Question: Please answer this question please. Thanks! Risk and return answers can be in percentage A researcher provides you with the following information for two risky

Please answer this question please. Thanks!

Risk and return answers can be in percentage

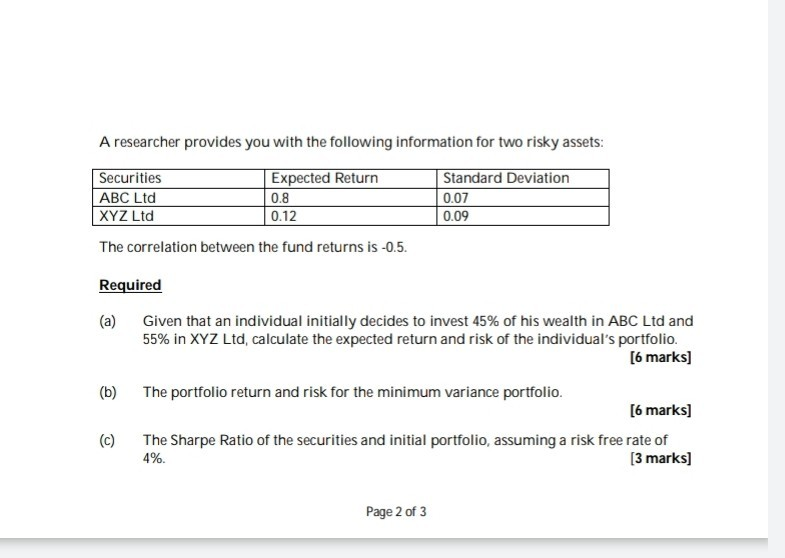

A researcher provides you with the following information for two risky assets: Securities ABC Ltd XYZ Ltd Expected Return 0.8 0.12 Standard Deviation 0.07 0.09 The correlation between the fund returns is -0.5. Required (a) Given that an individual initially decides to invest 45% of his wealth in ABC Ltd and 55% in XYZ Ltd, calculate the expected return and risk of the individual's portfolio. [6 marks] (b) The portfolio return and risk for the minimum variance portfolio. [6 marks] (c) The Sharpe Ratio of the securities and initial portfolio, assuming a risk free rate of 4%. [3 marks] Page 2 of 3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts