Question: please answer the 4 questions on the last page. Case 100 Pressed Paper Products, Inc. Cost of Capital Directed Pressed Paper Products, Inc. (PPP) operates

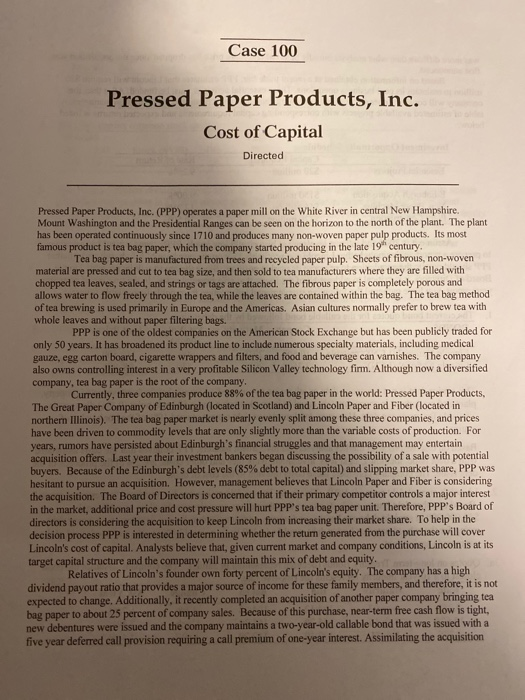

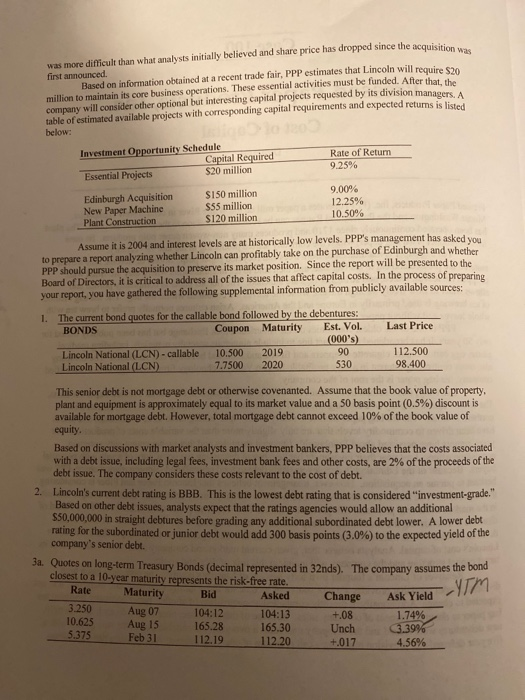

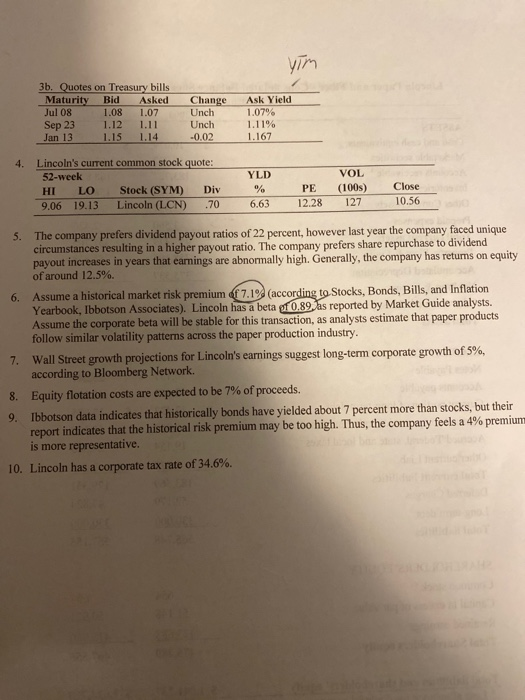

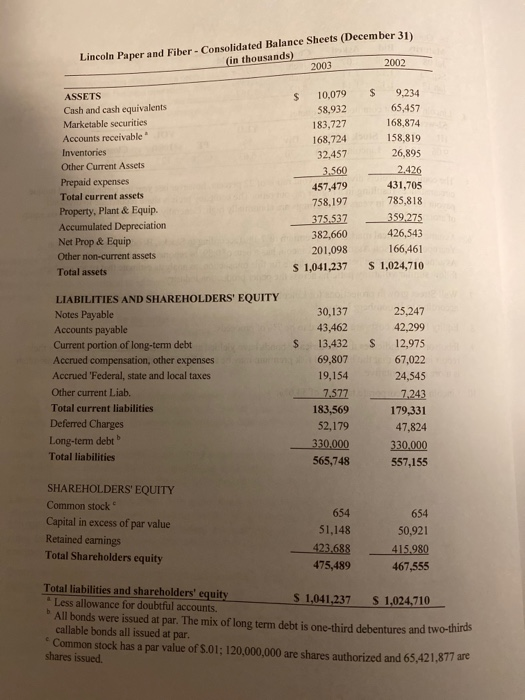

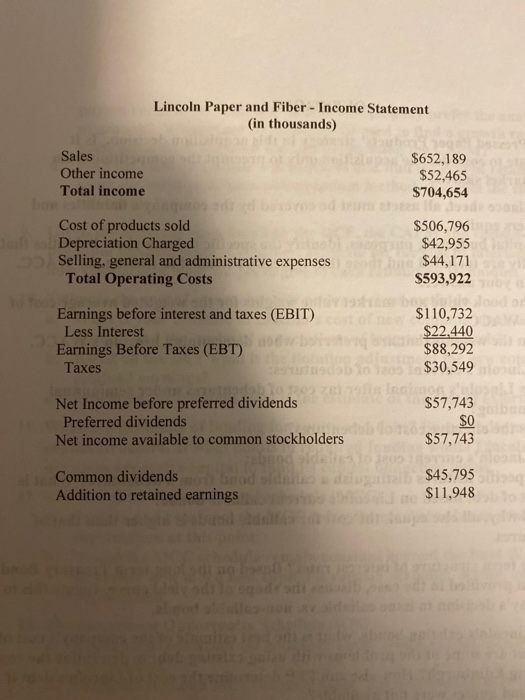

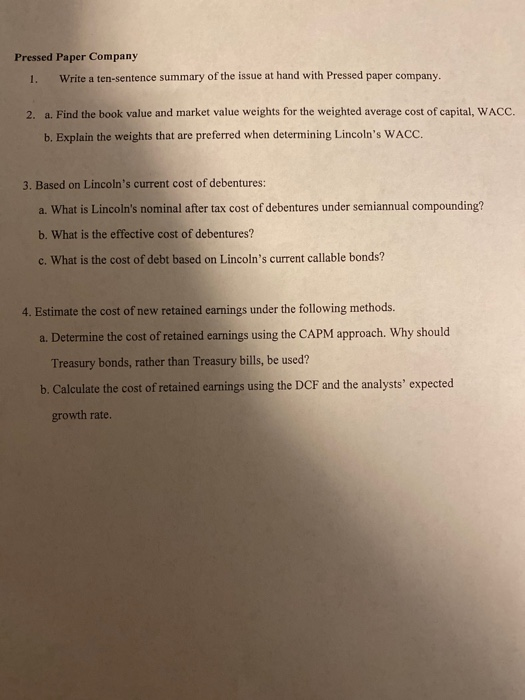

Case 100 Pressed Paper Products, Inc. Cost of Capital Directed Pressed Paper Products, Inc. (PPP) operates a paper mill on the White River in central New Hampshire. Mount Washington and the Presidential Ranges can be seen on the horizon to the north of the plant. The plant has been operated continuously since 1710 and produces many non-woven paper pulp products. Its most famous product is tea bag paper, which the company started producing in the late 19 century. Tea bag paper is manufactured from trees and recycled paper pulp. Sheets of fibrous, non-woven material are pressed and cut to tea bag size, and then sold to tea manufacturers where they are filled with chopped tea leaves, sealed, and strings or tags are attached. The fibrous paper is completely porous and allows water to flow freely through the tea, while the leaves are contained within the bag. The tea bag method of tea brewing is used primarily in Europe and the Americas. Asian cultures normally prefer to brew tea with whole leaves and without paper filtering bags. PPP is one of the oldest companies on the American Stock Exchange but has been publicly traded for only 50 years. It has broadened its product line to include numerous specialty materials, including medical zauze, egg carton board, cigarette wrappers and filters, and food and beverage can vamishes. The company also owns controlling interest in a very profitable Silicon Valley technology firm. Although now a diversified company, tea bag paper is the root of the company. Currently, three companies produce 88% of the tea bag paper in the world: Pressed Paper Products, The Great Paper Company of Edinburgh (located in Scotland) and Lincoln Paper and Fiber (located in northern Illinois). The tea bag paper market is nearly evenly split among these three companies, and prices have been driven to commodity levels that are only slightly more than the variable costs of production. For vears. rumors have persisted about Edinburgh's financial struggles and that management may entertain acquisition offers. Last year their investment bankers began discussing the possibility of a sale with potential buyers. Because of the Edinburgh's debt levels (85% debt to total capital) and slipping market share, PPP was hesitant to pursue an acquisition. However, management believes that Lincoln Paper and Fiber is considering the acquisition. The Board of Directors is concerned that if their primary competitor controls a maior interest in the market, additional price and cost pressure will hurt PPP's tea bag paper unit. Therefore, PPP's Board of directors is considering the acquisition to keep Lincoln from increasing their market share. To help in the decision process PPP is interested in determining whether the return generated from the purchase will cover Lincoln's cost of capital. Analysts believe that given current market and company conditions, Lincoln is at its target capital structure and the company will maintain this mix of debt and equity. Relatives of Lincoln's founder own forty percent of Lincoln's equity. The company has a high dividend payout ratio that provides a major source of income for these family members, and therefore, it is not expected to change. Additionally, it recently completed an acquisition of another paper company bringing tea bag paper to about 25 percent of company sales. Because of this purchase, near-term free cash flow is tight, new debentures were issued and the company maintains a two-year-old callable bond that was issued with a five year deferred call provision requiring a call premium of one-year interest. Assimilating the acquisition cquisition was was more difficult than what analysts initially believed and share price has dropped since the acquisiti first announced. Based on information obtained at a recent trade fair, PPP estimates that Lincoln will requires million to maintain its core business operations. These essential activities must be funded. After that the company will consider other optional but interesting capital projects requested by its division manager table of estimated available projects with corresponding capital requirements and expected returns is liste below: Investment Opportunity Schedule Capital Required Essential Projects $20 million Rate of Return 9.25% Edinburgh Acquisition New Paper Machine Plant Construction $150 million $55 million $120 million 9.00% 12.25% 10.50% Assume it is 2004 and interest levels are at historically low levels. PPP's management has asked you to prepare a report analyzing whether Lincoln can profitably take on the purchase of Edinburgh and whether PPP should pursue the acquisition to preserve its market position. Since the report will be presented to the Board of Directors, it is critical to address all of the issues that affect capital costs. In the process of preparing your report, you have gathered the following supplemental information from publicly available sources: 1. Last Price The current bond quotes for the callable bond followed by the debentures: BONDS Coupon Maturity Est. Vol. (000's) Lincoln National (LCN) - callable 10.500 2019 90 Lincoln National (LCN) 7.7500 2020 530 98.400 This senior debt is not mortgage debt or otherwise covenanted. Assume that the book value of property. plant and equipment is approximately equal to its market value and a 50 basis point (0.5%) discount is available for mortgage debt. However, total mortgage debt cannot exceed 10% of the book value of equity. Based on discussions with market analysts and investment bankers, PPP believes that the costs associated with a debt issue, including legal fees, investment bank fees and other costs, are 2% of the proceeds of the debt issue. The company considers these costs relevant to the cost of debt. Lincoln's current debt rating is BBB. This is the lowest debt rating that is considered investment-grade." Based on other debt issues, analysts expect that the ratings agencies would allow an additional 550,000,000 in straight debtures before grading any additional subordinated debt lower. A lower debt Caring for the subordinated or junior debt would add 300 basis points (3,0%) to the expected yield of the company's senior debt. 3a. Quotes on long-term Treasury Bonds (decimal represented in 32nds). The company assumes the bong closest to a 10-year maturity represents the risk-free rate. Rate Maturity Bid Asked Change Ask Yield- 3.250 Aug 07 104:12 104:13 +.08 1.74% 10.625 Aug 15 165.28 165.28 165.30 Unch 3.39% 5.375 Feb 31 112.19 112.20 +.017 4.56% e Ask Yield Wm 3b. Quotes on Treasury bills Maturity Bid Asked Jul 08 1.08 1.07 Sep 23 1.12 1.11 Jan 13 1 .15 1.14 Change Unch Unch -0.02 Ask Yield 1.07% 1.11% 1.167 4. Lincoln's current common stock quote: 52-week HI LO Stock (SYM) Div 9.06 19.13 Lincoln (LCN) 70 YLD % 6.63 PE 12.28 VOL (100) 127 Close 10.56 5. The company prefers dividend payout ratios of 22 percent, however last year the company faced unique circumstances resulting in a higher payout ratio. The company prefers share repurchase to dividend payout increases in years that earnings are abnormally high. Generally, the company has returns on equity of around 12.5%. 6. Assume a historical market risk premium of 7.19 (according to Stocks, Bonds, Bills, and Inflation Yearbook, Ibbotson Associates). Lincoln has a beta gf 0.89. Jas reported by Market Guide analysts. Assume the corporate beta will be stable for this transaction, as analysts estimate that paper products follow similar volatility patterns across the paper production industry. 7. Wall Street growth projections for Lincoln's earnings suggest long-term corporate growth of 5%, according to Bloomberg Network. 8. Equity flotation costs are expected to be 7% of proceeds. 9. Ibbotson data indicates that historically bonds have yielded about 7 percent more than stocks, but their report indicates that the historical risk premium may be too high. Thus, the company feels a 4% premium is more representative. 10. Lincoln has a corporate tax rate of 34.6%. Lincoln Paper and Fiber - Consolidated Balance Sheets (December 31) (in thousands) 2003 2002 ASSETS Cash and cash equivalents Marketable securities Accounts receivable Inventories Other Current Assets Prepaid expenses Total current assets Property, Plant & Equip. Accumulated Depreciation Net Prop & Equip Other non-current assets Total assets $ 10,079 58,932 183,727 168,724 32,457 3.560 457,479 758,197 375.537 382,660 201,098 S 1,041,237 $ 9,234 65,457 168,874 158,819 26,895 2.426 431,705 785,818 359,275 426,543 166,461 S 1,024,710 $ $ LIABILITIES AND SHAREHOLDERS' EQUITY Notes Payable Accounts payable Current portion of long-term debt Accrued compensation, other expenses Accrued 'Federal, state and local taxes Other current Liab. Total current liabilities Deferred Charges Long-term debt Total liabilities 30,137 43,462 13,432 69,807 19,154 7,577 183,569 52,179 330,000 565,748 25,247 42,299 12,975 67,022 24,545 7,243 179,331 47,824 330,000 557,155 SHAREHOLDERS' EQUITY Common stock Capital in excess of par value Retained earnings Total Shareholders equity 654 51,148 423.688 475,489 654 50,921 415.980 467,555 Total liabilities and shareholders' equity S 1,041,237 S 1,024,710 Less allowance for doubtful accounts. All bonds were issued at par. The mix of long term debt is one-third debentures and two- callable bonds all issued at par. Common stock has a par value of S.01; 120,000,000 are shares authorized and 65,421,877 are shares issued Lincoln Paper and Fiber - Income Statement (in thousands) Sales Other income Total income $652,189 $52,465 $704,654 Cost of products sold Depreciation Charged Selling, general and administrative expenses Total Operating Costs $506,796 $42,955 $44,171 $593,922 Earnings before interest and taxes (EBIT) Less Interest Earnings Before Taxes (EBT) Taxes $110,732 $22.440 $88,292 $30,549 Net Income before preferred dividends Preferred dividends Net income available to common stockholders $57,743 $0 $57,743 Common dividends Addition to retained earnings $45,795 to $11,948 Pressed Paper Company 1. Write a ten-sentence summary of the issue at hand with Pressed paper company. 2. a. Find the book value and market value weights for the weighted average cost of capital, WACC. b. Explain the weights that are preferred when determining Lincoln's WACC. 3. Based on Lincoln's current cost of debentures: a. What is Lincoln's nominal after tax cost of debentures under semiannual compounding? b. What is the effective cost of debentures? c. What is the cost of debt based on Lincoln's current callable bonds? 4. Estimate the cost of new retained earnings under the following methods. a. Determine the cost of retained earnings using the CAPM approach. Why should Treasury bonds, rather than Treasury bills, be used? b. Calculate the cost of retained earnings using the DCF and the analysts' expected growth rate. Case 100 Pressed Paper Products, Inc. Cost of Capital Directed Pressed Paper Products, Inc. (PPP) operates a paper mill on the White River in central New Hampshire. Mount Washington and the Presidential Ranges can be seen on the horizon to the north of the plant. The plant has been operated continuously since 1710 and produces many non-woven paper pulp products. Its most famous product is tea bag paper, which the company started producing in the late 19 century. Tea bag paper is manufactured from trees and recycled paper pulp. Sheets of fibrous, non-woven material are pressed and cut to tea bag size, and then sold to tea manufacturers where they are filled with chopped tea leaves, sealed, and strings or tags are attached. The fibrous paper is completely porous and allows water to flow freely through the tea, while the leaves are contained within the bag. The tea bag method of tea brewing is used primarily in Europe and the Americas. Asian cultures normally prefer to brew tea with whole leaves and without paper filtering bags. PPP is one of the oldest companies on the American Stock Exchange but has been publicly traded for only 50 years. It has broadened its product line to include numerous specialty materials, including medical zauze, egg carton board, cigarette wrappers and filters, and food and beverage can vamishes. The company also owns controlling interest in a very profitable Silicon Valley technology firm. Although now a diversified company, tea bag paper is the root of the company. Currently, three companies produce 88% of the tea bag paper in the world: Pressed Paper Products, The Great Paper Company of Edinburgh (located in Scotland) and Lincoln Paper and Fiber (located in northern Illinois). The tea bag paper market is nearly evenly split among these three companies, and prices have been driven to commodity levels that are only slightly more than the variable costs of production. For vears. rumors have persisted about Edinburgh's financial struggles and that management may entertain acquisition offers. Last year their investment bankers began discussing the possibility of a sale with potential buyers. Because of the Edinburgh's debt levels (85% debt to total capital) and slipping market share, PPP was hesitant to pursue an acquisition. However, management believes that Lincoln Paper and Fiber is considering the acquisition. The Board of Directors is concerned that if their primary competitor controls a maior interest in the market, additional price and cost pressure will hurt PPP's tea bag paper unit. Therefore, PPP's Board of directors is considering the acquisition to keep Lincoln from increasing their market share. To help in the decision process PPP is interested in determining whether the return generated from the purchase will cover Lincoln's cost of capital. Analysts believe that given current market and company conditions, Lincoln is at its target capital structure and the company will maintain this mix of debt and equity. Relatives of Lincoln's founder own forty percent of Lincoln's equity. The company has a high dividend payout ratio that provides a major source of income for these family members, and therefore, it is not expected to change. Additionally, it recently completed an acquisition of another paper company bringing tea bag paper to about 25 percent of company sales. Because of this purchase, near-term free cash flow is tight, new debentures were issued and the company maintains a two-year-old callable bond that was issued with a five year deferred call provision requiring a call premium of one-year interest. Assimilating the acquisition cquisition was was more difficult than what analysts initially believed and share price has dropped since the acquisiti first announced. Based on information obtained at a recent trade fair, PPP estimates that Lincoln will requires million to maintain its core business operations. These essential activities must be funded. After that the company will consider other optional but interesting capital projects requested by its division manager table of estimated available projects with corresponding capital requirements and expected returns is liste below: Investment Opportunity Schedule Capital Required Essential Projects $20 million Rate of Return 9.25% Edinburgh Acquisition New Paper Machine Plant Construction $150 million $55 million $120 million 9.00% 12.25% 10.50% Assume it is 2004 and interest levels are at historically low levels. PPP's management has asked you to prepare a report analyzing whether Lincoln can profitably take on the purchase of Edinburgh and whether PPP should pursue the acquisition to preserve its market position. Since the report will be presented to the Board of Directors, it is critical to address all of the issues that affect capital costs. In the process of preparing your report, you have gathered the following supplemental information from publicly available sources: 1. Last Price The current bond quotes for the callable bond followed by the debentures: BONDS Coupon Maturity Est. Vol. (000's) Lincoln National (LCN) - callable 10.500 2019 90 Lincoln National (LCN) 7.7500 2020 530 98.400 This senior debt is not mortgage debt or otherwise covenanted. Assume that the book value of property. plant and equipment is approximately equal to its market value and a 50 basis point (0.5%) discount is available for mortgage debt. However, total mortgage debt cannot exceed 10% of the book value of equity. Based on discussions with market analysts and investment bankers, PPP believes that the costs associated with a debt issue, including legal fees, investment bank fees and other costs, are 2% of the proceeds of the debt issue. The company considers these costs relevant to the cost of debt. Lincoln's current debt rating is BBB. This is the lowest debt rating that is considered investment-grade." Based on other debt issues, analysts expect that the ratings agencies would allow an additional 550,000,000 in straight debtures before grading any additional subordinated debt lower. A lower debt Caring for the subordinated or junior debt would add 300 basis points (3,0%) to the expected yield of the company's senior debt. 3a. Quotes on long-term Treasury Bonds (decimal represented in 32nds). The company assumes the bong closest to a 10-year maturity represents the risk-free rate. Rate Maturity Bid Asked Change Ask Yield- 3.250 Aug 07 104:12 104:13 +.08 1.74% 10.625 Aug 15 165.28 165.28 165.30 Unch 3.39% 5.375 Feb 31 112.19 112.20 +.017 4.56% e Ask Yield Wm 3b. Quotes on Treasury bills Maturity Bid Asked Jul 08 1.08 1.07 Sep 23 1.12 1.11 Jan 13 1 .15 1.14 Change Unch Unch -0.02 Ask Yield 1.07% 1.11% 1.167 4. Lincoln's current common stock quote: 52-week HI LO Stock (SYM) Div 9.06 19.13 Lincoln (LCN) 70 YLD % 6.63 PE 12.28 VOL (100) 127 Close 10.56 5. The company prefers dividend payout ratios of 22 percent, however last year the company faced unique circumstances resulting in a higher payout ratio. The company prefers share repurchase to dividend payout increases in years that earnings are abnormally high. Generally, the company has returns on equity of around 12.5%. 6. Assume a historical market risk premium of 7.19 (according to Stocks, Bonds, Bills, and Inflation Yearbook, Ibbotson Associates). Lincoln has a beta gf 0.89. Jas reported by Market Guide analysts. Assume the corporate beta will be stable for this transaction, as analysts estimate that paper products follow similar volatility patterns across the paper production industry. 7. Wall Street growth projections for Lincoln's earnings suggest long-term corporate growth of 5%, according to Bloomberg Network. 8. Equity flotation costs are expected to be 7% of proceeds. 9. Ibbotson data indicates that historically bonds have yielded about 7 percent more than stocks, but their report indicates that the historical risk premium may be too high. Thus, the company feels a 4% premium is more representative. 10. Lincoln has a corporate tax rate of 34.6%. Lincoln Paper and Fiber - Consolidated Balance Sheets (December 31) (in thousands) 2003 2002 ASSETS Cash and cash equivalents Marketable securities Accounts receivable Inventories Other Current Assets Prepaid expenses Total current assets Property, Plant & Equip. Accumulated Depreciation Net Prop & Equip Other non-current assets Total assets $ 10,079 58,932 183,727 168,724 32,457 3.560 457,479 758,197 375.537 382,660 201,098 S 1,041,237 $ 9,234 65,457 168,874 158,819 26,895 2.426 431,705 785,818 359,275 426,543 166,461 S 1,024,710 $ $ LIABILITIES AND SHAREHOLDERS' EQUITY Notes Payable Accounts payable Current portion of long-term debt Accrued compensation, other expenses Accrued 'Federal, state and local taxes Other current Liab. Total current liabilities Deferred Charges Long-term debt Total liabilities 30,137 43,462 13,432 69,807 19,154 7,577 183,569 52,179 330,000 565,748 25,247 42,299 12,975 67,022 24,545 7,243 179,331 47,824 330,000 557,155 SHAREHOLDERS' EQUITY Common stock Capital in excess of par value Retained earnings Total Shareholders equity 654 51,148 423.688 475,489 654 50,921 415.980 467,555 Total liabilities and shareholders' equity S 1,041,237 S 1,024,710 Less allowance for doubtful accounts. All bonds were issued at par. The mix of long term debt is one-third debentures and two- callable bonds all issued at par. Common stock has a par value of S.01; 120,000,000 are shares authorized and 65,421,877 are shares issued Lincoln Paper and Fiber - Income Statement (in thousands) Sales Other income Total income $652,189 $52,465 $704,654 Cost of products sold Depreciation Charged Selling, general and administrative expenses Total Operating Costs $506,796 $42,955 $44,171 $593,922 Earnings before interest and taxes (EBIT) Less Interest Earnings Before Taxes (EBT) Taxes $110,732 $22.440 $88,292 $30,549 Net Income before preferred dividends Preferred dividends Net income available to common stockholders $57,743 $0 $57,743 Common dividends Addition to retained earnings $45,795 to $11,948 Pressed Paper Company 1. Write a ten-sentence summary of the issue at hand with Pressed paper company. 2. a. Find the book value and market value weights for the weighted average cost of capital, WACC. b. Explain the weights that are preferred when determining Lincoln's WACC. 3. Based on Lincoln's current cost of debentures: a. What is Lincoln's nominal after tax cost of debentures under semiannual compounding? b. What is the effective cost of debentures? c. What is the cost of debt based on Lincoln's current callable bonds? 4. Estimate the cost of new retained earnings under the following methods. a. Determine the cost of retained earnings using the CAPM approach. Why should Treasury bonds, rather than Treasury bills, be used? b. Calculate the cost of retained earnings using the DCF and the analysts' expected growth rate

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts