Question: Please answer all parts ABC and please show work so i understand how to get the answer! There are some similar questions i found posted

Please answer all parts ABC and please show work so i understand how to get the answer! There are some similar questions i found posted on chegg however they have dislikes and no replies to see what is wrong with their formulas or answers please help me out!

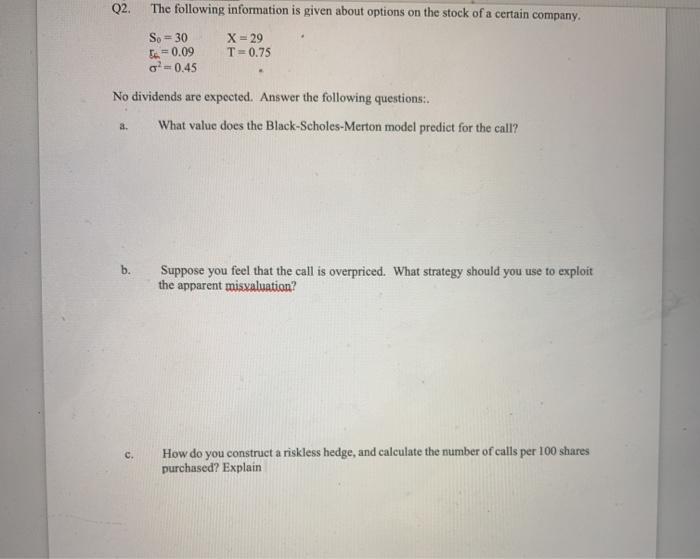

Q2. The following information is given about options on the stock of a certain company. So = 30 t=0.09 -0.45 X = 29 T=0.75 No dividends are expected. Answer the following questions: What value does the Black-Scholes-Merton model predict for the call? a. b. Suppose you feel that the call is overpriced. What strategy should you use to exploit the apparent misvaluation? c. How do you construct a riskless hedge, and calculate the number of calls per 100 shares purchased? Explain

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock