Question: Part II. Problems (50 points) Problem #1. (20 points) You know the following information about the possible returns offered by the two funds, fund X

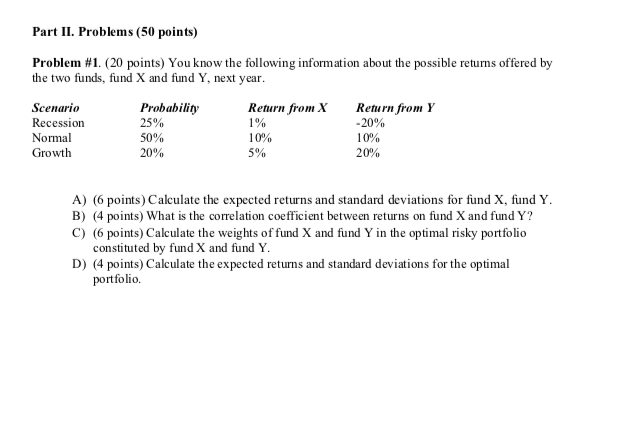

Part II. Problems (50 points) Problem #1. (20 points) You know the following information about the possible returns offered by the two funds, fund X and fund Y, next year. Scenario Probability Return from X Return from Y Recession 25% -20% Normal 50% 10% Growth 20% 5% 20% 1% 10% A) (6 points) Calculate the expected returns and standard deviations for fund X, fund Y. B) (4 points) What is the correlation coefficient between returns on fund X and fund Y? C) (6 points) Calculate the weights of fund X and fund Y in the optimal risky portfolio constituted by fund X and fund Y. D) (4 points) Calculate the expected returns and standard deviations for the optimal portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts