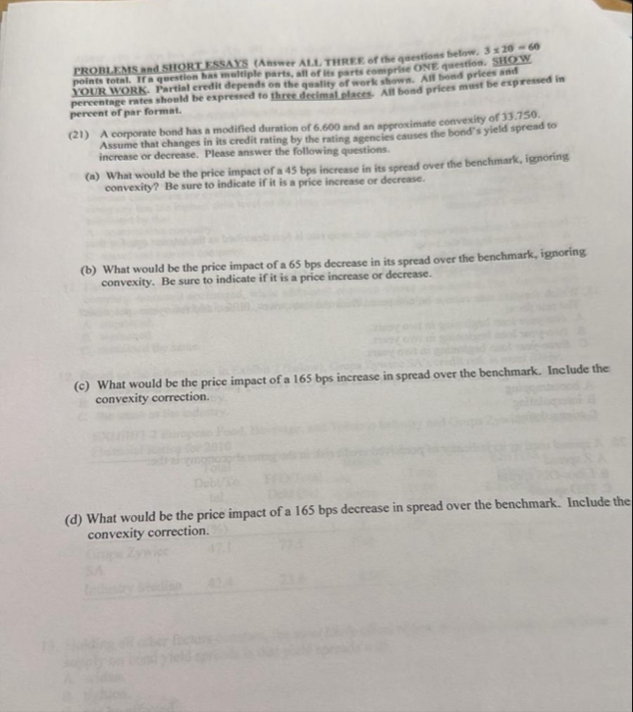

Question: PLEASE ANSWER ASAP I WILL LEAVE THUMBS UP If a question has meltiple parts, afl of its parts comprise ONE question. SHOW YOUR WORK. Partint

PLEASE ANSWER ASAP I WILL LEAVE THUMBS UP

If a question has meltiple parts, afl of its parts comprise ONE question. SHOW YOUR WORK. Partint eredit depends on the quality of work shown. All bond prices and percentage rates should be expressed to threedecimal places. All bond prices mest be expressed in percent of par format.

A corporate bond has a modified duration of and an approximate convexity of Assume that changes in its credit rating by the rating agencies causes the bond's yield spread to increase or decrease. Please answer the following questions.

a What would be the price impact of a bps increase in its spread over the benchmark, ignoring convexity? Be sure to indicate if it is a price increase or decrease.

b What would be the price impact of a bps decrease in its spread over the benchmark, ignoring convexity. Be sure to indicate if it is a price increase or decrease.

c What would be the price impact of a bps increase in spread over the benchmark. Include the convexity correction.

d What would be the price impact of a bps decrease in spread over the benchmark. Include the convexity correction.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock