Question: PLEASE ANSWER THE FULL QUESTION THEY ARE INTERELATED AND PART OF 1 MAIN QUESTION. IT IS URGENT THANK YOU! 2. a. Over a two year

PLEASE ANSWER THE FULL QUESTION THEY ARE INTERELATED AND PART OF 1 MAIN QUESTION.

IT IS URGENT THANK YOU!

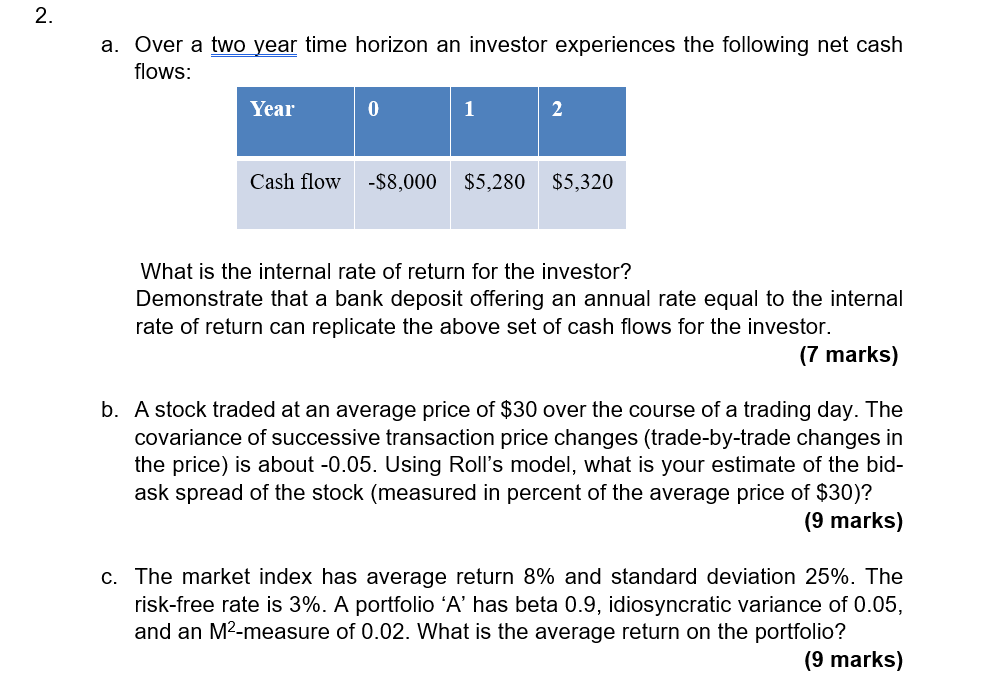

2. a. Over a two year time horizon an investor experiences the following net cash flows: Year 0 1 2 Cash flow -$8,000 $5,280 $5,320 What is the internal rate of return for the investor? Demonstrate that a bank deposit offering an annual rate equal to the internal rate of return can replicate the above set of cash flows for the investor. (7 marks) b. A stock traded at an average price of $30 over the course of a trading day. The covariance of successive transaction price changes (trade-by-trade changes in the price) is about -0.05. Using Roll's model, what is your estimate of the bid- ask spread of the stock (measured in percent of the average price of $30)? (9 marks) C. The market index has average return 8% and standard deviation 25%. The risk-free rate is 3%. A portfolio 'A' has beta 0.9, idiosyncratic variance of 0.05, and an M2-measure of 0.02. What is the average return on the portfolio? (9 marks) 2. a. Over a two year time horizon an investor experiences the following net cash flows: Year 0 1 2 Cash flow -$8,000 $5,280 $5,320 What is the internal rate of return for the investor? Demonstrate that a bank deposit offering an annual rate equal to the internal rate of return can replicate the above set of cash flows for the investor. (7 marks) b. A stock traded at an average price of $30 over the course of a trading day. The covariance of successive transaction price changes (trade-by-trade changes in the price) is about -0.05. Using Roll's model, what is your estimate of the bid- ask spread of the stock (measured in percent of the average price of $30)? (9 marks) C. The market index has average return 8% and standard deviation 25%. The risk-free rate is 3%. A portfolio 'A' has beta 0.9, idiosyncratic variance of 0.05, and an M2-measure of 0.02. What is the average return on the portfolio? (9 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts