Question: please answer Problem 1 (12 points): Consider a multi-factor key rate model with key rates being YTM on 2, 5, 10, and 30-year par ponds.

please answer

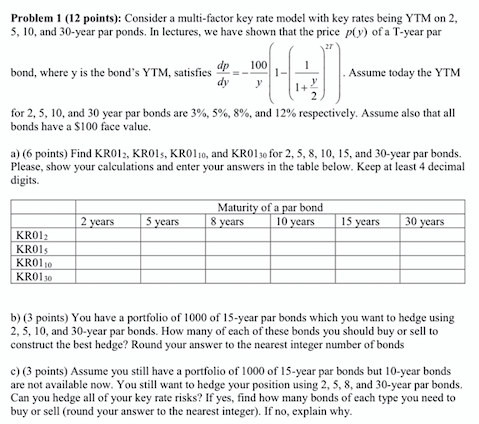

Problem 1 (12 points): Consider a multi-factor key rate model with key rates being YTM on 2, 5, 10, and 30-year par ponds. In lectures, we have shown that the price p(y) of a T-year par 100 dp bond, where y is the bond's YTM, satisfies dy Assume today the YTM y 2 for 2, 5, 10, and 30 year par bonds are 3%, 5%, 8%, and 12% respectively. Assume also that all bonds have a $100 face value. a) (6 points) Find KRO12, KROIS, KRO110, and KR01 30 for 2, 5, 8, 10, 15, and 30-year par bonds. Please, show your calculations and enter your answers in the table below. Keep at least 4 decimal digits. Maturity of a par bond 8 years 10 years 2 years 5 years 15 years 30 years KROI KROIS KR0110 KRO130 b) (3 points) You have a portfolio of 1000 of 15-year par bonds which you want to hedge using 2, 5, 10, and 30-year par bonds. How many of each of these bonds you should buy or sell to construct the best hedge? Round your answer to the nearest integer number of bonds c) (3 points) Assume you still have a portfolio of 1000 of 15-year par bonds but 10-year bonds are not available now. You still want to hedge your position using 2, 5, 8, and 30-year par bonds. Can you hedge all of your key rate risks? If yes, find how many bonds of each type you need to buy or sell (round your answer to the nearest integer). If no, explain why. Problem 1 (12 points): Consider a multi-factor key rate model with key rates being YTM on 2, 5, 10, and 30-year par ponds. In lectures, we have shown that the price p(y) of a T-year par 100 dp bond, where y is the bond's YTM, satisfies dy Assume today the YTM y 2 for 2, 5, 10, and 30 year par bonds are 3%, 5%, 8%, and 12% respectively. Assume also that all bonds have a $100 face value. a) (6 points) Find KRO12, KROIS, KRO110, and KR01 30 for 2, 5, 8, 10, 15, and 30-year par bonds. Please, show your calculations and enter your answers in the table below. Keep at least 4 decimal digits. Maturity of a par bond 8 years 10 years 2 years 5 years 15 years 30 years KROI KROIS KR0110 KRO130 b) (3 points) You have a portfolio of 1000 of 15-year par bonds which you want to hedge using 2, 5, 10, and 30-year par bonds. How many of each of these bonds you should buy or sell to construct the best hedge? Round your answer to the nearest integer number of bonds c) (3 points) Assume you still have a portfolio of 1000 of 15-year par bonds but 10-year bonds are not available now. You still want to hedge your position using 2, 5, 8, and 30-year par bonds. Can you hedge all of your key rate risks? If yes, find how many bonds of each type you need to buy or sell (round your answer to the nearest integer). If no, explain why

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts