Question: Please answer question 4 the first screenshot has the question background please show the formulas and explain the inputs A pension fund manager has a

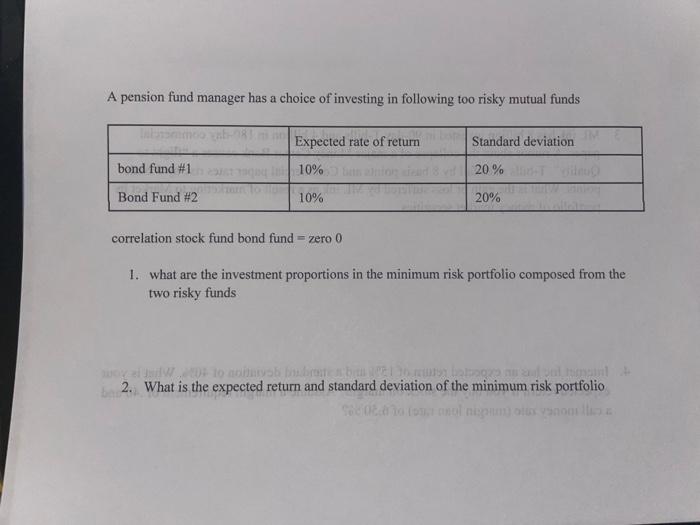

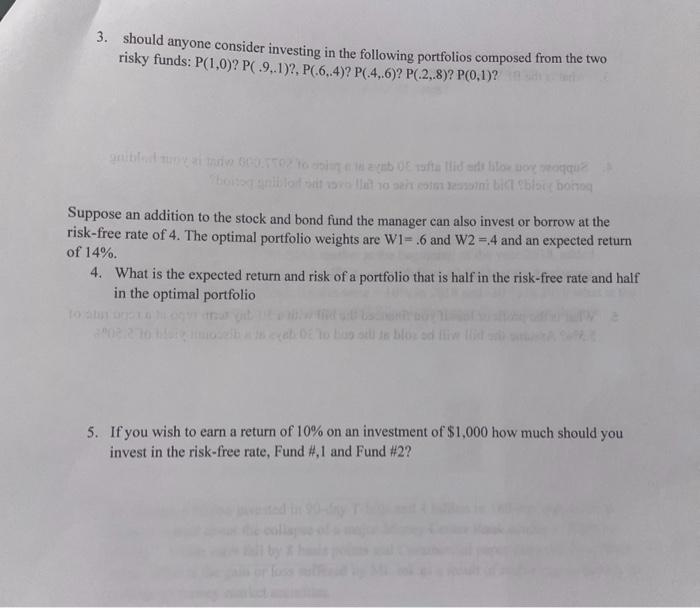

A pension fund manager has a choice of investing in following too risky mutual funds correlation stock fund bond fund = zero 0 1. what are the investment proportions in the minimum risk portfolio composed from the two risky funds 2. What is the expected return and standard deviation of the minimum risk portfolio 3. should anyone consider investing in the following portfolios composed from the two risky funds: P(1,0)?P(.9,.1)?,P(.6,4)?P(.4,6)?P(.2,.8)?P(0,1) ? Suppose an addition to the stock and bond fund the manager can also invest or borrow at the risk-free rate of 4 . The optimal portfolio weights are W1=.6 and W2=.4 and an expected return of 14%. 4. What is the expected return and risk of a portfolio that is half in the risk-free rate and half in the optimal portfolio 5. If you wish to earn a return of 10% on an investment of $1,000 how much should you invest in the risk-free rate, Fund #,1 and Fund #2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts