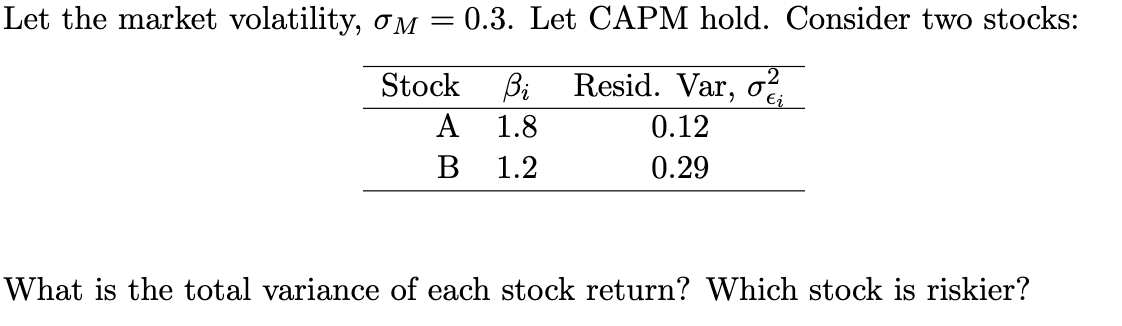

Question: Please answer this question. Thanks Let the market volatility, 0M = 0.3. Let CAPM hold. Consider two stocks: Stock g- Resid. Var, of. A 1.8

Please answer this question. Thanks

Let the market volatility, 0M = 0.3. Let CAPM hold. Consider two stocks: Stock g- Resid. Var, of. A 1.8 0.12 B 1.2 0.29 What is the total variance of each stock return? Which stock is riskier

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock