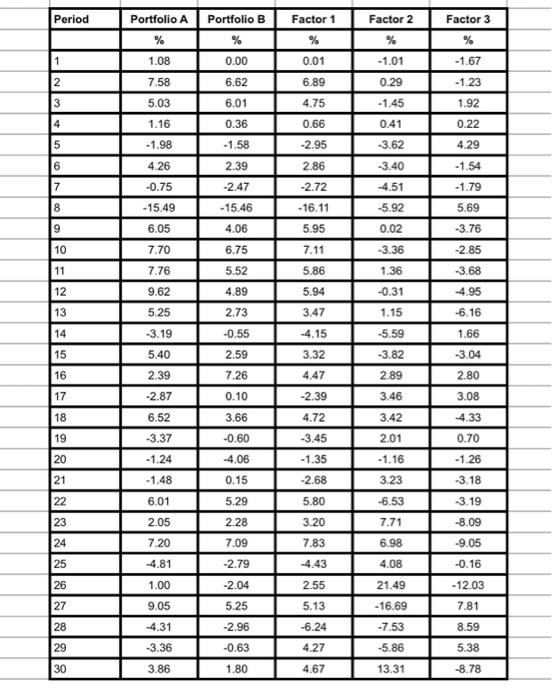

Question: Part a to e have been solved. kindly assist with part fghi. f. Using regression analysis, calculate the factor betas of each stock associated with

Period Portfolio A Factor 1 Factor 2 Factor 3 % Portfolio B % 0.00 % % % 1 1.08 0.01 - 1.01 -1.67 2 7.58 6.62 6.89 0.29 -1.23 3 5.03 6.01 4.75 -1.45 1.92 4 0.36 0.66 0.41 0.22 1.16 -1.98 5 -1.58 -2.95 -3.62 4.29 16 4.26 2.39 2.86 -3.40 -1.54 7 -0.75 -2.47 -2.72 4.51 -1.79 8 -15.49 -5.92 5.69 -15.46 4.06 9 6.05 -16.11 5.95 7.11 0.02 -3.76 10 7.70 -2.85 6.75 5.52 3.36 1.36 11 5.86 -3.68 7.76 9.62 12 4.89 5.94 -0.31 -4.95 13 5.25 2.73 3.47 1.15 -6.16 14 -0.55 -4.15 -5.59 1.66 -3.19 5.40 15 2.59 -3.82 -3.04 3.32 4.47 16 2.39 7.26 2.89 2.80 17 -2.87 0.10 -2.39 3.46 3.08 18 6.52 3.66 4.72 3.42 -4.33 19 -3.37 -0.60 -3.45 2.01 0.70 20 -1.16 -1.26 -1.24 -1.48 -4.06 0.15 -1.35 -2.68 21 3.23 3.18 22 6.01 5.29 5.80 -6.53 -3.19 23 2.05 2.28 3.20 7.71 24 7.20 7.09 7.83 6.98 -8.09 -9.05 -0.16 25 -4.81 -2.79 4.08 26 1.00 -2.04 2.55 21.49 -12.03 27 9.05 5.25 5.13 -16.69 7.81 28 -4.31 -2.96 -6.24 -7.53 8.59 29 -3.36 -0.63 4.27 -5.86 5.38 30 3.86 1.80 4.67 13.31 -8.78 Period Portfolio A Factor 1 Factor 2 Factor 3 % Portfolio B % 0.00 % % % 1 1.08 0.01 - 1.01 -1.67 2 7.58 6.62 6.89 0.29 -1.23 3 5.03 6.01 4.75 -1.45 1.92 4 0.36 0.66 0.41 0.22 1.16 -1.98 5 -1.58 -2.95 -3.62 4.29 16 4.26 2.39 2.86 -3.40 -1.54 7 -0.75 -2.47 -2.72 4.51 -1.79 8 -15.49 -5.92 5.69 -15.46 4.06 9 6.05 -16.11 5.95 7.11 0.02 -3.76 10 7.70 -2.85 6.75 5.52 3.36 1.36 11 5.86 -3.68 7.76 9.62 12 4.89 5.94 -0.31 -4.95 13 5.25 2.73 3.47 1.15 -6.16 14 -0.55 -4.15 -5.59 1.66 -3.19 5.40 15 2.59 -3.82 -3.04 3.32 4.47 16 2.39 7.26 2.89 2.80 17 -2.87 0.10 -2.39 3.46 3.08 18 6.52 3.66 4.72 3.42 -4.33 19 -3.37 -0.60 -3.45 2.01 0.70 20 -1.16 -1.26 -1.24 -1.48 -4.06 0.15 -1.35 -2.68 21 3.23 3.18 22 6.01 5.29 5.80 -6.53 -3.19 23 2.05 2.28 3.20 7.71 24 7.20 7.09 7.83 6.98 -8.09 -9.05 -0.16 25 -4.81 -2.79 4.08 26 1.00 -2.04 2.55 21.49 -12.03 27 9.05 5.25 5.13 -16.69 7.81 28 -4.31 -2.96 -6.24 -7.53 8.59 29 -3.36 -0.63 4.27 -5.86 5.38 30 3.86 1.80 4.67 13.31 -8.78

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts