Question: Please answer the next question based on the closing July futures contract prices for Swiss francs (CHF) for three consecutive days in April 20XX. Each

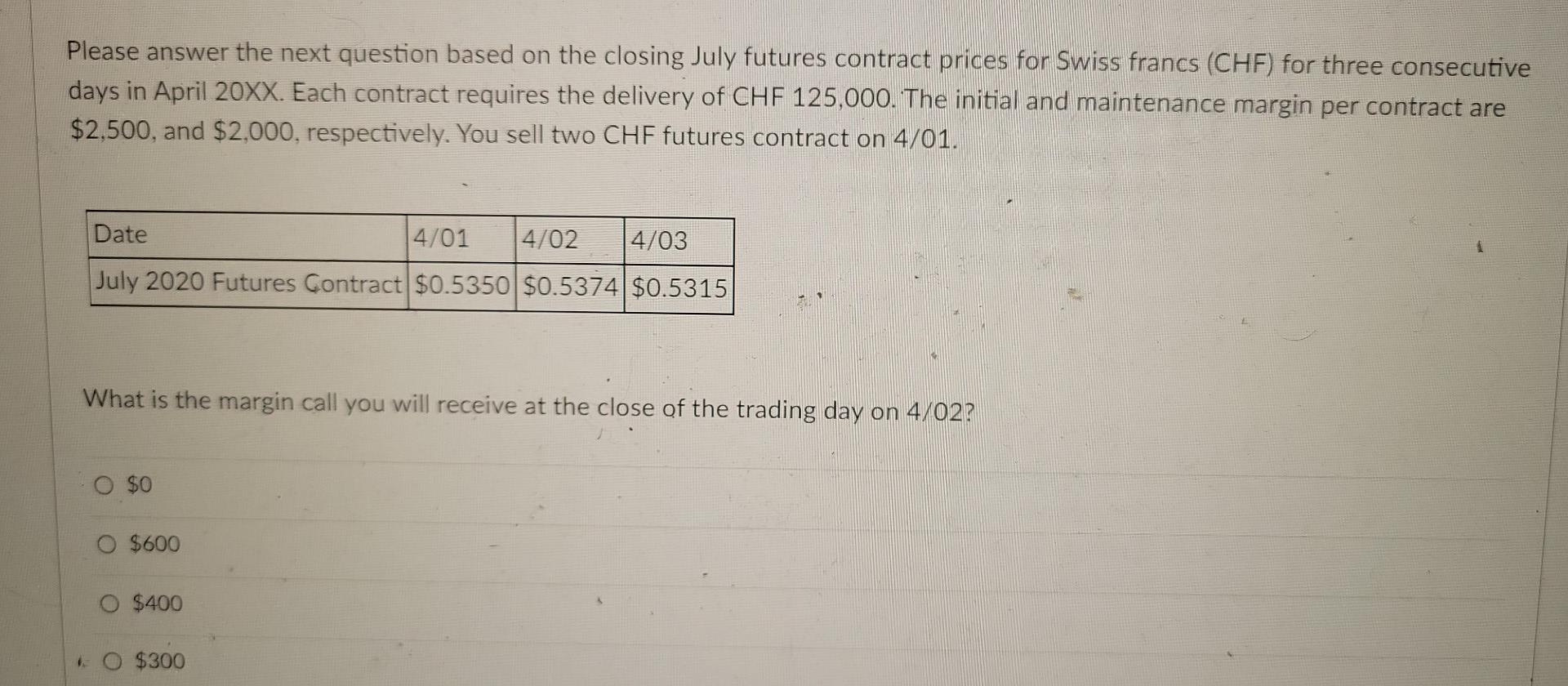

Please answer the next question based on the closing July futures contract prices for Swiss francs (CHF) for three consecutive days in April 20XX. Each contract requires the delivery of CHF 125,000. The initial and maintenance margin per contract are $2,500, and $2,000, respectively. You sell two CHF futures contract on 4/01. Date 4/01 4/02 4/03 July 2020 Futures Contract $0.5350 $0.5374 $0.5315 What is the margin call you will receive at the close of the trading day on 4/02? O $0 O $600 0 $400 $300

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock