Question: Part I - Questions 1 - 3 0 - Multiple Choice ( Circle the best choice ) During the current year, Walter, a single taxpayer,

Part I Questions Multiple Choice Circle the best choice

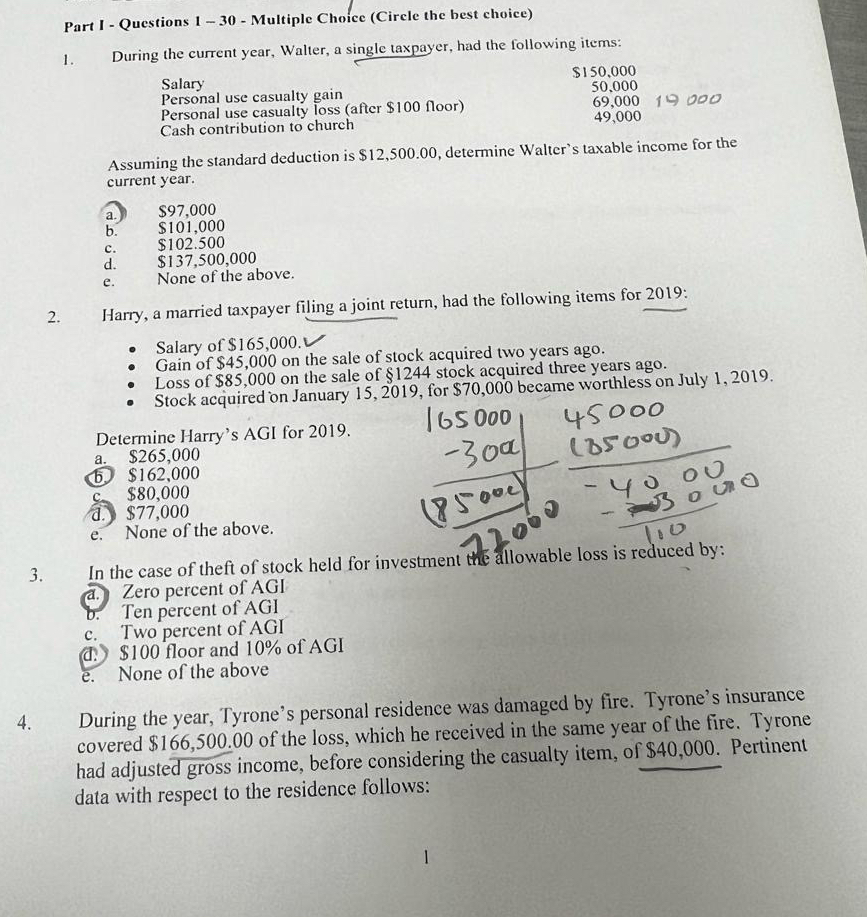

During the current year, Walter, a single taxpayer, had the following items:

tableSalaryPersonal use casualty gain,Personal use casualty loss after $ floorCash contribution to church,

Assuming the standard deduction is $ determine Walter's taxable income for the current year.

a $

b$

c $

d$

e None of the above.

Harry, a married taxpayer filing a joint return, had the following items for :

Salary of $

Gain of $ on the sale of stock acquired two years ago.

Loss of $ on the sale of $ stock acquired three years ago.

Stock acquired on January for $ became worthless on July

Determine Harry's AGI for

a $

b $

c $

a $

e None of the above.

In the case of theft of stock held for investment the allowable loss is reduced by:

a Zero percent of AGI

b Ten percent of AGI

c Two percent of AGI

d $ floor and of AGI

e None of the above

During the year, Tyrone's personal residence was damaged by fire. Tyrone's insurance covered $ of the loss, which he received in the same year of the fire. Tyrone had adjusted gross income, before considering the casualty item, of $ Pertinent data with respect to the residence follows:

![the current year, Walter, a single taxpayer, had the following items: \table[[,,],[Salary,,],[Personal](https://s3.amazonaws.com/si.experts.images/answers/2024/06/6663e7b6913f1_4146663e7b688e30.jpg)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock