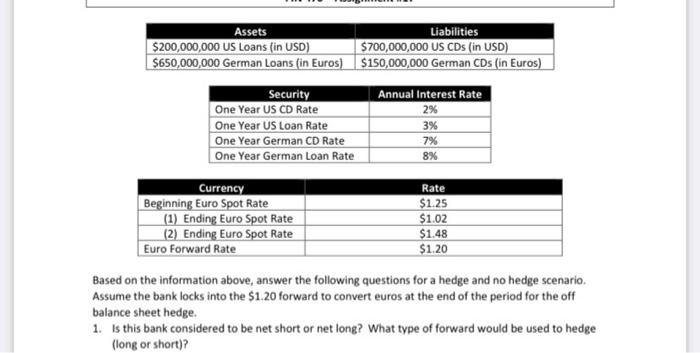

Question: please answer question #1 Assets Liabilities $200,000,000 US Loans (in USD) $700,000,000 US CDs (in USD) $650,000,000 German Loans (in Euros) $150,000,000 German CDs (in

Assets Liabilities $200,000,000 US Loans (in USD) $700,000,000 US CDs (in USD) $650,000,000 German Loans (in Euros) $150,000,000 German CDs (in Euros) Security Annual Interest Rate One Year US CD Rate 2% One Year US Loan Rate 3% One Year German CD Rate 7% One Year German Loan Rate 8% Currency Rate Beginning Euro Spot Rate $1.25 (1) Ending Euro Spot Rate $1.02 (2) Ending Euro Spot Rate Euro Forward Rate $1.20 $1.48 Based on the information above, answer the following questions for a hedge and no hedge scenario. Assume the bank locks into the $1.20 forward to convert euros at the end of the period for the off balance sheet hedge. 1. Is this bank considered to be net short or net long? What type of forward would be used to hedge (long or short)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts