Question: Please answer all questions thanks Alternatively, consider a situation, again in the setting of Exhibit 9-9a, where the bottom of the long-run average cost curve

Please answer all questions thanks

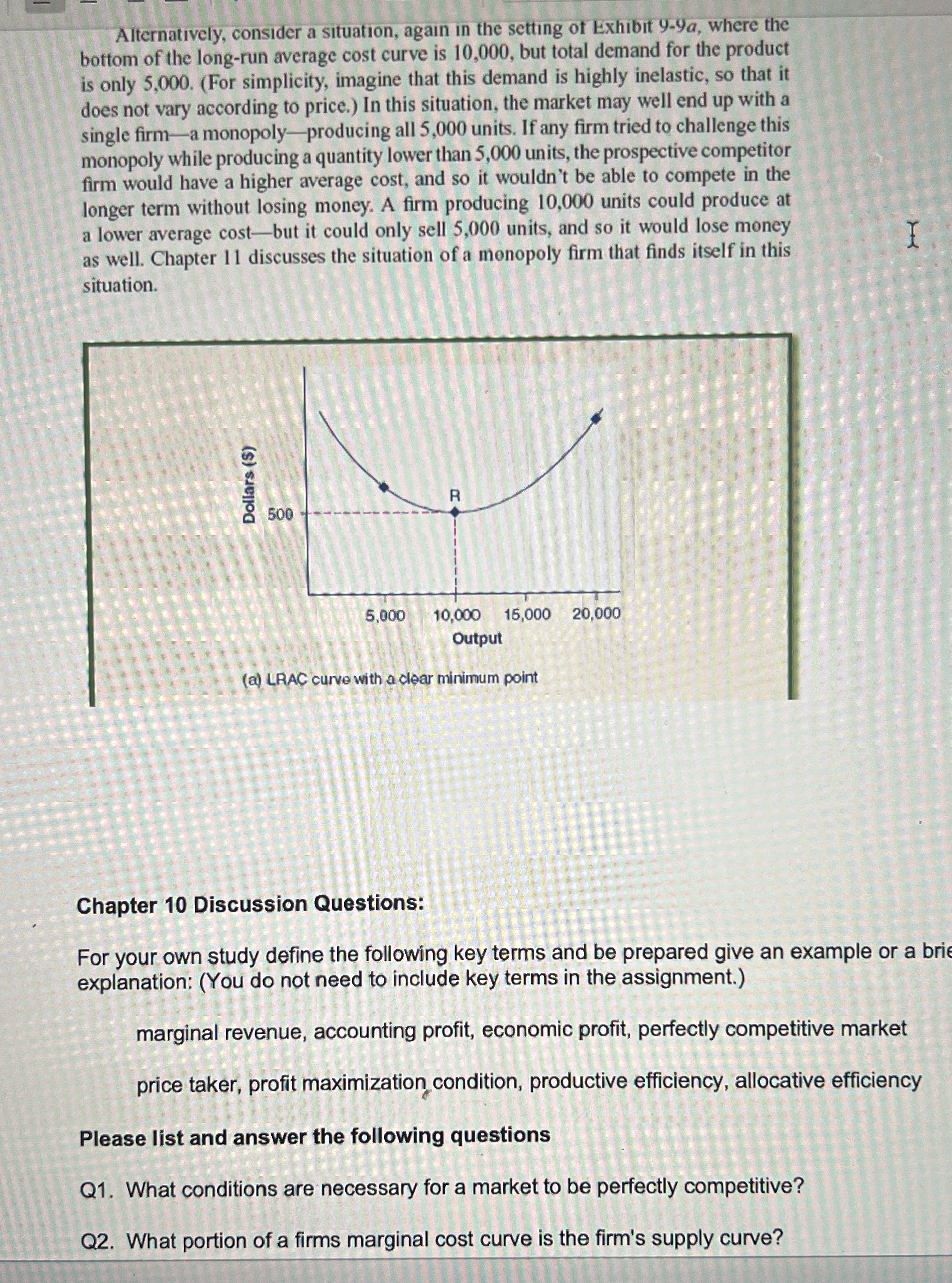

Alternatively, consider a situation, again in the setting of Exhibit 9-9a, where the bottom of the long-run average cost curve is 10,000, but total demand for the product is only 5,000. (For simplicity, imagine that this demand is highly inelastic, so that it does not vary according to price.) In this situation, the market may well end up with a single firm-a monopoly-producing all 5,000 units. If any firm tried to challenge this monopoly while producing a quantity lower than 5,000 units, the prospective competitor firm would have a higher average cost, and so it wouldn't be able to compete in the longer term without losing money. A firm producing 10,000 units could produce at a lower average cost-but it could only sell 5,000 units, and so it would lose money as well. Chapter 1 1 discusses the situation of a monopoly firm that finds itself in this situation. Dollars ($) D 500 5,000 10,000 15,000 20,000 Output (a) LRAC curve with a clear minimum point Chapter 10 Discussion Questions: For your own study define the following key terms and be prepared give an example or a bri explanation: (You do not need to include key terms in the assignment.) marginal revenue, accounting profit, economic profit, perfectly competitive market price taker, profit maximization condition, productive efficiency, allocation efficiency Please list and answer the following questions Q1. What conditions are necessary for a market to be perfectly competitive? Q2. What portion of a firms marginal cost curve is the firm's supply curve

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts