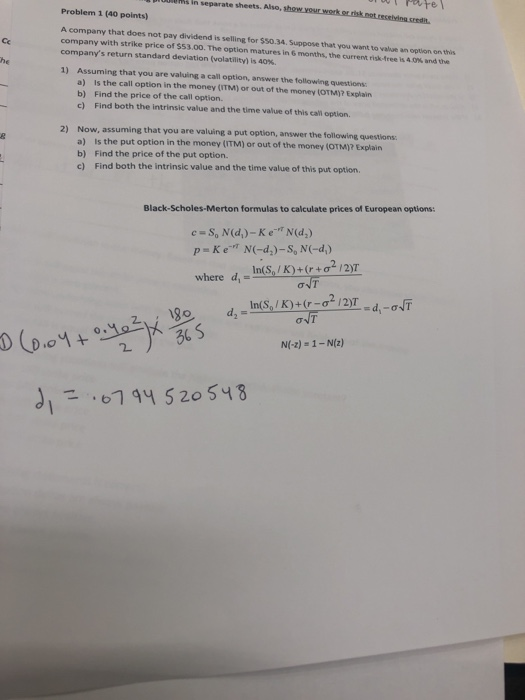

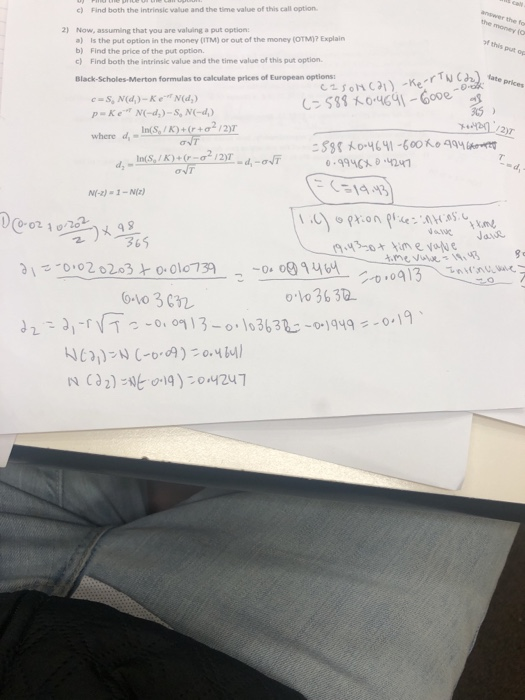

Question: Pare s in separate sheets. Also, Problem 1 (40 points) A company that does not pay dividend is selling for $$0.34. Suppose that you want

Pare s in separate sheets. Also, Problem 1 (40 points) A company that does not pay dividend is selling for $$0.34. Suppose that you want to value an option on this company with strike price of S53.00. The option matures in 6 months, the current risk4ree is 40% rdre company's return standard deviation (volatility) is 40%. 1) Assuming that you are valuing a call option, answer the following questions: he Is the call option in the money (ITM) or out of the money (OTM)? Explain Find the price of the call option. Find both the intrinsic value and the time value of this call option a) b) c) 2) Now, assuming that you are valuing a put option, answer the following questions: Is the put option in the money (ITM) or out of the Find the price of the put option. Find both the intrinsic value and the time value of this put option. a) b) c) money (OTM)? Explain Black-Scholes-Merton formulas to calculate prices of European options: In(sa/K)+(r+2/2)T aNT d, where N(-z)-1-N(z) 7 94 520548 r the fo the money (O c) Find both the intrinsic value and the time value of this call option of this put op 2) Now, assuming that you are valuing a put option a) Is the put option in the money (ITM) or out of the money (OTM)? Explain b) Find the price of the put option. c) Find both the intrinsic value and the time value of this put option Black-Scholes-Merton formulas to calculate prices of European options ate prices /2)7 where d, In(S./K+Ct .4247 0 . 994CA M-2)-1-N(z) o o 3630 6-10 3 Pare s in separate sheets. Also, Problem 1 (40 points) A company that does not pay dividend is selling for $$0.34. Suppose that you want to value an option on this company with strike price of S53.00. The option matures in 6 months, the current risk4ree is 40% rdre company's return standard deviation (volatility) is 40%. 1) Assuming that you are valuing a call option, answer the following questions: he Is the call option in the money (ITM) or out of the money (OTM)? Explain Find the price of the call option. Find both the intrinsic value and the time value of this call option a) b) c) 2) Now, assuming that you are valuing a put option, answer the following questions: Is the put option in the money (ITM) or out of the Find the price of the put option. Find both the intrinsic value and the time value of this put option. a) b) c) money (OTM)? Explain Black-Scholes-Merton formulas to calculate prices of European options: In(sa/K)+(r+2/2)T aNT d, where N(-z)-1-N(z) 7 94 520548 r the fo the money (O c) Find both the intrinsic value and the time value of this call option of this put op 2) Now, assuming that you are valuing a put option a) Is the put option in the money (ITM) or out of the money (OTM)? Explain b) Find the price of the put option. c) Find both the intrinsic value and the time value of this put option Black-Scholes-Merton formulas to calculate prices of European options ate prices /2)7 where d, In(S./K+Ct .4247 0 . 994CA M-2)-1-N(z) o o 3630 6-10 3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts