Question: please answer question (d) (e) (f), thank you Analysis of Financial Markets Homework 5 Question 1 Consider the following perfectly positively correlated portfolios and assume

please answer question (d) (e) (f), thank you

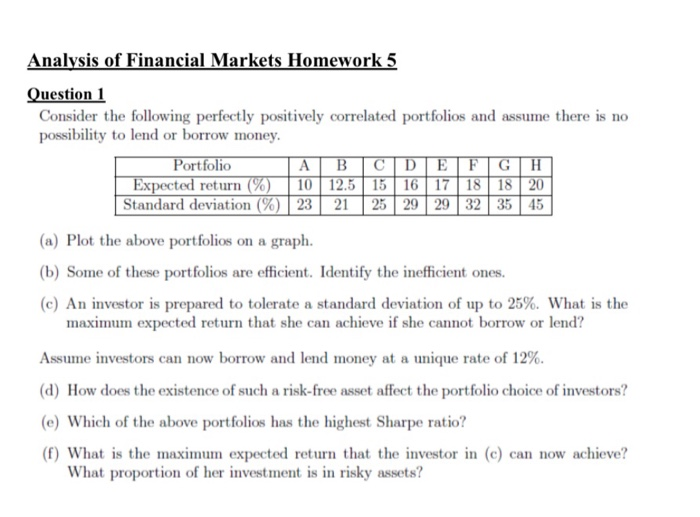

please answer question (d) (e) (f), thank youAnalysis of Financial Markets Homework 5 Question 1 Consider the following perfectly positively correlated portfolios and assume there is no possibility to lend or borrow money. Portfolio ABCDEFGH Expected return (%) 10 12.5 15 16 17 18 18 20 Standard deviation (%) 23 21 25 29 29 32 35 45 (a) Plot the above portfolios on a graph. (b) Some of these portfolios are efficient. Identify the inefficient ones. (e) An investor is prepared to tolerate a standard deviation of up to 25%. What is the maximum expected return that she can achieve if she cannot borrow or lend? Assume investors can now borrow and lend money at a unique rate of 12%. (a) How does the existence of such a risk-free asset affect the portfolio choice of investors? (e) Which of the above portfolios has the highest Sharpe ratio? (f) What is the maximum expected return that the investor in (e) can now achieve? What proportion of her investment is in risky assets

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts