Paron Co is intending to acquire a subsidiary on 1 January 20x0 and has shortlisted one...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

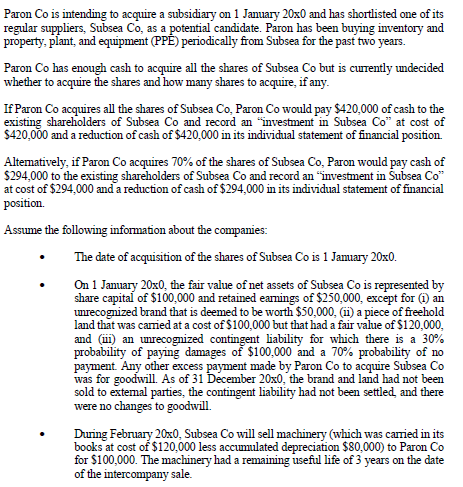

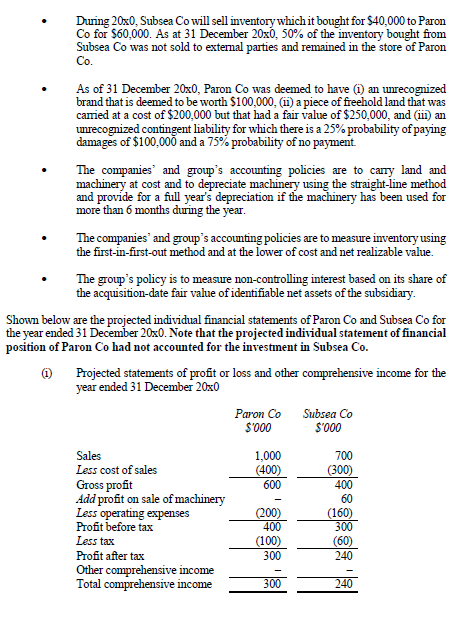

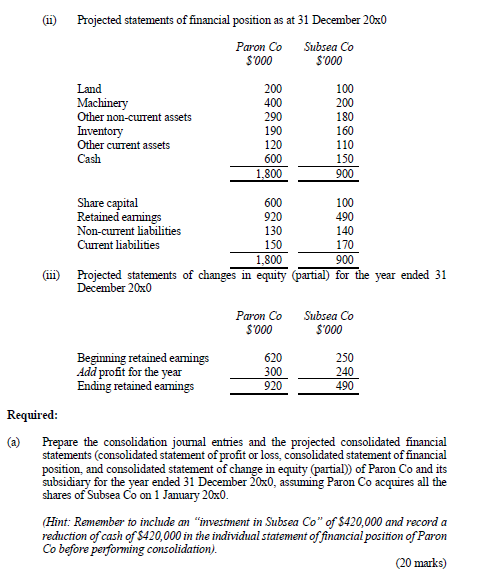

Paron Co is intending to acquire a subsidiary on 1 January 20x0 and has shortlisted one of its regular suppliers, Subsea Co, as a potential candidate. Paron has been buying inventory and property, plant, and equipment (PPE) periodically from Subsea for the past two years. Paron Co has enough cash to acquire all the shares of Subsea Co but is currently undecided whether to acquire the shares and how many shares to acquire, if any. If Paron Co acquires all the shares of Subsea Co, Paron Co would pay $420,000 of cash to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $420,000 and a reduction of cash of $420,000 in its individual statement of financial position. Alternatively, if Paron Co acquires 70% of the shares of Subsea Co, Paron would pay cash of $294,000 to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $294,000 and a reduction of cash of $294,000 in its individual statement of financial position. Assume the following information about the companies: The date of acquisition of the shares of Subsea Co is 1 January 20x0. On 1 January 20x0, the fair value of net assets of Subsea Co is represented by share capital of $100,000 and retained earnings of $250,000, except for (1) an unrecognized brand that is deemed to be worth $50,000, (ii) a piece of freehold land that was carried at a cost of $100,000 but that had a fair value of $120,000, and (iii) an unrecognized contingent liability for which there is a 30% probability of paying damages of $100,000 and a 70% probability of no payment. Any other excess payment made by Paron Co to acquire Subsea Co was for goodwill. As of 31 December 20x0, the brand and land had not been sold to external parties, the contingent liability had not been settled, and there were no changes to goodwill. During February 20x0, Subsea Co will sell machinery (which was carried in its books at cost of $120,000 less accumulated depreciation $80,000) to Paron Co for $100,000. The machinery had a remaining useful life of 3 years on the date of the intercompany sale. During 20x0, Subsea Co will sell inventory which it bought for $40,000 to Paron Co for $60,000. As at 31 December 20x0, 50% of the inventory bought from Subsea Co was not sold to external parties and remained in the store of Paron Co. As of 31 December 20x0, Paron Co was deemed to have (1) an unrecognized brand that is deemed to be worth $100,000, (11) a piece of freehold land that was carried at a cost of $200,000 but that had a fair value of $250,000, and (iii) an unrecognized contingent liability for which there is a 25% probability of paying damages of $100,000 and a 75% probability of no payment. The companies and group's accounting policies are to carry land and machinery at cost and to depreciate machinery using the straight-line method and provide for a full year's depreciation if the machinery has been used for more than 6 months during the year. The companies' and group's accounting policies are to measure inventory using the first-in-first-out method and at the lower of cost and net realizable value. The group's policy is to measure non-controlling interest based on its share of the acquisition-date fair value of identifiable net assets of the subsidiary. Shown below are the projected individual financial statements of Paron Co and Subsea Co for the year ended 31 December 20x0. Note that the projected individual statement of financial position of Paron Co had not accounted for the investment in Subsea Co. (1) Projected statements of profit or loss and other comprehensive income for the year ended 31 December 20x0 Sales Less cost of sales Gross profit Add profit on sale of machinery Less operating expenses Profit before tax Less tax Profit after tax Other comprehensive income Total comprehensive income Paron Co $'000 1,000 (400) 600 (200) ***** 400 (100) 300 300 Subsea Co $'000 ********* (300) (160) (60) (111) Required: (a) Projected statements of financial position as at 31 December 20x0 Paron Co $'000 Land Machinery Other non-current assets Inventory Other current assets Cash Share capital Retained earnings Non-current liabilities Current liabilities 200 400 290 190 120 600 1,800 Beginning retained earnings Add profit for the year Ending retained earnings 600 920 130 150 Paron Co $'000 Subsea Co $'000 1,800 900 Projected statements of changes in equity (partial) for the year ended 31 December 20x0 620 300 920 100 200 180 160 110 150 900 100 490 140 170 Subsea Co $'000 250 240 490 Prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of Paron Co and its subsidiary for the year ended 31 December 20x0, assuming Paron Co acquires all the shares of Subsea Co on 1 January 20x0. (Hint: Remember to include an "investment in Subsea Co" of $420,000 and record a reduction of cash of $420,000 in the individual statement of financial position of Paron Co before performing consolidation). (20 marks) Paron Co is intending to acquire a subsidiary on 1 January 20x0 and has shortlisted one of its regular suppliers, Subsea Co, as a potential candidate. Paron has been buying inventory and property, plant, and equipment (PPE) periodically from Subsea for the past two years. Paron Co has enough cash to acquire all the shares of Subsea Co but is currently undecided whether to acquire the shares and how many shares to acquire, if any. If Paron Co acquires all the shares of Subsea Co, Paron Co would pay $420,000 of cash to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $420,000 and a reduction of cash of $420,000 in its individual statement of financial position. Alternatively, if Paron Co acquires 70% of the shares of Subsea Co, Paron would pay cash of $294,000 to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $294,000 and a reduction of cash of $294,000 in its individual statement of financial position. Assume the following information about the companies: The date of acquisition of the shares of Subsea Co is 1 January 20x0. On 1 January 20x0, the fair value of net assets of Subsea Co is represented by share capital of $100,000 and retained earnings of $250,000, except for (1) an unrecognized brand that is deemed to be worth $50,000, (ii) a piece of freehold land that was carried at a cost of $100,000 but that had a fair value of $120,000, and (iii) an unrecognized contingent liability for which there is a 30% probability of paying damages of $100,000 and a 70% probability of no payment. Any other excess payment made by Paron Co to acquire Subsea Co was for goodwill. As of 31 December 20x0, the brand and land had not been sold to external parties, the contingent liability had not been settled, and there were no changes to goodwill. During February 20x0, Subsea Co will sell machinery (which was carried in its books at cost of $120,000 less accumulated depreciation $80,000) to Paron Co for $100,000. The machinery had a remaining useful life of 3 years on the date of the intercompany sale. During 20x0, Subsea Co will sell inventory which it bought for $40,000 to Paron Co for $60,000. As at 31 December 20x0, 50% of the inventory bought from Subsea Co was not sold to external parties and remained in the store of Paron Co. As of 31 December 20x0, Paron Co was deemed to have (1) an unrecognized brand that is deemed to be worth $100,000, (11) a piece of freehold land that was carried at a cost of $200,000 but that had a fair value of $250,000, and (iii) an unrecognized contingent liability for which there is a 25% probability of paying damages of $100,000 and a 75% probability of no payment. The companies and group's accounting policies are to carry land and machinery at cost and to depreciate machinery using the straight-line method and provide for a full year's depreciation if the machinery has been used for more than 6 months during the year. The companies' and group's accounting policies are to measure inventory using the first-in-first-out method and at the lower of cost and net realizable value. The group's policy is to measure non-controlling interest based on its share of the acquisition-date fair value of identifiable net assets of the subsidiary. Shown below are the projected individual financial statements of Paron Co and Subsea Co for the year ended 31 December 20x0. Note that the projected individual statement of financial position of Paron Co had not accounted for the investment in Subsea Co. (1) Projected statements of profit or loss and other comprehensive income for the year ended 31 December 20x0 Sales Less cost of sales Gross profit Add profit on sale of machinery Less operating expenses Profit before tax Less tax Profit after tax Other comprehensive income Total comprehensive income Paron Co $'000 1,000 (400) 600 (200) ***** 400 (100) 300 300 Subsea Co $'000 ********* (300) (160) (60) (111) Required: (a) Projected statements of financial position as at 31 December 20x0 Paron Co $'000 Land Machinery Other non-current assets Inventory Other current assets Cash Share capital Retained earnings Non-current liabilities Current liabilities 200 400 290 190 120 600 1,800 Beginning retained earnings Add profit for the year Ending retained earnings 600 920 130 150 Paron Co $'000 Subsea Co $'000 1,800 900 Projected statements of changes in equity (partial) for the year ended 31 December 20x0 620 300 920 100 200 180 160 110 150 900 100 490 140 170 Subsea Co $'000 250 240 490 Prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of Paron Co and its subsidiary for the year ended 31 December 20x0, assuming Paron Co acquires all the shares of Subsea Co on 1 January 20x0. (Hint: Remember to include an "investment in Subsea Co" of $420,000 and record a reduction of cash of $420,000 in the individual statement of financial position of Paron Co before performing consolidation). (20 marks) Paron Co is intending to acquire a subsidiary on 1 January 20x0 and has shortlisted one of its regular suppliers, Subsea Co, as a potential candidate. Paron has been buying inventory and property, plant, and equipment (PPE) periodically from Subsea for the past two years. Paron Co has enough cash to acquire all the shares of Subsea Co but is currently undecided whether to acquire the shares and how many shares to acquire, if any. If Paron Co acquires all the shares of Subsea Co, Paron Co would pay $420,000 of cash to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $420,000 and a reduction of cash of $420,000 in its individual statement of financial position. Alternatively, if Paron Co acquires 70% of the shares of Subsea Co, Paron would pay cash of $294,000 to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $294,000 and a reduction of cash of $294,000 in its individual statement of financial position. Assume the following information about the companies: The date of acquisition of the shares of Subsea Co is 1 January 20x0. On 1 January 20x0, the fair value of net assets of Subsea Co is represented by share capital of $100,000 and retained earnings of $250,000, except for (1) an unrecognized brand that is deemed to be worth $50,000, (ii) a piece of freehold land that was carried at a cost of $100,000 but that had a fair value of $120,000, and (iii) an unrecognized contingent liability for which there is a 30% probability of paying damages of $100,000 and a 70% probability of no payment. Any other excess payment made by Paron Co to acquire Subsea Co was for goodwill. As of 31 December 20x0, the brand and land had not been sold to external parties, the contingent liability had not been settled, and there were no changes to goodwill. During February 20x0, Subsea Co will sell machinery (which was carried in its books at cost of $120,000 less accumulated depreciation $80,000) to Paron Co for $100,000. The machinery had a remaining useful life of 3 years on the date of the intercompany sale. During 20x0, Subsea Co will sell inventory which it bought for $40,000 to Paron Co for $60,000. As at 31 December 20x0, 50% of the inventory bought from Subsea Co was not sold to external parties and remained in the store of Paron Co. As of 31 December 20x0, Paron Co was deemed to have (1) an unrecognized brand that is deemed to be worth $100,000, (11) a piece of freehold land that was carried at a cost of $200,000 but that had a fair value of $250,000, and (iii) an unrecognized contingent liability for which there is a 25% probability of paying damages of $100,000 and a 75% probability of no payment. The companies and group's accounting policies are to carry land and machinery at cost and to depreciate machinery using the straight-line method and provide for a full year's depreciation if the machinery has been used for more than 6 months during the year. The companies' and group's accounting policies are to measure inventory using the first-in-first-out method and at the lower of cost and net realizable value. The group's policy is to measure non-controlling interest based on its share of the acquisition-date fair value of identifiable net assets of the subsidiary. Shown below are the projected individual financial statements of Paron Co and Subsea Co for the year ended 31 December 20x0. Note that the projected individual statement of financial position of Paron Co had not accounted for the investment in Subsea Co. (1) Projected statements of profit or loss and other comprehensive income for the year ended 31 December 20x0 Sales Less cost of sales Gross profit Add profit on sale of machinery Less operating expenses Profit before tax Less tax Profit after tax Other comprehensive income Total comprehensive income Paron Co $'000 1,000 (400) 600 (200) ***** 400 (100) 300 300 Subsea Co $'000 ********* (300) (160) (60) (111) Required: (a) Projected statements of financial position as at 31 December 20x0 Paron Co $'000 Land Machinery Other non-current assets Inventory Other current assets Cash Share capital Retained earnings Non-current liabilities Current liabilities 200 400 290 190 120 600 1,800 Beginning retained earnings Add profit for the year Ending retained earnings 600 920 130 150 Paron Co $'000 Subsea Co $'000 1,800 900 Projected statements of changes in equity (partial) for the year ended 31 December 20x0 620 300 920 100 200 180 160 110 150 900 100 490 140 170 Subsea Co $'000 250 240 490 Prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of Paron Co and its subsidiary for the year ended 31 December 20x0, assuming Paron Co acquires all the shares of Subsea Co on 1 January 20x0. (Hint: Remember to include an "investment in Subsea Co" of $420,000 and record a reduction of cash of $420,000 in the individual statement of financial position of Paron Co before performing consolidation). (20 marks) Paron Co is intending to acquire a subsidiary on 1 January 20x0 and has shortlisted one of its regular suppliers, Subsea Co, as a potential candidate. Paron has been buying inventory and property, plant, and equipment (PPE) periodically from Subsea for the past two years. Paron Co has enough cash to acquire all the shares of Subsea Co but is currently undecided whether to acquire the shares and how many shares to acquire, if any. If Paron Co acquires all the shares of Subsea Co, Paron Co would pay $420,000 of cash to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $420,000 and a reduction of cash of $420,000 in its individual statement of financial position. Alternatively, if Paron Co acquires 70% of the shares of Subsea Co, Paron would pay cash of $294,000 to the existing shareholders of Subsea Co and record an "investment in Subsea Co" at cost of $294,000 and a reduction of cash of $294,000 in its individual statement of financial position. Assume the following information about the companies: The date of acquisition of the shares of Subsea Co is 1 January 20x0. On 1 January 20x0, the fair value of net assets of Subsea Co is represented by share capital of $100,000 and retained earnings of $250,000, except for (1) an unrecognized brand that is deemed to be worth $50,000, (ii) a piece of freehold land that was carried at a cost of $100,000 but that had a fair value of $120,000, and (iii) an unrecognized contingent liability for which there is a 30% probability of paying damages of $100,000 and a 70% probability of no payment. Any other excess payment made by Paron Co to acquire Subsea Co was for goodwill. As of 31 December 20x0, the brand and land had not been sold to external parties, the contingent liability had not been settled, and there were no changes to goodwill. During February 20x0, Subsea Co will sell machinery (which was carried in its books at cost of $120,000 less accumulated depreciation $80,000) to Paron Co for $100,000. The machinery had a remaining useful life of 3 years on the date of the intercompany sale. During 20x0, Subsea Co will sell inventory which it bought for $40,000 to Paron Co for $60,000. As at 31 December 20x0, 50% of the inventory bought from Subsea Co was not sold to external parties and remained in the store of Paron Co. As of 31 December 20x0, Paron Co was deemed to have (1) an unrecognized brand that is deemed to be worth $100,000, (11) a piece of freehold land that was carried at a cost of $200,000 but that had a fair value of $250,000, and (iii) an unrecognized contingent liability for which there is a 25% probability of paying damages of $100,000 and a 75% probability of no payment. The companies and group's accounting policies are to carry land and machinery at cost and to depreciate machinery using the straight-line method and provide for a full year's depreciation if the machinery has been used for more than 6 months during the year. The companies' and group's accounting policies are to measure inventory using the first-in-first-out method and at the lower of cost and net realizable value. The group's policy is to measure non-controlling interest based on its share of the acquisition-date fair value of identifiable net assets of the subsidiary. Shown below are the projected individual financial statements of Paron Co and Subsea Co for the year ended 31 December 20x0. Note that the projected individual statement of financial position of Paron Co had not accounted for the investment in Subsea Co. (1) Projected statements of profit or loss and other comprehensive income for the year ended 31 December 20x0 Sales Less cost of sales Gross profit Add profit on sale of machinery Less operating expenses Profit before tax Less tax Profit after tax Other comprehensive income Total comprehensive income Paron Co $'000 1,000 (400) 600 (200) ***** 400 (100) 300 300 Subsea Co $'000 ********* (300) (160) (60) (111) Required: (a) Projected statements of financial position as at 31 December 20x0 Paron Co $'000 Land Machinery Other non-current assets Inventory Other current assets Cash Share capital Retained earnings Non-current liabilities Current liabilities 200 400 290 190 120 600 1,800 Beginning retained earnings Add profit for the year Ending retained earnings 600 920 130 150 Paron Co $'000 Subsea Co $'000 1,800 900 Projected statements of changes in equity (partial) for the year ended 31 December 20x0 620 300 920 100 200 180 160 110 150 900 100 490 140 170 Subsea Co $'000 250 240 490 Prepare the consolidation journal entries and the projected consolidated financial statements (consolidated statement of profit or loss, consolidated statement of financial position, and consolidated statement of change in equity (partial)) of Paron Co and its subsidiary for the year ended 31 December 20x0, assuming Paron Co acquires all the shares of Subsea Co on 1 January 20x0. (Hint: Remember to include an "investment in Subsea Co" of $420,000 and record a reduction of cash of $420,000 in the individual statement of financial position of Paron Co before performing consolidation). (20 marks)

Expert Answer:

Answer rating: 100% (QA)

To prepare the consolidation journal entries and the projected consolidated financial statements for Paron Co and its subsidiary Subsea Co several steps must be followed To simplify the process I will ... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

Read the case study and answer the question below with a one page response. What does a SWOT analysis reveal about the overall attractiveness of Under Armours situation? Founded in 1996 by former...

-

For each of the following independent cases, state the highest level of deficiency that you believe the circumstances representa control deficiency, a significant deficiency, or a material weakness....

-

Pierce Phones is considering the introduction of a new model of headphone whose selling price is $18 per unit and whose variable expense is $15 per unit. The company's monthly fixed expense is...

-

In clinical lab reports, some concentrations are given in mg/dL. Convert a Ca2+ concentration of 6.6 mg/dL to %m/v. Express your answer using two significant figures.

-

Why would you purchase the assets of a business instead of buying the shares?

-

In 2016, a father of two minor children in Cuyahoga county, Ohio, filed a claim to determine custody of the children. At the pretrial, the father informed the magistrate he wanted to be named a legal...

-

House of Organs, Inc., purchases organs from a well-known manufacturer and sells them at the retail level. The organs sell, on the average, for $2,500 each. The average cost of an organ from the...

-

Does the City Project Meet the Pareto Efficiency Criterion? Stanley Ryan, Your Supervisor Read the following scenario and then answer the Problem Demonstration Questions below. The allocation of...

-

What are the most significant differences between the AICPA and the PCAOB standard unmodified opinion audit reports?

-

Use implicit differentiation to find an equation of the tangent line to the curve at the given point. 6(x + y2)2 = 169(x - y) (5,1) (lemniscate) y = y X

-

Rodney and Dennis are gleaning (gathering) corn from a corn field that is 1.8 miles long. Rodney starts at one end and is picking corn at a speed of .15 miles per hour. Rodney and Dennis are gleaning...

-

Can you examine the concept of dynamic delegation in the context of agile organizational structures, exploring how flexible delegation mechanisms adapt to changing market conditions and enable rapid...

-

Can you please fill this table based on the kellogs rice crispies product? Thank you Competitor analysis Brand Name Brand Purpose and Values Unique Value Proposition Tagline Target Audience Core...

-

If you were able to sell a 6 oz. bowl of soup for $4.25, how much revenue would you expect to make if you sold the entire 25-gallon batch of soup?

-

You are about to purchase a $10m apartment building that you anticipate will have a first-year PGI of $515,000, Operating Expenses of $95,000, and an NOI of $400,000. You anticipate NOI will increase...

-

On December 31, 2014, Southgate Inc. showed the following (All of the shares had been issued early in 2013): Southgate Inc. Equity Section of Balance Sheet December 31, 2014 Contributed capital...

-

Outline some of the major problems confronting an international advertiser.

-

Delta Ltd has been developing a lightweight automated wheelchair. The research costs written off have been far greater than originally estimated and the equity and preference capital has been eroded...

-

Gamma plc had an issued share capital at 1 April 20X0 of: 200,000 made up of 20p shares. 50,000 1 convertible preference shares receiving a dividend of 2.50 per share: These shares were...

-

Gettry Doffit plc is an international company with worldwide turnover of 26 million. The activities of the company include the breaking down and disposal of noxious chemicals at a specialized plant...

-

Continuing to focus on evidence associated with the act, concealment, and conversion, use the evidentiary material to continue the examination. In addition, the examiner also starts to think of terms...

-

Consider the following cash flow profile and assume MARR is 10 percent/year. a. Determine the ERR for this project. b. Is this project economically attractive? EOY 0 2 3 4 5 6 NCF -$100 $15 $15 $15...

-

Quilts R Us (QRU) is considering investing in a new patterning attachment with the cash flow profile shown in the table below. QRU's MARR is 13.5 percent/year. a. What is this investment's external...

Study smarter with the SolutionInn App