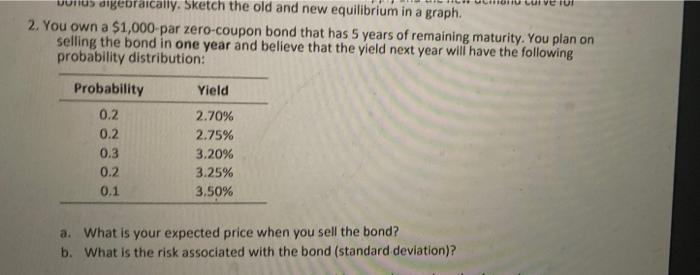

Question: part B us digebraically. Sketch the old and new equilibrium in a graph. 2. You own a $1,000 par zero-coupon bond that has 5 years

part B

us digebraically. Sketch the old and new equilibrium in a graph. 2. You own a $1,000 par zero-coupon bond that has 5 years of remaining maturity. You plan on selling the bond in one year and believe that the yield next year will have the following probability distribution: Probability Yield 0.2 2.70% 0.2 2.75% 0.3 3.20% 0.2 3.25% 0.1 3.50% a. What is your expected price when you sell the bond? b. What is the risk associated with the bond (standard deviation)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock