Question: Please advise the answer for part a to c 1. Based on a one-factor model, consider a portfolio of two securities with the following characteristics:

Please advise the answer for part a to c

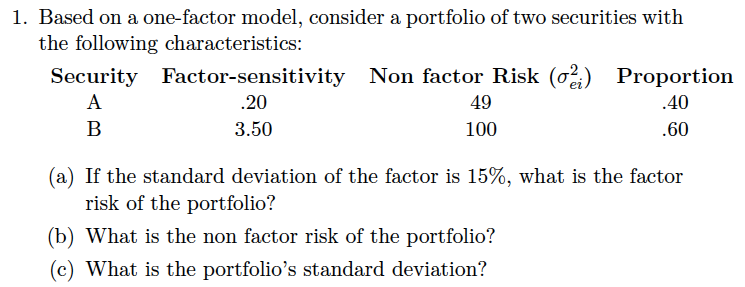

1. Based on a one-factor model, consider a portfolio of two securities with the following characteristics: Security Factor-sensitivity Non factor Risk (02) Proportion .20 49 .40 B 3.50 100 .60 (a) If the standard deviation of the factor is 15%, what is the factor risk of the portfolio? (b) What is the non factor risk of the portfolio? (c) What is the portfolio's standard deviation? 1. Based on a one-factor model, consider a portfolio of two securities with the following characteristics: Security Factor-sensitivity Non factor Risk (02) Proportion .20 49 .40 B 3.50 100 .60 (a) If the standard deviation of the factor is 15%, what is the factor risk of the portfolio? (b) What is the non factor risk of the portfolio? (c) What is the portfolio's standard deviation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts