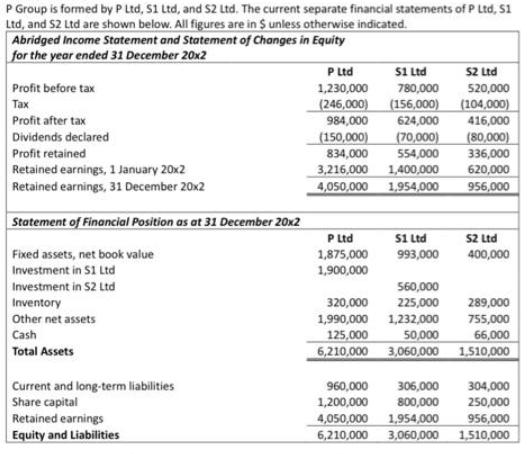

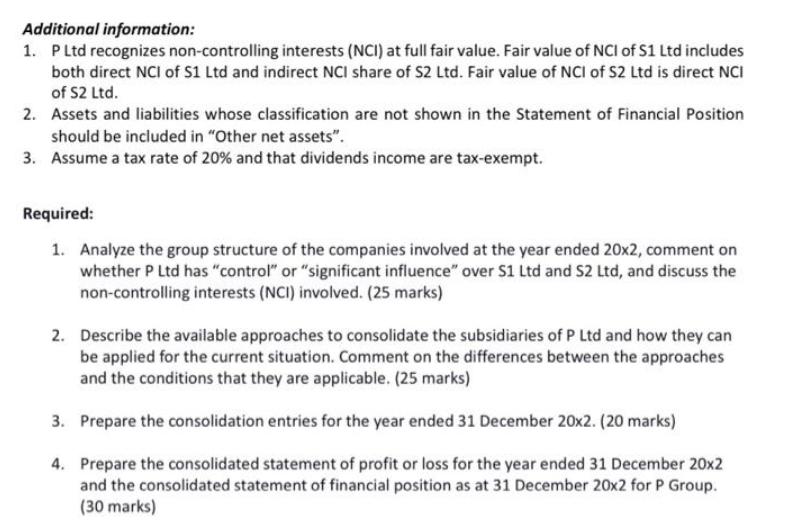

P Group is formed by P Ltd, S1 Ltd, and 52 Ltd. The current separate financial...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

1 P Ltd has control over both 1 Ltd and 2 Ltd because it has a majority shareholding in both companies P Ltd also has the power to appoint and remove the majority of the board of directors of both com... View the full answer

Related Book For

Advanced Accounting

ISBN: 978-0077431808

10th edition

Authors: Joe Hoyle, Thomas Schaefer, Timothy Doupnik

Posted Date: