Question: Please answer part (b), part (c). u-d 2. Continuation (Pricing options): Assume that the interest rate is r = 0.04. 1+r-d (a) Compute p* the

Please answer part (b), part (c).

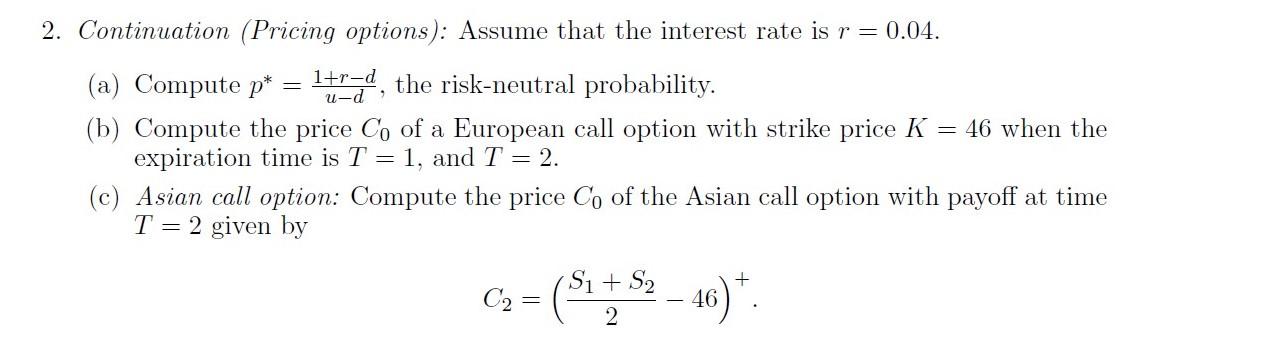

u-d 2. Continuation (Pricing options): Assume that the interest rate is r = 0.04. 1+r-d (a) Compute p* the risk-neutral probability. (b) Compute the price Co of a European call option with strike price K 46 when the expiration time is T = 1, and T = 2. (c) Asian call option: Compute the price Co of the Asian call option with payoff at time T = 2 given by = C2 = S1 + S2 2 u-d 2. Continuation (Pricing options): Assume that the interest rate is r = 0.04. 1+r-d (a) Compute p* the risk-neutral probability. (b) Compute the price Co of a European call option with strike price K 46 when the expiration time is T = 1, and T = 2. (c) Asian call option: Compute the price Co of the Asian call option with payoff at time T = 2 given by = C2 = S1 + S2 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts