Question: Please answer both part, i.e. a and b b)What happens to the replicating portfolio as the stock price changes? A stock is currently trading for

Please answer both part, i.e. a and b

b)What happens to the replicating portfolio as the stock price changes?

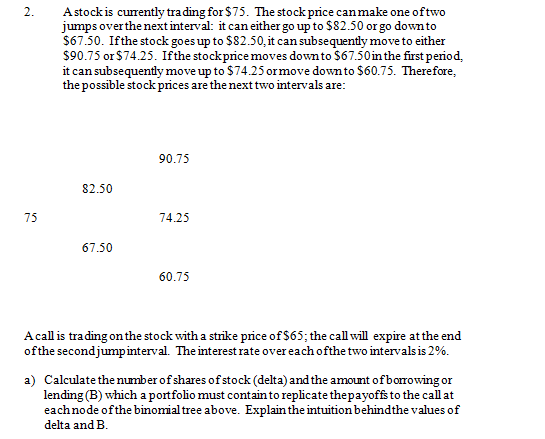

A stock is currently trading for $75. The stock price can make one of two jumps over the next interval: it can either go up to $82.50 or go down to $67.50. If the stock goes up to $82.50, it can subsequently move to either $90.75 or $74.25. If the stock price moves down to $67.50 in the first period, it can subsequently move up to $74.25 or move down to $60.75. Therefore, the possible stock prices are the next two intervals are: A call is trading on the stock with a strike price of $65: the call will expire at the end of the second jump interval. The interest rate over each of the two intervals is 2%. a) Calculate the number of shares of stock (delta) and the amount of borrowing or lending (B) which a portfolio must contain to replicate the payoffs to the call at each node of the binomial tree above. Explain the intuition behind the values of delta and E

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts