14-43 On July 1, 2020, West Company purchased for cash, eight \(\$ 10,000\)...

-

On January 1, 2020, Lazer Inc. purchased for cash, ten \(\$ 1,000,4 \%\) bonds of Star Corp. at par. The bond interest is paid annually on January 1 of each year, and the bond maturity date is...

Study smarter with the SolutionInn App